Oliver Stone

February proved to be a month of stark regional divergence across global equity markets, punctuated by a landmark US Supreme Court ruling that reshaped the tariff landscape, and escalating geopolitical tensions in the Middle East. For UK investors, sterling weakness against most major currencies added an additional layer of complexity to portfolio positioning.

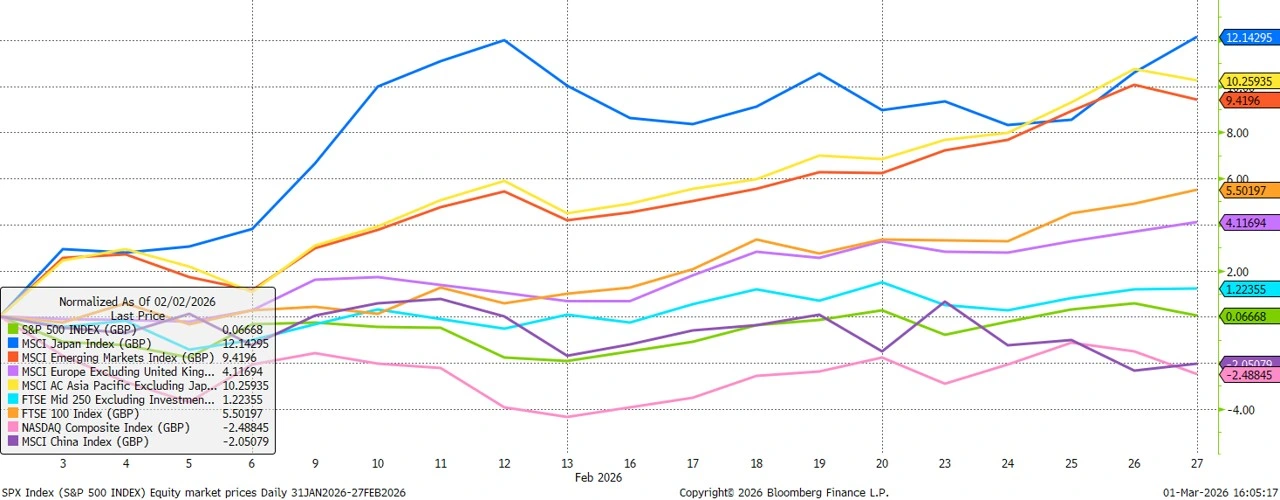

In GBP terms, Asian markets delivered exceptional performance during February, with Japan’s equity market surging 12.1% to claim the top spot among major regional indices. The Nikkei 225 reached a historic milestone of 59,000, propelled by Prime Minister Sanae Takaichi’s growth-oriented policies following her election victory. Foreign investors responded enthusiastically, purchasing a net ¥1.78 trillion ($11.5 billion) in Japanese shares and futures in the week ended February 13—the largest inflow since November 2014. Japanese chipmakers, defence contractors, and materials producers led the rally, with the top three performers in the MSCI World Index all being Japanese firms.

The broader Asian story was equally compelling. Asia ex-Japan gained 10.3%, posting its best February on record as investors piled into companies supplying artificial intelligence infrastructure. South Korea’s technology giants Samsung Electronics and SK Hynix reached a combined market capitalization of $1.14 trillion, surpassing China’s Alibaba and Tencent at $1.07 trillion—a symbolic shift underscoring how the AI boom has reshaped investment dynamics across the region.

By contrast, US equities struggled again. The S&P 500 Index gained a mere 0.1% in GBP terms, weighed down by a rotation away from mega-cap technology stocks as artificial intelligence enthusiasm cooled:

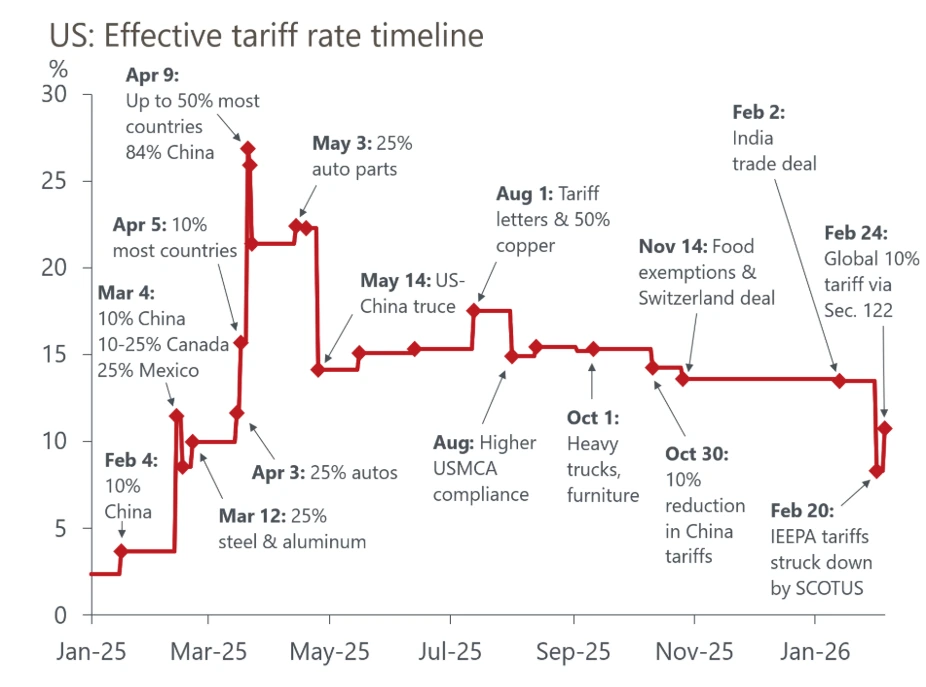

The month’s most significant policy development came on February 20, when the US Supreme Court struck down President Trump’s sweeping global tariffs in a 6-3 decision. Chief Justice John Roberts, writing for the majority, ruled that Trump had exceeded his authority by invoking the International Emergency Economic Powers Act (IEEPA) to impose “reciprocal” tariffs, stating that the Constitution reserves the authority over taxes and tariffs for Congress.

The immediate impact was substantial: the US effective tariff rate fell from 13.6% to 6.5%, with China emerging as a significant beneficiary as its fentanyl-linked and reciprocal tariffs were invalidated. Markets rallied on the news, with European shares hitting an all-time high and the S&P 500 rising as much as 0.7%:

However, the relief proved short-lived. President Trump immediately announced plans to impose a 10% global tariff under Section 122 of the 1974 Trade Act, later raised to 15%, effective for 150 days. Treasury Secretary Scott Bessent assured markets that tariff revenue would be “virtually unchanged” in 2026 as the administration invoked alternative legal authorities. The ruling also opened the door to a potentially prolonged battle over refunds, with as much as $170 billion in already-collected tariffs now subject to legal challenge.

UK investors faced headwinds from sterling weakness, which depreciated against all major developed and emerging market currencies during February. The pound fell by 1.5% against the euro, touching its lowest level in more than two months, and against the US dollar, sterling lost 1.3%, snapping a three-month winning streak.

The catalyst for sterling’s decline was twofold. First, the Bank of England came unexpectedly close to cutting interest rates, with a 5-4 split among rate-setters in favour of holding at 3.75%—far closer than the 7-2 outcome economists had anticipated. This fuelled bets on a March rate cut, with traders pricing roughly 60% probability. Second, domestic political turmoil intensified following various government scandals through the month, along with a Green Party by-election victory in Manchester, amplifying speculation about Keir Starmer’s future:

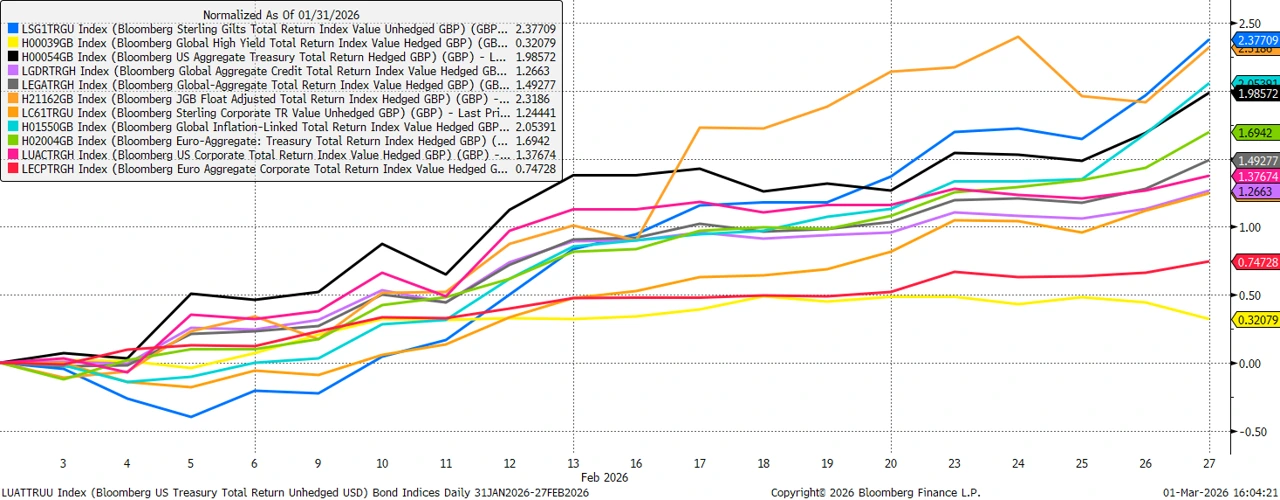

Bond markets reflected growing risk aversion, with government bonds strongly outperforming corporate bonds. UK Gilts delivered particularly strong returns, rising by 2.4% over the month following the BOE’s close rate vote, and as haven demand intensified amid souring sentiment toward risky assets.

US Treasuries rallied sharply as well, with the 10-year yield falling below 3.96%—the lowest in 6 months—and the 2-year yield reaching its lowest level since August 2022 at 3.37%.

UK gilts declined 6.1% in GBP terms despite initial gains The yield curve steepened as front-end gilts rallied on rate cut expectations while longer-dated bonds sold off on supply concerns.

Corporate bond markets proved resilient though less positive, the global high yield index rising by 0.3% over the month, reflecting continued risk appetite despite equity market volatility.

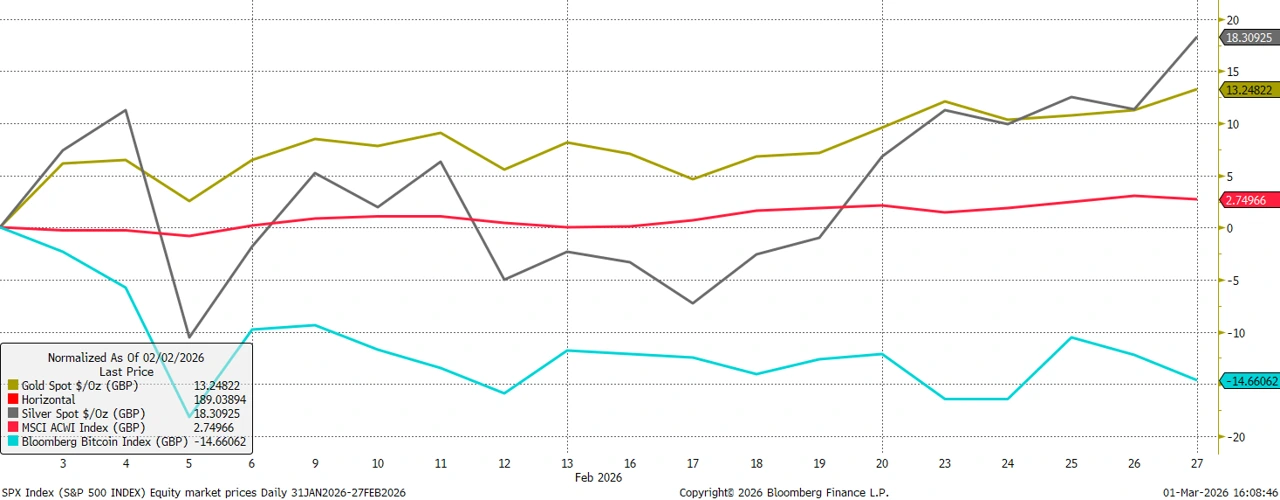

Precious metals posted yet more remarkable performance in February. Silver led the way with an 18.3% gain in GBP terms, extending its winning streak to 10 consecutive months, while gold advanced by 13.2%, posting one of its biggest monthly increases since January 2012.

The rally was driven by a combination of factors: early-month volatility that saw both metals register sharp drawdowns before dip-buyers returned, sustained retail demand despite price swings, and escalating geopolitical tensions as the month drew to a close:

The month ended with a dramatic escalation in Middle East tensions that has continued to dominate headlines into early March. On 1st March, Iran’s supreme leader Ayatollah Ali Khamenei was killed in coordinated US-Israeli airstrikes, marking a significant intensification of the conflict spiralling across the oil-rich region. President Trump stated that “heavy and pinpoint bombing” would continue throughout the week, while Iran responded with retaliatory missile attacks on Gulf nations.

The conflict has already begun disrupting traffic around the Strait of Hormuz, the critical shipping chokepoint through which roughly one-fifth of the world’s oil and liquefied natural gas flows. Oil prices, which had settled at around $73 per barrel before the attacks, have risen sharply through the first week of March, as investors assess and price in the higher risks to global energy supply.

The conflict introduces the risk of a prolonged period of elevated oil prices feeding through to broader inflation, potentially forcing central banks to maintain restrictive policy for longer than previously anticipated, or in a worst-case scenario, even consider tightening further despite slowing growth.

As we move into March, several themes warrant close attention. The durability of Asian equity outperformance will depend on whether AI infrastructure demand remains robust. The tariff landscape remains fluid, with the 150-day clock ticking on Trump’s Section 122 levies and ongoing legal battles over refunds. Sterling’s trajectory will hinge on BOE policy decisions and domestic political stability. Most critically, the Middle East conflict introduces significant uncertainty around oil prices and inflation, with potential ramifications for central bank policy globally.

For us as UK-based investors, February’s divergent performance across regions and asset classes underscores the importance of diversification and active currency management in navigating an increasingly complex global landscape.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: