Oliver Stone

December wrapped up a volatile year with a mix of resilience and rotation.

Outside the US, equity markets finished 2025 on a firmer footing: European and UK equities moved higher in December, helped by their bias toward banks, materials and other “old economy” sectors.

The FTSE 100’s full year story was particularly strong, chalking up its best annual gain since 2009 as investors rewarded cash generative franchises and dividend depth.

By contrast, the US stalled into year end.

In local currency, the S&P 500 was broadly flat for December, but translated returns were softer in sterling as the dollar weakened yet again.

A late month wobble in mega cap technology stocks hurt returns, reminding investors that market leadership can change quickly when valuations are rich and positioning crowded.

![]()

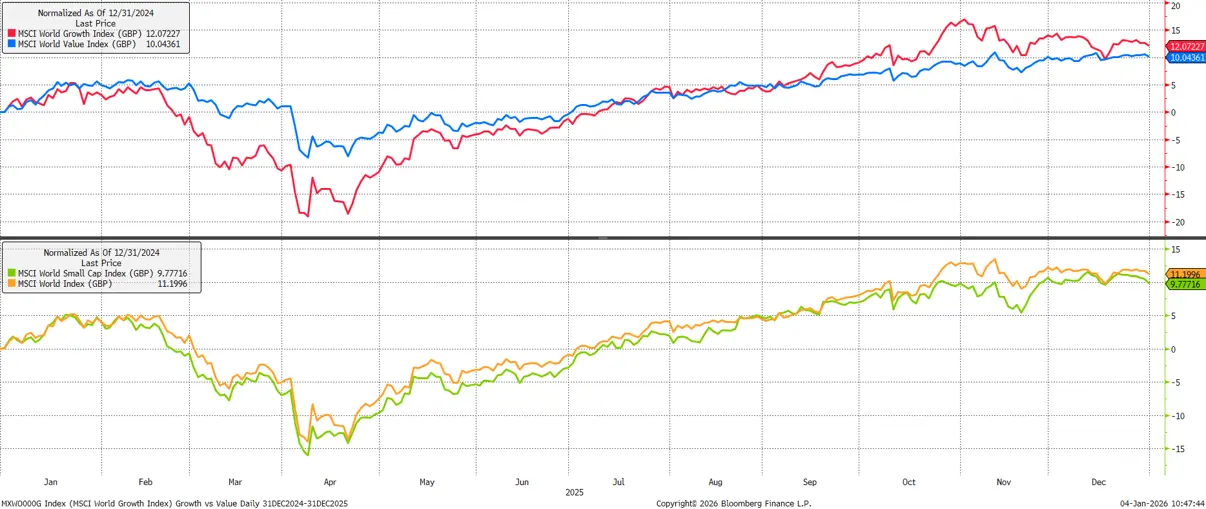

Under the surface, factor signals told a similar tale as in November.

Value stocks outpaced growth counterparts again in December – partly a function of profit taking in the AI complex, partly the straightforward arithmetic of lower multiples.

Small caps were marginally ahead of large caps over the month, but the bigger picture across 2025 was one of convergence: both value and growth ended the year with similar headline returns, even though the value path was less bumpy, proving the importance of diversification:

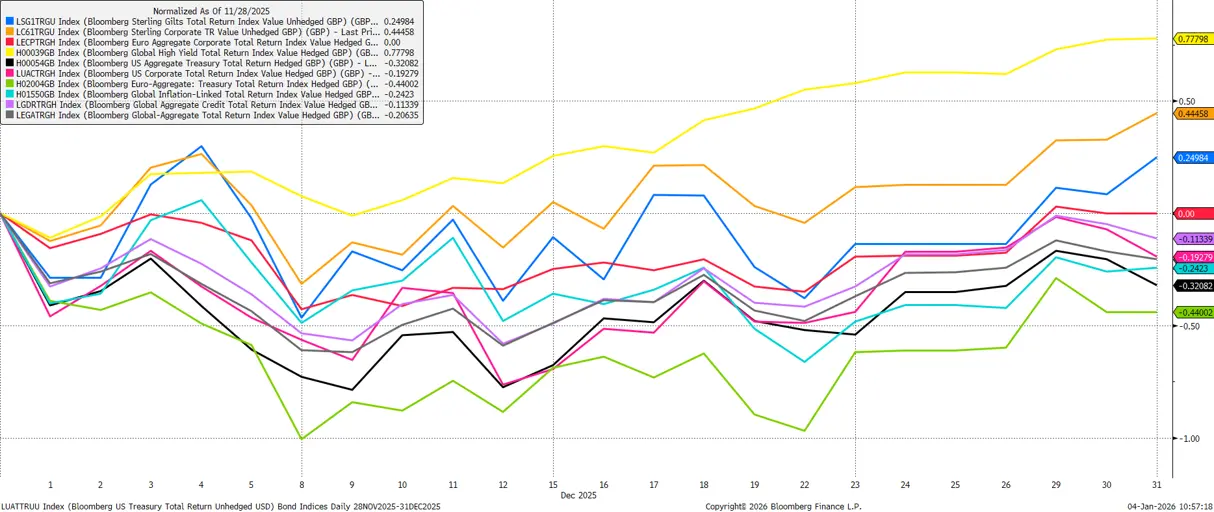

Fixed income had a constructive month particularly in the UK.

Gilts rallied as two things broke in their favour: the Bank of England cut Bank Rate by 0.25% to 3.75%, and November inflation surprised meaningfully to the downside versus consensus expectations.

Neither move was a shock in isolation, but together they sharpened the market’s focus on a gradual, data dependent easing path rather than a race to the bottom.

Credit outperformed government bonds through December, consistent with the late cycle pattern we’ve seen most of the year.

And for 2025 as a whole, bond portfolios did what you’d want in a normalising environment: they earned their keep mostly via income rather than capital appreciation:

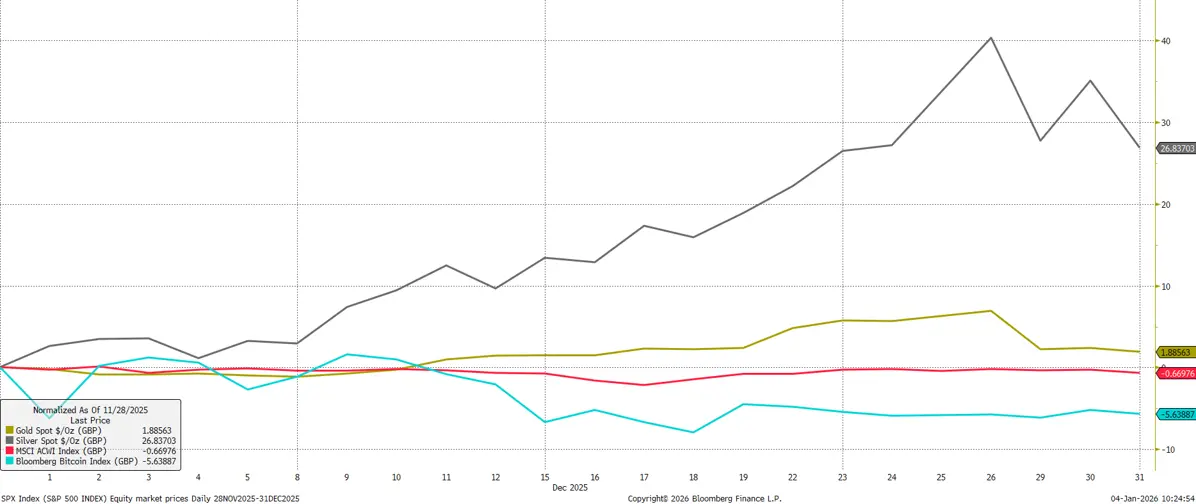

Commodities were the standout yet again in December, with precious metals firmly in the spotlight.

Gold made successive record highs and briefly traded above $4,500/oz late in the month; silver’s move was even more dramatic, with a near vertical December that put the closing price around $72/oz and cemented eye catching full year gains of close to 150%.

The drivers are familiar – central bank buying, geopolitical hedging, and, for silver, tight physical markets and strong industrial pull – but the scale of the move forces the risk conversation.

These are useful hedges in the current macro regime, but position sizing needs to respect the higher volatility reality after such outsized returns:

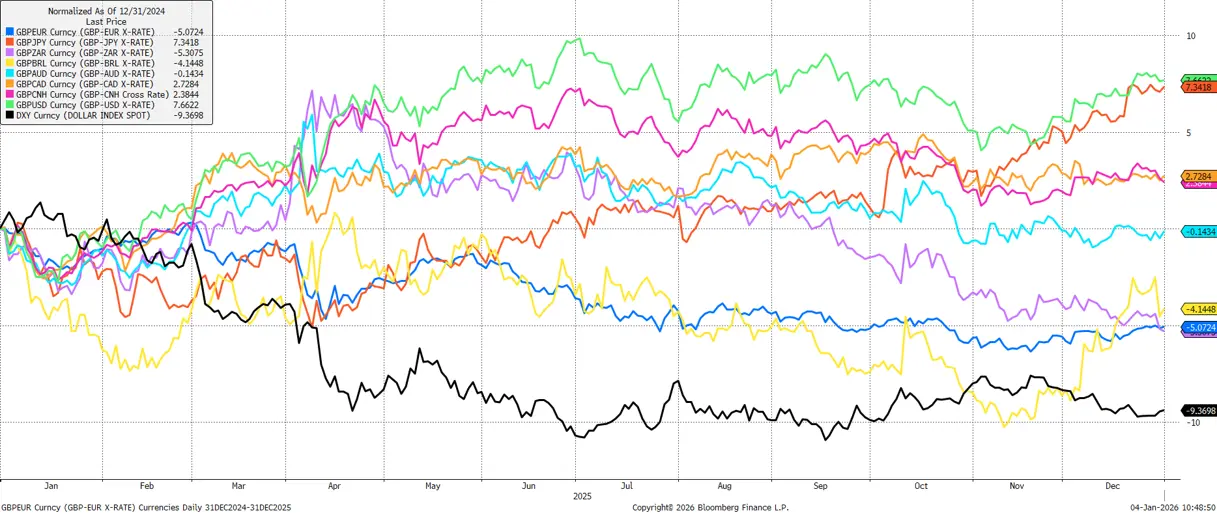

Currencies did their part to shape relative performance.

Sterling strengthened into year end, rising against both the dollar and the yen.

The dollar’s weakness shaved translated US equity returns, with the yen’s slide similarly framing Japan’s softer equity outcome in December.

That yen move was not one way traffic, though, and it arrived alongside an important policy inflection: the Bank of Japan raised its policy rate by 25bp to 0.75%, the highest in three decades.

The message from Tokyo was normalization, not tightness – real rates remain significantly negative – but the signal matters for global asset pricing.

JGB yields edged up, carry strategies re priced at the margin, and investors were reminded that Japan’s regime is moving, even if slowly:

On the policy front elsewhere, December offered clarity with caveats.

The Federal Reserve delivered a third straight 25bp cut, taking the funds rate to 3.50%–3.75% and pairing it with language that was, by design, a shade hawkish.

Minutes made the split obvious: some officials want to guard against an inflation re acceleration, others worry more about a cooling labour market, and both camps prefer to see cleaner data after autumn’s federal government shutdown before committing to a faster path.

In the UK, the BoE’s 5–4 vote to cut underscored a similar balance – disinflation progress is real, but services inflation and the 2026 wage round keep caution front and centre.

The ECB stayed on hold and described policy as “in a good place,” a sensible stance given its updated forecasts and the risk of reading too much into short term resilience.

Inflation prints supported the drift lower without suggesting the job is finished.

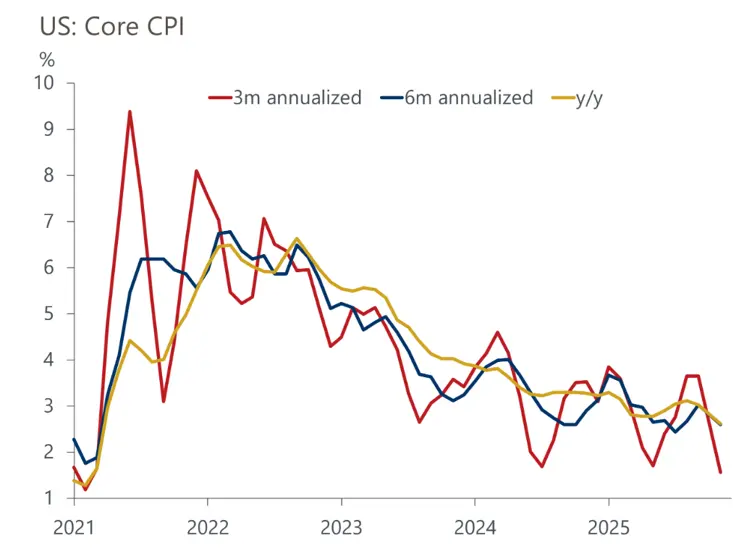

US headline CPI came in at 2.7% year on year with core at 2.6%, the softest pace since 2021; the UK’s November CPI fell to 3.2%, below the Bank’s forecast, with goods disinflation and food prices doing the heavy lifting while services remained stickier.

Both sets of numbers help rate cut narratives, but both are still above target, and both were produced in a year that had sizable data quirks.

The upshot: progress is there; complacency isn’t warranted:

Macro growth data paint a picture of resilience with cooling edges.

The US entered December with robust Q3 GDP and better than expected payrolls, but higher unemployment and a more cautious consumer mix kept markets honest.

Europe’s growth profile remains slower and more uneven, though the equity uplift reflected a different composition story – less exposure to stretched tech, more exposure to sectors that benefit from real assets, capex, and pricing power.

The UK economy remains subdued, but the combination of lower inflation, supportive policy, and equity sector biases was enough to lift domestic benchmarks into year end.

Geopolitics stayed in the background but influenced hedging behaviour.

Energy chokepoints and broader regional tensions didn’t disrupt supply chains meaningfully in December, yet they reinforced the bid for safe haven assets and raised the premium investors place on portfolio insurance.

Policy uncertainty arguably mattered more: the prospect of Fed leadership transition in 2026, the legal trajectory of US trade levies, and the evolving stance on fiscal discipline in several jurisdictions are all live issues for rates, FX and sector dispersion.

The common thread through December is that the macro is getting easier to live with – lower inflation, gentler policy, broader equity participation – but not easy enough to jettison discipline.

Valuations are elevated in pockets, data is still normalizing, and geopolitics can change the narrative quickly.

Portfolios that stayed diversified in 2025 were rewarded. Portfolios that stay selective in 2026 should continue to be.

As we head into 2026, there are reasons for continued optimism: inflation is easing, interest rates should drift down gradually, and growth will likely be positive across regions and sectors, if not stellar.

That mix favours a well diversified portfolio – balancing risk exposures to buffer against any unpleasant surprises that will undoubtedly occur as we move through the year.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: