Market Updates

Oliver Stone

April 2025 was a month marked by significant volatility and uncertainty across global financial markets. The primary driver of this turbulence was the announcement of sweeping tariffs by the US administration, which had far-reaching implications for trade, economic growth, and investor sentiment.

Global equity markets experienced substantial swings throughout April. The initial tariff announcements on April 2nd triggered a global sell-off, with US stocks plunging by over 10% at one point and a surge in the VIX volatility index. However, markets calmed later in the month after some US policy moderation and better-than-feared corporate earnings results. The S&P 500 ultimately closed down around 4% in GBP terms, while the tech-heavy NASDAQ outperformed despite starting the month weakly, falling by 2.5%. Ex-US developed markets outperformed strongly as capital flowed towards the UK, Europe, and Japan, continuing the trend of the previous three months. China, seen as the nation worst affected by US policy, was the weakest in GBP terms:

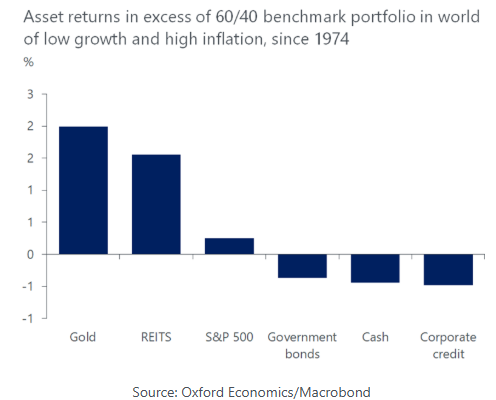

Gold performed exceptionally well in April, rising by more than 5% in GBP terms (black line above). Gold’s role as a safe-haven asset was reinforced by broader economic uncertainties and geopolitical tensions, with investors continuing to turn to the precious metal as a hedge against potential market downturns and inflationary pressures. The chart below shows the performance of various asset classes relative to a standard 60/40 equity/bond portfolio during periods of low growth and high inflation since 1974, and clearly illustrates that gold has consistently outperformed other asset classes in those periods, achieving the highest positive returns. In contrast, assets like the S&P 500 and government bonds have struggled, often showing negative or minimal returns.

Currency markets were also strongly impacted by the tariff announcements, with movements here being a key component of equity returns when translated back into GBP. The US dollar, which would usually be expected to appreciate in an uncertain macroeconomic environment, sold off heavily vs all major currencies; the black line below charts the performance of the dollar index (DXY) which is a trade weighted index of developed market currencies vs the USD. Over April this gauge fell by 7.%, with notable underlying drops vs the Euro and Yen.

Global government bond markets saw initial rallies into the teeth of April’s uncertainty, followed by a concerted sell-off as investors priced in additional inflation concerns linked to the impact of US tariff policies. Some recovery was seen later in the month as policy moderated, but per the chart below, investment grade and high yield corporate debt underperformed government bonds over the month, while US assets underperformed European and UK counterparts. Despite signs of growth weakening in the US, the Federal Reserve has been clear that they won’t cut rates until the weakness is apparent in macroeconomic data due to inflation risks. This means less positivity at the margin for US bonds:

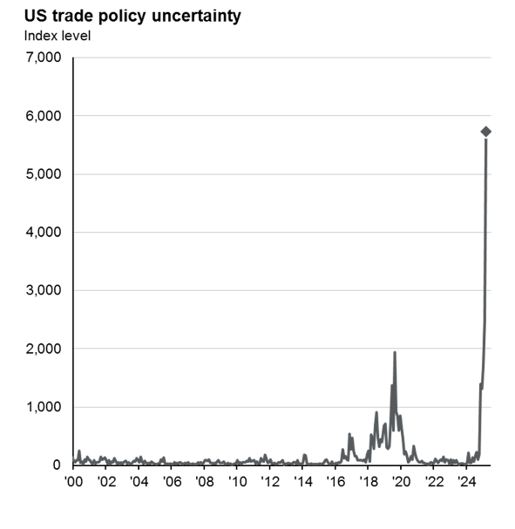

As mentioned above, one of the key themes in April was the impact of US tariff measures on the global economy. Observed levels of US trade policy uncertainty were extremely high as the chart below shows, and this uncertainty is expected to persist into the third quarter of 2025, adding to concerns about a potential growth slowdown, especially as the full shock from tariffs hasn’t fully hit macroeconomic and earnings data yet:

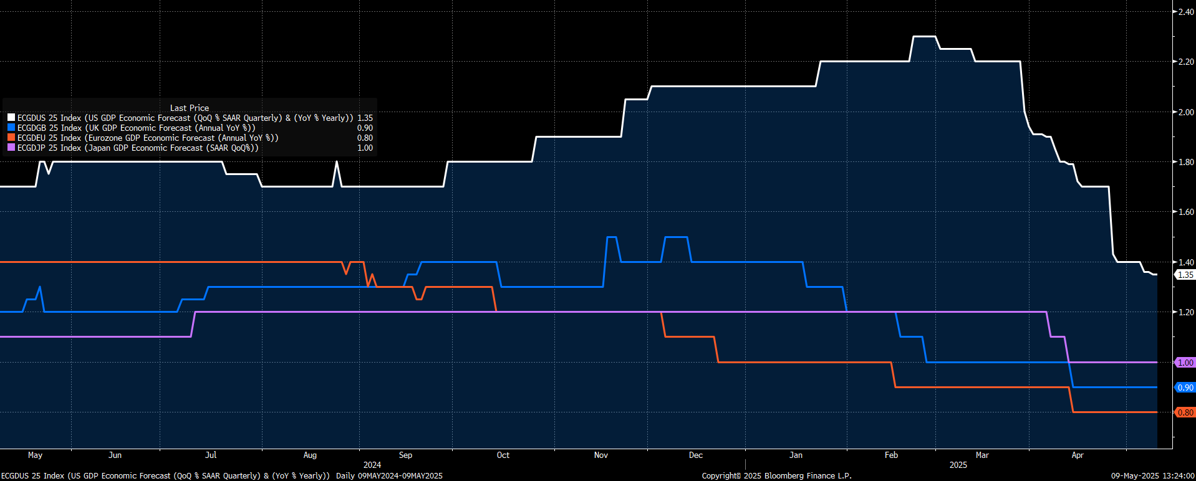

Economic indicators such as GDP growth and inflation trends have shown mixed signals. The final chart below shows market consensus 2025 GDP forecasts for the US (white), UK (blue), Eurozone (orange) and Japan (pink), with all to a greater or lesser extent having been downgraded since the start of the year. The US GDP growth forecast has suffered particularly heavily, falling from a relatively robust peak of c.2.3% in February 2025 down to 1.35% today, with the trajectory still downwards. This decline underscores the challenges faced by the US economy and others in maintaining growth momentum amidst external pressures.

Looking ahead, financial markets’ drivers are expected to remain complex and dynamic, with several key factors shaping the investment landscape; most prominently the ongoing impact of US tariffs will continue to influence global trade policies, creating uncertainty and potential volatility. Additionally, central bank actions, including policy adjustments and rate cuts, will have significant implications for various asset classes. Understanding the direction of monetary policy will be important to adjust strategies accordingly.

As always, portfolio diversification will be crucial in mitigating risks associated with market fluctuations and economic instability. By adopting a strategic approach that emphasises diversification, we can help to guide you through these uncertain times and ensure that investment portfolios are well-positioned for long-term success.

To take a deeper dive into the update, listen to our Market Update podcast. In this episode, we explore April’s market performance highlights and discuss the broader economic developments that shaped investor sentiment, including government policy shifts and central bank responses around the world.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: