Market Updates

Harry Scargill

March 2025 brought significant volatility across global markets, shaped by intensifying trade tensions, divergent central bank policies, and mounting recession concerns. Investor sentiment deteriorated as the US administration dramatically expanded tariffs targeting multiple trading partners, while fiscal developments in Europe and the UK highlighted contrasting approaches to economic challenges. The combination of increasing protectionism, sticky inflation, and slowing growth created a complex environment for investors navigating an increasingly uncertain global landscape.

Equities faced the brunt of the growing uncertainty around global trade and economic growth. major indices such as the S&P 500 extended their February correction, losing 8% in March, heavily impacted by technology and cyclical sectors reacting to escalating tariff threats and policy uncertainty. European equities also weakened, with the MSCI Europe index declining by -3.2%, driven by sluggish regional growth and heightened US trade tensions. Germany’s substantial fiscal stimulus announcement later in the month provided partial relief, particularly benefiting defence and infrastructure-related stocks.

In the UK, the FTSE All Share fell -2.6%, though larger-cap stocks provided relative resilience due to exposure in banks, defence, and commodities. Japanese equities fell by -3.6%, while broader Asian sentiment was mixed. Notably, Chinese equities held up well, losing only -0.5% despite ongoing trade concerns.

Bond markets saw volatility throughout March but held up relatively well, helped by a rally across most major indices in the final week. US government bonds gained 0.2%, as recession fears drove Treasury yields lower in a flight to safety and a repricing of Federal Reserve rate cuts this year. In Europe, bonds reacted negatively to Germany’s announced, “fiscal bazooka,” pushing Bund yields sharply higher towards 3%, and causing European government bonds to lose -1.7%. UK gilts also declined, by -1.2%, despite the Bank of England’s cautious easing stance.

Despite broader market volatility, corporate bonds displayed notable resilience, highlighting selective investor confidence in credit quality amidst macroeconomic uncertainties.

Currency markets reflected the broader themes playing out across economies in March. The US dollar weakened against all major currencies, as investors reassessed the demand for US assets given trade uncertainty and a weaker economy leading to more rate cuts. The Pound also weakened against the Euro, given the comments made above about how European Central Bank rates might also stay higher, alongside a stronger German economy at the heart of the region.

Trade policy dominated economic discussions in March, with the US administration aggressively expanding its tariff regime. Having already implemented tariffs against China, Canada, and Mexico in February, President Trump ordered a 25% tariff on autos and auto parts on March 26, effective April 3.

Initial tariffs announced on March 4 were somewhat watered down after negotiations, but tariff rates on US imports from Canada and Mexico have still ended up at double-digit levels. The market currently assumes 25% tariffs will be reimposed in April on imports from Canada and Mexico (with a lower 10% tariff on Canadian energy) alongside the steel, aluminium and China tariff.

Taken together, the overall US effective tariff rate is expected to significantly rise from its previous level – a dramatic shift that reverses several decades of trade globalisation. Markets are now bracing for further potential escalation, with additional “reciprocal tariffs” expected to be announced in early April, following what Trump describes as the United States’ “Liberation Day” on the 2nd. Investor concerns extend beyond the blunt tariffs currently being enforced or threatened, particularly given the ongoing uncertainty surrounding their exact nature, with plans appearing to shift almost daily. This volatile environment makes it extremely difficult for businesses and consumers to plan effectively, leading to delays in capital expenditure, hiring, investment, and broader spending. Such hesitation may result in knock-on effects further down the line.

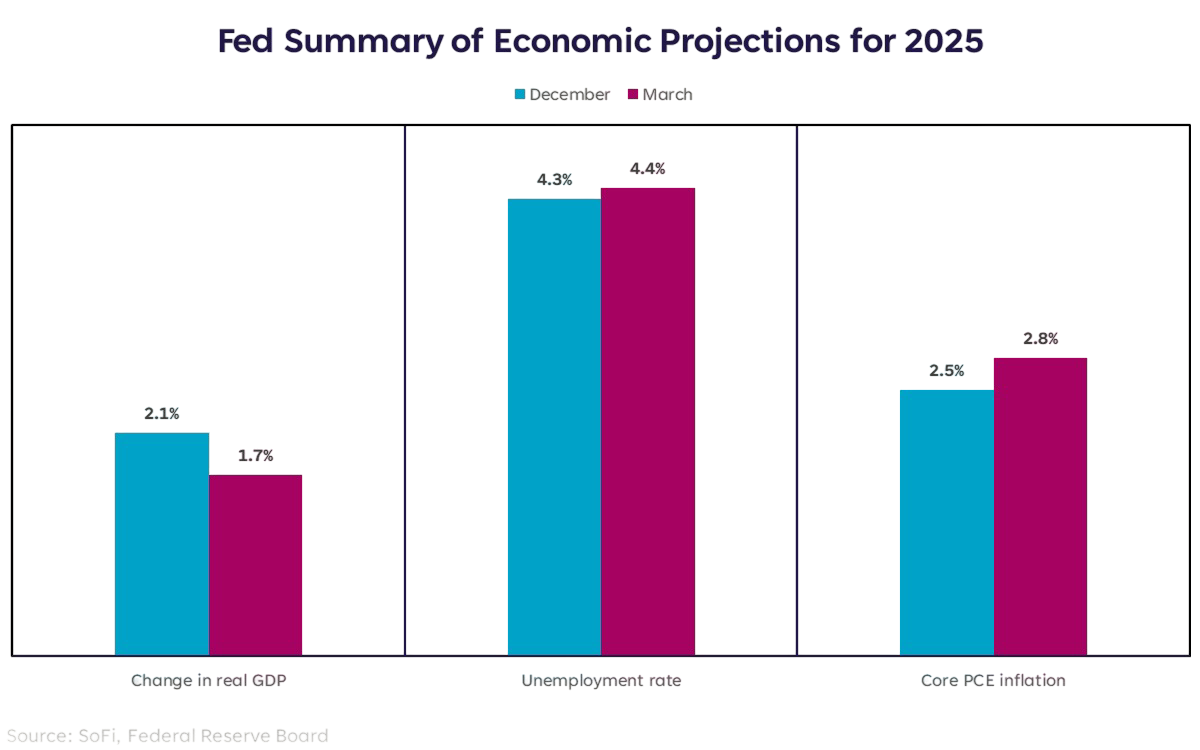

All this uncertainty is already beginning to weigh on business and consumer confidence, as well as broader economic projections. In the Federal Reserve’s March meeting, they updated their projections for the end of 2025, shown below, lowering growth, while rising the rate of inflation and unemployment. However, it is important to note that these levels are still far from forecasting a recession and independent from political noise would be considered healthy.

March brought a paradigm shift in European fiscal policy, centred on Germany’s massive stimulus announcement. The incoming CDU-SPD coalition government proposed an unprecedented fiscal expansion that quickly earned the nickname “fiscal bazooka”. The package totals approximately €500 billion (12% of 2024 GDP) and represents a dramatic departure from Germany’s traditional fiscal conservatism.

The plan includes widening the structural deficit allowed under Germany’s constitutional debt brake, exempting defence spending above 1% of GDP from deficit calculations, and creating a massive infrastructure fund outside the scope of the debt brake. This would fund a substantial increase in defence spending from just 1.3% of GDP in 2021 to around 3% by 2027, alongside accelerated €100 billion investment in transport, energy, and digital infrastructure.

This fiscal expansion is deemed significant enough to transform Germany’s economic outlook. Economists have substantially revised their projections upward, now expecting GDP growth to average 1.8% over the next four years – 0.7 percentage points higher than forecast just a month ago. However, this fiscal expansion also raises inflation concerns for the region.

The UK Spring Statement, delivered on March 26th, revealed a challenging economic outlook and limited fiscal flexibility. The Office for Budget Responsibility cut its 2025 GDP forecast to 1.0% (from 2%), though it projected improvement from 2026 onward with growth of 1.9% in 2026, 1.8% in 2027, 1.7% in 2028, and 1.8% in 2029.

Inflation is expected to follow a complex path – having fallen to 2.8% in February (the lowest since the inflation surge began), it’s projected to rise again to 3.8% by July before averaging 3.2% overall for 2025. The forecast then shows inflation falling to 2.1% in 2026 and reaching the Bank of England’s 2% target in 2027.

Chancellor Rachel Reeves announced approximately £10 billion in fiscal tightening to address a £14 billion deterioration in public finances since the October Budget. Despite this adjustment, fiscal headroom remains limited at just £9.9 billion – leaving little margin for error if economic conditions deteriorate further. Reeves also announced several spending priorities, such as defence expenditures and building social and affordable housing.

The global market and economic environment we find ourselves in presents a complex mix of challenges and opportunities. Escalating trade tensions, persistent inflation concerns, and mounting recession fears create headwinds, yet selective opportunities exist across asset classes for investors.

The key to navigating this uncertain landscape lies in diversification, across geographies, asset classes, sectors, and investment styles. By maintaining a balanced approach, focusing on quality, and remaining tactically flexible, investors can position portfolios to weather potential volatility while capturing opportunities as they emerge.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: