Oliver Stone

Global markets began 2026 on a broadly constructive footing, with January delivering positive returns across most major asset classes despite an ongoing backdrop of macroeconomic, political, and geopolitical uncertainty. Rather than a simple risk-on or risk-off environment, market outcomes were shaped by pronounced rotation across regions, styles, currencies, and asset classes. Leadership continued to broaden beyond the narrow concentration that defined much of the past two years, while bond markets reflected growing divergence across sovereign curves and credit sectors.

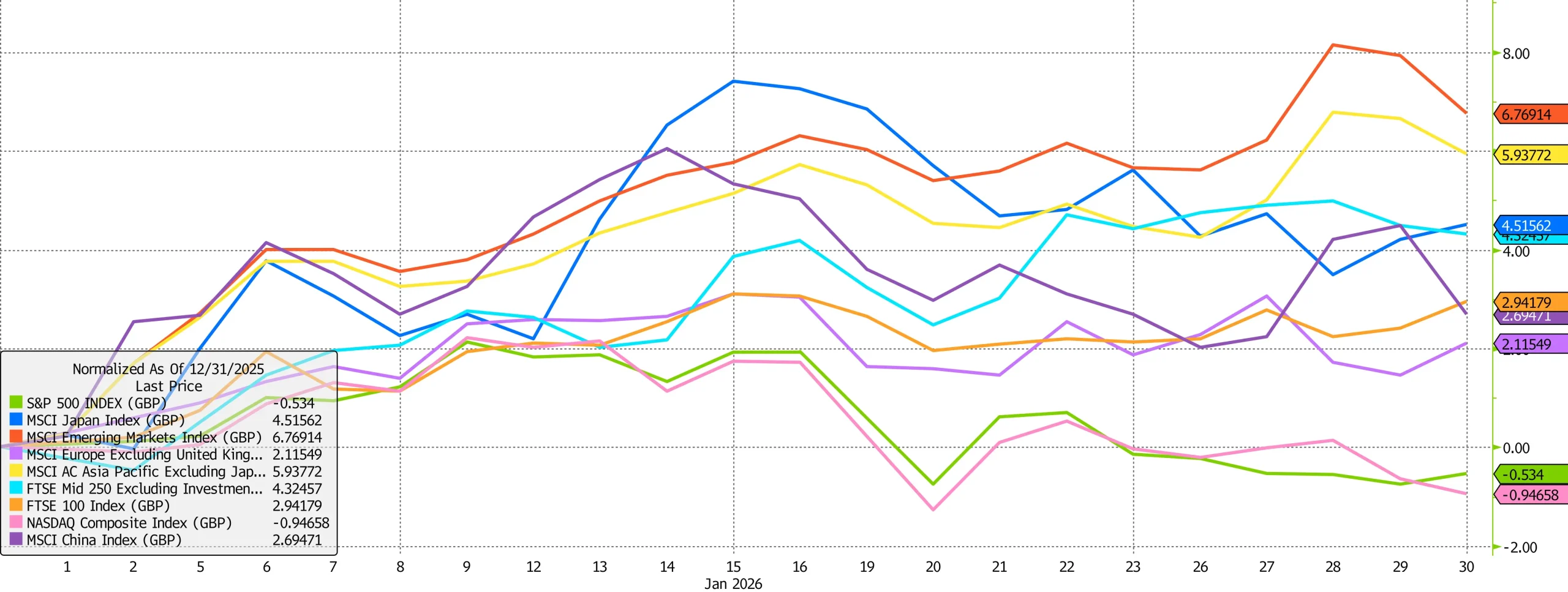

Source: Bloomberg

Global equities advanced meaningfully during the month, with the global equity index rising 1.0% in sterling terms, supported by strong performance across Asia (shown in yellow) and emerging markets (in red). Improving macroeconomic indicators, easing financial conditions, and resilient earnings sentiment underpinned gains in these regions, offsetting more muted returns across parts of the developed world, particularly the United States.

Within emerging markets, equities across Latin America and Asia rallied sharply, supported by US dollar weakness, favourable duration dynamics, and renewed investor appetite for higher-beta exposures. At a country level, Korea performed especially well, while Brazil also posted notable gains, benefiting from rising commodity prices and improving domestic sentiment. In China, shares in property developers jumped after reports that Beijing had effectively dismantled its long-standing “three red lines” policy, removing borrowing limits that had constrained developers and contributed to a prolonged debt crisis. While largely symbolic and insufficient to resolve deeper structural challenges, the move was interpreted as an acknowledgment that policy tightening had gone too far in a sector central to household wealth and local government finances.

Across developed markets, performance was more mixed. In the US, January marked a continuation of the style rotation that had begun to surface at various points in 2025. Value-oriented and cyclical sectors outperformed growth, signalling a pause in the multi-year dominance of growth and AI-related themes. The region’s technology index, the Nasdaq (above in pink), edged down 0.9%, while the broader S&P 500 (in green) fell 0.5%, lagging both small-cap equities and many international markets. The “Magnificent Seven” underperformed the broader index, highlighting increasing investor sensitivity to valuation, earnings quality, and capital intensity.

This shift was reinforced by heightened earnings-related volatility within the US technology sector. A notable example was Microsoft, which recorded its largest one-day share price decline since March 2020. Despite delivering strong earnings growth, investor concerns around elevated capital expenditure and the lengthening payback period for AI-related investment weighed on sentiment. This episode underscored growing selectivity within what had previously been a broadly supported technology complex, as markets increasingly differentiate between revenue growth, capital efficiency, and long-term returns on investment.

Elsewhere, Japanese equities (above in blue) delivered one of the strongest performances among developed markets, rising 4.5%. Equity strength was underpinned by ongoing corporate governance reforms, robust capital expenditure trends, and improving consumer sentiment. Investor confidence was further boosted by a surprise election announcement from Prime Minister Sanae Takaichi, who is seeking a strengthened mandate for her reflationary policy agenda centred on fiscal stimulus, tax reductions, and wage growth. While equity markets welcomed the growth narrative, bond markets were more cautious, reflecting concerns around increased government borrowing given Japan’s already elevated debt burden.

Across Europe and the UK (above in purple and orange, respectively), equity markets posted modest but consistent gains in January. Inflation continued to ease across both regions, while economic indicators began to show early signs of stabilisation. With the European Central Bank expected to maintain policy rates at current levels in the months ahead, and supportive fiscal developments, most notably Germany’s newly implemented 2025 budget, regional confidence has remained firm. These conditions reinforced the positive momentum seen in European equity markets toward the end of last year, when improved policy clarity and resilient earnings helped lift indices to multi-year highs. UK equities displayed similar resilience, underpinned by moderating inflation, gradual real wage growth, and positive spillover effects from strengthening economic conditions across Europe.

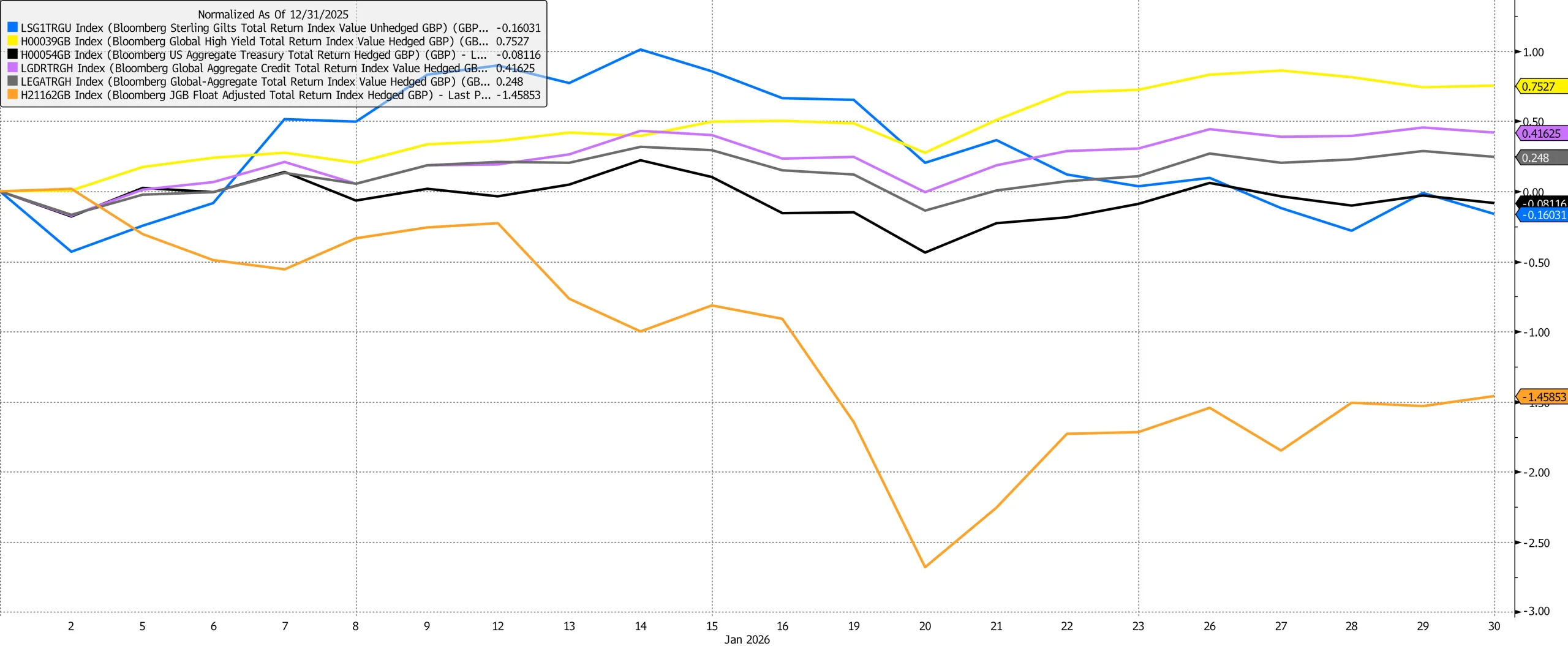

Bond markets added an important additional layer to January’s market narrative. One month into the year, the long end of the government bond curve underperformed across most major markets. Japanese government bonds stood out as the weakest segment, with the yield curve steepening sharply amid rising inflation expectations and concerns over debt sustainability. In contrast, European government bonds outperformed their US and UK counterparts, benefiting from relative policy clarity, easing inflation, and more contained issuance expectations.

Source: Bloomberg

In the US, Treasury markets were more challenging. Although the Federal Reserve held interest rates steady, long-end yields rose through January, leading Treasuries to close the month down 0.1%. The Federal Open Market Committee meeting itself proved largely anticlimactic, with Chair Powell maintaining an optimistic “Goldilocks” tone on the economy, highlighting steady activity and signs of stabilisation in the labour market. Although inflation remains above target, Powell suggested much of the current overshoot is tariff-related and likely to peak in the second quarter of the year.

Corporate credit was a clear winner within fixed income, with the global corporate bond index (in purple, above) rising 0.4% versus 0.2% from the broad global bond index (above in grey). Risk appetite remained firm, global financial conditions continued to loosen, and default expectations stayed contained. Within investment-grade credit, European corporate bonds outperformed, helped by the relative strength of European sovereign markets. Credit spreads tightened modestly, but investors remained selective, favouring balance-sheet strength and regions with supportive policy backdrops.

Commodities also played a meaningful role in shaping market dynamics. Energy prices surprised to the upside, with Brent crude rising by roughly 15% over the, well above consensus expectations for the first quarter of 2026. This move supported energy equities globally and contributed to the outperformance of commodity-linked regions, particularly in emerging markets. The rise in energy prices also fed into bond market dynamics, reinforcing sensitivity at the long end of yield curves.

Looking ahead, we expect markets to remain focused on the trajectory of the US dollar, geopolitical developments, and the evolving global policy landscape. January’s market behaviour points toward a more multipolar investment environment in 2026, where returns are driven less by a single theme or region and more by underlying fundamentals and diversification across geographies, styles, and asset classes.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: