Oliver Stone

April delivered broadly positive returns across risk assets, while fixed income markets experienced a more mixed environment as the ongoing tensions between the United States and Iran led investors to continually reassess the outlook for inflation and central bank policy. Reversing losses seen through March, equity markets benefited from resilient economic data and strong corporate earnings. Bond markets, however, exhibited greater divergence across sub-asset classes as shifting expectations around interest rates and economic growth drove volatility.

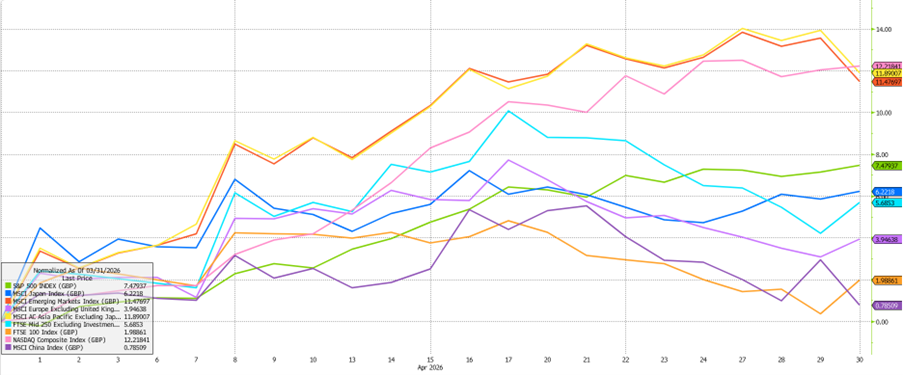

Despite tensions between the US and Iran continuing to dominate headlines, and the Strait of Hormuz remaining severely disrupted, risk sentiment improved across equity markets. Brent crude oil prices ended the month well above $100 per barrel, with ongoing ceasefire talks failing to result in a lasting agreement. Nevertheless, global equities delivered strong performance through the month, with continued economic resilience and positive momentum in technology-led sectors supporting renewed investor confidence rather than widespread risk aversion.

In the US, the S&P 500 rose approximately 7.5% in sterling terms, extending the strong performance seen earlier in the year. Markets were buoyed by robust earnings reports, particularly within the technology and financial sectors, alongside continued optimism surrounding artificial intelligence and technology investment. Large-cap technology stocks again led performance in the region, with the NASDAQ Composite rising 12.2% over the month.

Economic data in the US remained broadly supportive of equity markets. Recent figures suggest the US labour market remained stable through the first quarter, although weaker household spending and geopolitical uncertainty may influence firms’ hiring intentions and delay any meaningful acceleration in employment growth. That said, tax incentives have helped support consumer spending, offsetting some of the negative effects of higher fuel prices. Corporate earnings releases have also generally exceeded expectations. While inflation remains above central bank targets, it has moderated from its peak, allowing the Federal Reserve to maintain its current policy stance.

European equities also posted gains, although performance was somewhat more modest. The MSCI Europe ex UK index increased by roughly 3.9% in April. However, a slowdown in business activity across the region suggests that ongoing disruption in energy markets is beginning to feed through to the real economy, placing downward pressure on the region’s growth outlook.

The UK market lagged somewhat relative to its global peers, with the FTSE 100 returning approximately 2.0%. The UK market’s heavier weighting towards energy, materials and defensive sectors limited participation in the global technology rally. Financials also experienced increased volatility as rising UK inflation created uncertainty around the policy path of the Bank of England. Nevertheless, relatively attractive dividend yields and valuations continue to support investor interest.

In contrast, Asian and Emerging Market equities delivered particularly strong performance during the month. The MSCI Asia ex Japan index rose 11.9%, while the MSCI Emerging Markets Index gained 11.5%. Both regions benefited from improving sentiment towards regional growth and renewed investor interest in global technology supply chains. Investor sentiment towards emerging markets was also supported by a softer US dollar and stabilising growth prospects in several key economies.

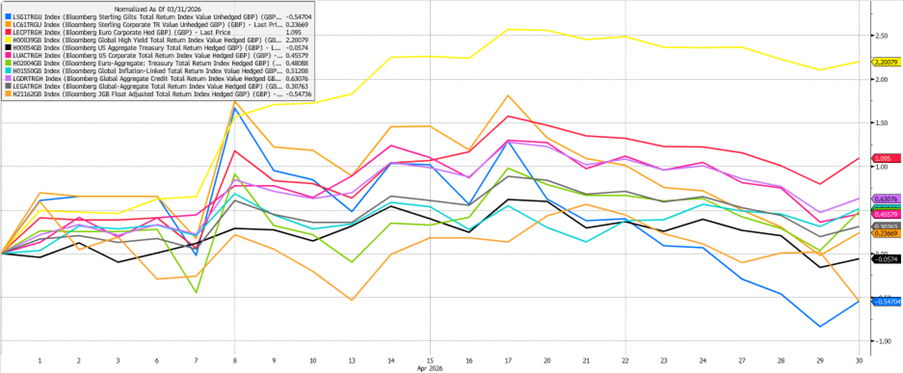

Within bond markets, the picture was more mixed as investors reassessed the timing and scale of potential interest rate cuts from major central banks. Global bond returns were modestly positive overall, delivering a gain of roughly 0.3%. This reflected a balance between strong corporate fundamentals and income generation, alongside continued fluctuations in government bond yields.

Shifting expectations around monetary policy were the primary driver of volatility across government bond markets. US Treasuries declined by approximately 0.1% during the period, as stronger economic data and persistent inflation pressures pushed yields higher.

UK government bonds also came under pressure, falling 0.5% as persistent inflation and growing political uncertainty dampened investor sentiment. Yields rose across the curve, with markets moving to price in additional rate hikes later this year.

Elsewhere, corporate bonds continued their strong run from earlier in the year, delivering steady outperformance as spreads remained relatively stable. The Bloomberg Global Aggregate Corporate Index returned 0.6%, with the improved risk sentiment that buoyed equity markets spilling over into credit.

Inflation-linked bonds also posted gains, reflecting sustained demand for inflation protection despite growing signs that headline inflation is gradually moderating.

Overall, while fixed income returns were relatively muted compared with equities, the asset class continues to provide an important source of diversification and income. Yields remain significantly higher than those seen during the ultra-low interest rate environment of the past decade, improving the long-term outlook for bond investors. However, as uncertainty around inflation and interest rates persists, active asset allocation remains increasingly important to manage risk and ensure that fixed income continues to serve its role within diversified portfolios.

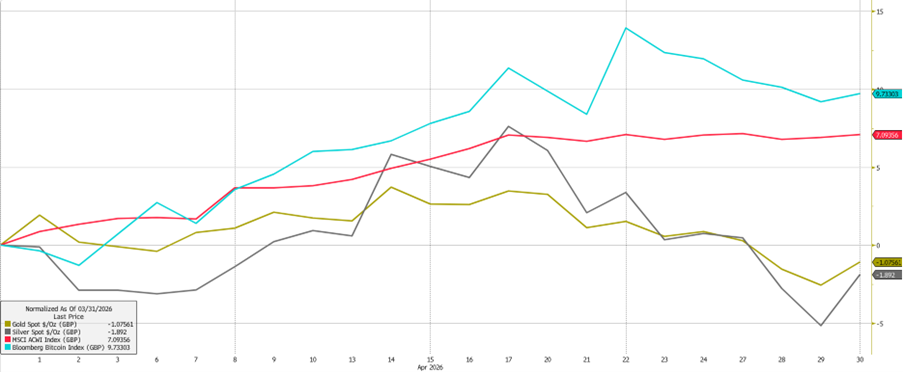

Commodity markets delivered mixed performance over the period. Shifting inflation expectations weighed on gold, leading to some easing in prices. In contrast, higher oil prices provided support to the broader commodity index, while strengthening demand for raw materials – driven in part by the global buildout of AI data centres – underpinned industrial metals.

Looking ahead, markets will remain focused on inflation trends, central bank policy signals and the sustainability of corporate earnings growth. While volatility may persist as geopolitical developments lead investors to adjust expectations around interest rates, the broader economic backdrop remains relatively supportive. As always, disciplined portfolio construction and a long-term investment perspective remain central to navigating evolving market conditions.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: