Oliver Stone

May 2026 was anything but dull. The Iranian conflict that began in March continued to cast a long shadow over virtually every asset class; driving energy prices, bond yields, currency moves and central bank rhetoric in ways that continue to make life complicated for investors.

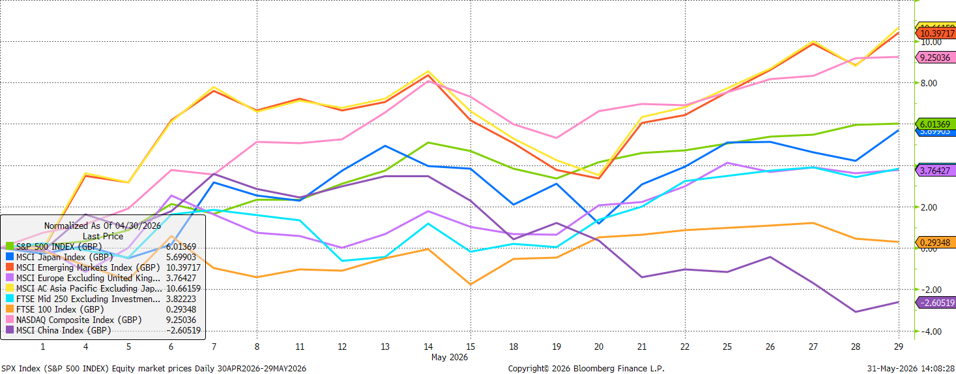

The headline story in equities was a remarkable run for US stocks. The S&P 500 notched its ninth consecutive weekly gain by the end of May – a winning streak not seen since 2023 – powered by a near-20% rally from its March lows. The engine behind this was a combination of AI enthusiasm and hopes that a ceasefire deal with Iran could reopen the Strait of Hormuz. Companies like Dell and AMD delivered strong earnings and upbeat outlooks, and Micron crossed the $1 trillion market cap threshold, adding further fuel to the tech-driven narrative.

Global markets broadly followed suit. The MSCI All Country World Index hit record highs, and Asian markets were particularly strong – South Korea’s Kospi has now surged around 100% this year alone, making it the world’s best-performing major equity index, driven by its semiconductor and AI-supply-chain exposure – despite a 25% drawdown in March. It’s up more than 250% in the last 12 months!

Japan’s Nikkei also had a standout week early in the month, jumping 6% as it caught up after a public holiday.

European equities had a trickier time, showing a much stronger negative correlation with oil prices than global peers, meaning every price spike hit European stocks harder. With oil prices ranging between roughly $90 and $115 per barrel through the month, that created real headwinds for continental markets. For UK investors, the FTSE’s energy-heavy composition offered some natural buffer, but the domestic political backdrop (more on that below) kept a firm lid on any enthusiasm.

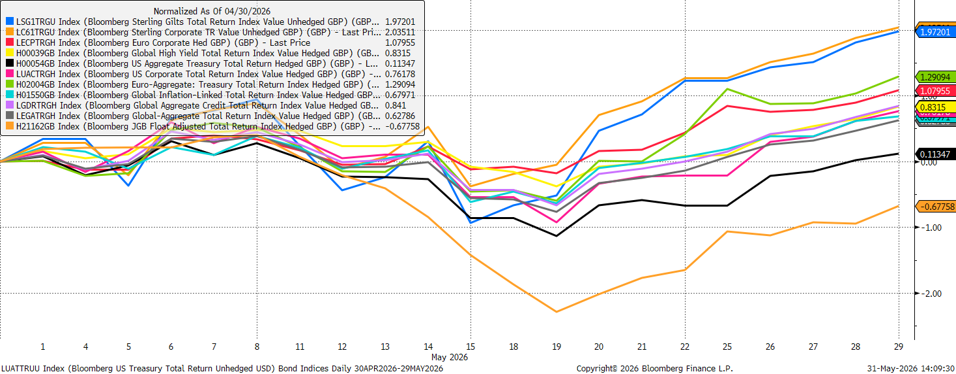

If equities were the good news story, bonds were the uncomfortable one. Government debt sold off sharply across the developed world, with the US 30-year Treasury yield touching 5.20% mid-month – its highest level since 2007. The US 10-year yield rose around 6 basis points over the course of May to close near 4.45%, having briefly topped 4.68% at its worst point.

The UK was not spared. Early in the month, 30-year gilt yields surged to 5.78% – a level not seen since 1998 – as energy-driven inflation fears collided with domestic political uncertainty. The 10-year gilt briefly topped 5.10%.

Bond yields did pull back from their peaks in the final two weeks of the month as ceasefire hopes calmed nerves somewhat. UK 10-year real yields ended May broadly flat on the month at around 1.45%, while US real yields rose 17 basis points over May to 2.05% in a meaningful tightening of financial conditions.

The Bank of England (BoE) held its base rate at 3.75% and the debate within the Monetary Policy Committee was fascinating. Governor Andrew Bailey signalled the Bank could tolerate inflation running temporarily above its 2% target given the softness in the real economy, provided second-round effects don’t materialise. MPC member Alan Taylor suggested that simply holding rates at current levels may be enough to do the job. But Catherine Mann offered a starkly different view, warning that the era of “good luck” on inflation is over and that a more shock-prone world is here to stay. Markets ended the month pricing around 0.60% of BoE rate hikes by year-end, which is a significant shift from where expectations sat at the start of the year.

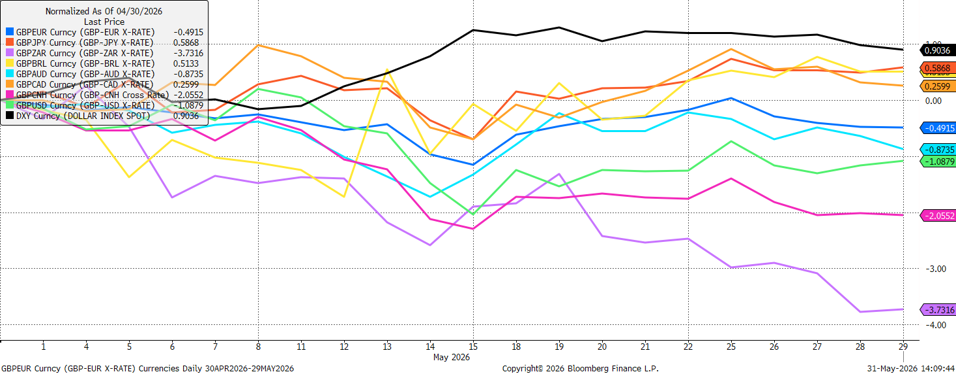

In currencies, it was a more difficult month for the pound, which fell by around 1.1% vs the US dollar over May – its largest monthly decline since March. US dollar strength was the primary driver early on, moving higher as oil prices pushed US inflation expectations higher, but sterling had its own domestic headwinds too.

Labour’s bruising defeat in local elections at the start of the month triggered a wave of calls for Keir Starmer to resign, and the emergence of Manchester Mayor Andy Burnham as a potential leadership challenger prompted bearish moves within the pound currency complex.

The pound did recover some ground in the final two weeks, driven by Iran ceasefire hopes, and as some of the political noise faded. Against the euro, UK political risks continued to keep GBP on the back foot. For UK investors with overseas assets, the weaker pound was actually a tailwind as it boosted the sterling value of overseas holdings.

Commodities: Oil Dominates, Gold Pulls Back

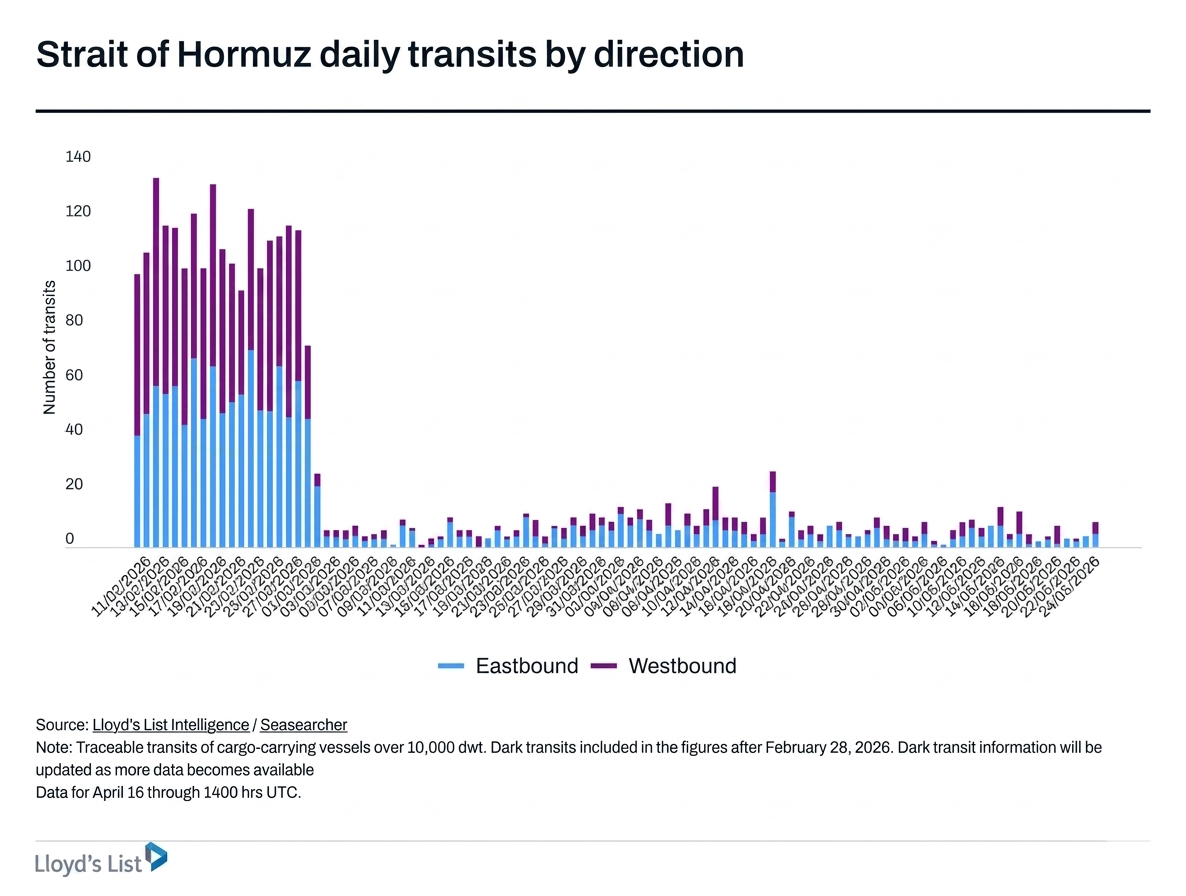

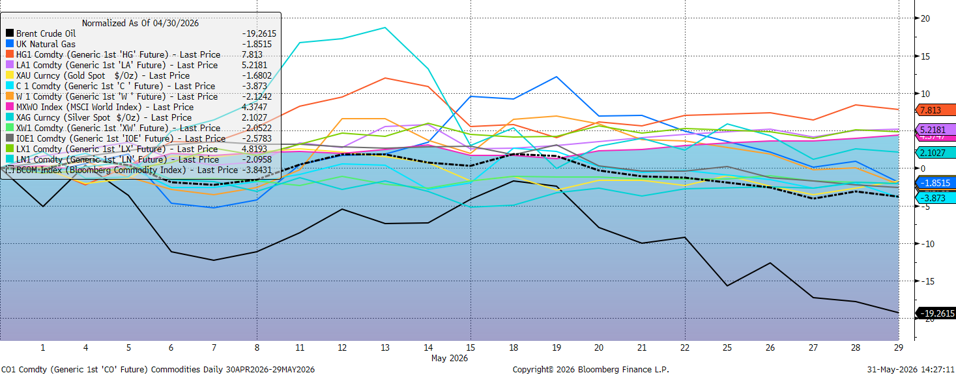

Oil was once again the commodity story of the month. The price of Brent Crude fell by around 19% during May but as mentioned above has been trading in a wide $90–$115 per barrel range since March, with every twist in the US-Iran negotiations sending prices sharply in one direction or the other. With the Strait of Hormuz still effectively closed, global inventories have been drawing down rapidly.

Gold had a more complicated month. Having traded above $4,750 early in May on optimism around Iran peace talks, the precious metal fell to a two-month low around $4,390 later in the month as fresh US-Iran strikes boosted the dollar and pushed investors toward oil and cash rather than bullion. It recovered to around $4,530 by month-end as oil prices eased on ceasefire hopes. The relationship between gold and oil has been somewhat inverted this cycle; when oil spikes, the dollar tends to strengthen, which weighs on gold even as inflation fears rise.

The thread running through all of this is energy-driven inflation and what central banks do about it. US PCE inflation hit 3.8% year-on-year in April – the highest level since 2023 – and US consumer sentiment fell to a record low. The US Federal Reserve is in a difficult spot: markets expect it to act if inflation expectations drift further, but rate hikes into a slowing consumer backdrop carry their own risks. The UK faces a similar dilemma, with April CPI at 2.8% and a labour market that showed signs of softening in April.

For investors, while equity markets have been particularly strong over the last two months, how the Iran situation resolves (or doesn’t) will likely define the investment landscape for the rest of the summer and beyond, and is unsurprisingly what we are heavily focused on monitoring in the months ahead.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: