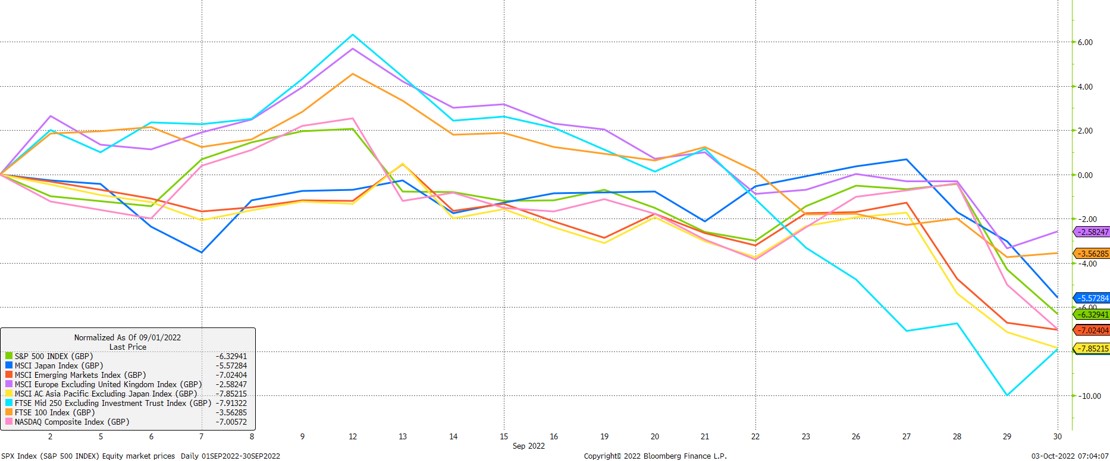

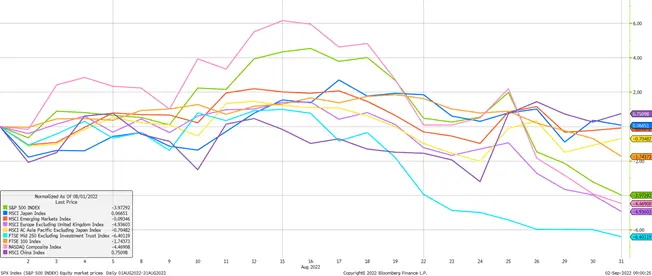

As the first chart below shows, all major equity regions were negative in pound terms, with European and UK large-cap stocks faring best, while emerging market, Asian and UK mid-caps were worst:

Over the year-to-date, UK large-cap equities in the form of the FTSE 100 index remain standout performers in relative terms. The second chart below shows that despite their making a loss of 6.6%, this is far in advance of most other major indices, with European equities for example falling by more than 19% over the same time period. As we have commented before, this phenomenon has occurred due to a combination of the FTSE 100’s international focus, and its composition leaning more towards cyclical sectors, particularly energy:

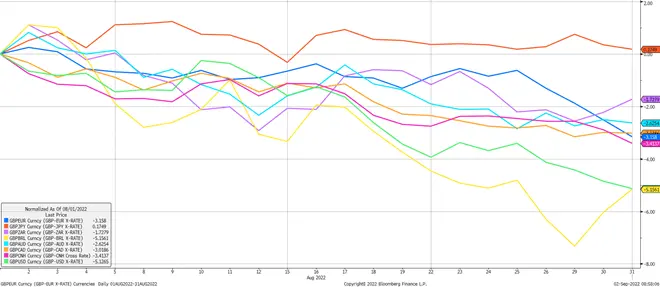

The outperformance of UK equities is even more stark when viewed in local currency terms – i.e. unadjusted for the pound’s weakness. Again, this is something we have commented on several times through 2022, but it bears repeating how significant the pound’s weakness has been. The third chart below shows the scale of international equities’ underperformance when viewed in this way; UK investors have been well shielded from this due to the pound:

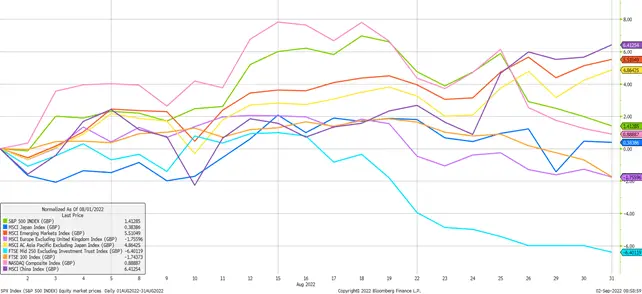

UK equities’ outperformance is all the more impressive given the domestic machinations that have occurred during September and October. Following the now ex-Chancellor, Kwasi Kwarteng’s, ‘mini-budget’ on 23rd September, we saw astonishing levels of volatility in UK government bond and currency markets, which has almost immediately started to impact the wider economy.

The Government’s announcements did not entirely come out of the blue. Measures to cap energy prices for consumers and businesses had long been expected, as had some notions of fiscal easing elsewhere, but on the day and subsequently, two aspects caught investors by surprise: the scale of the intended action, and the lack of balancing measures to fund it.

The energy package alone was expected to cost up to £150bn over its two-year duration, though given the volatility of natural gas prices, this figure is, in reality, open ended. Additionally, Kwarteng presented a reversal of the previous increase in national insurance contributions, the removal of the top rate of tax, a cut to the basic rate of income tax and a cut to stamp duty, amongst various other measures. On top of that, over the subsequent weekend, he explicitly stated that he expected to deliver further tax cuts in the near future.

Crucially, this was all to be met by massive, increased borrowing, at a time where interest rates are rising, and global central banks, including the Bank of England are turning increasingly hawkish to combat high and sticky inflation.

The Government chose not to involve the Office for Budget Responsibility (OBR) in this first instance, apparently keen to front-load its policy agenda. This meant that no independent analysis was provided as to the impact of these measures on the outlook for government debt sustainability. Perhaps not surprisingly then, these factors combined to produce the moves seen in the last week of September and into October, with the Bank of England (BoE) forced to rapidly intervene in size to stop the Gilt market from seizing up.

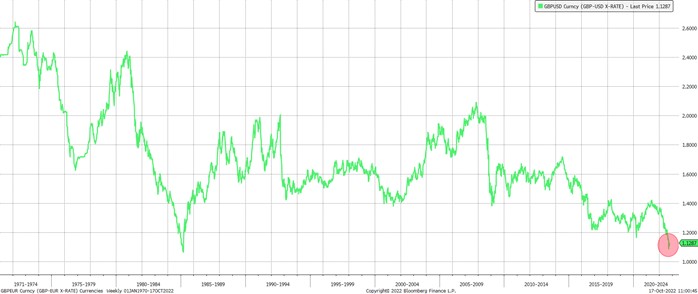

Starting with the pound, the chart below shows its performance versus the US dollar in 2022, with the red oval highlighting the period following the mini-budget. The pound has been on a downwards trajectory versus the dollar this year, along with many other currencies, but this most recent move has been out of kilter with other competitors, reaching a new all-time intra-day low on 26th September:

This is better viewed in a long-term context, whereas can be seen, the pound now trades versus the dollar at a level not seen since the mid-1980s:

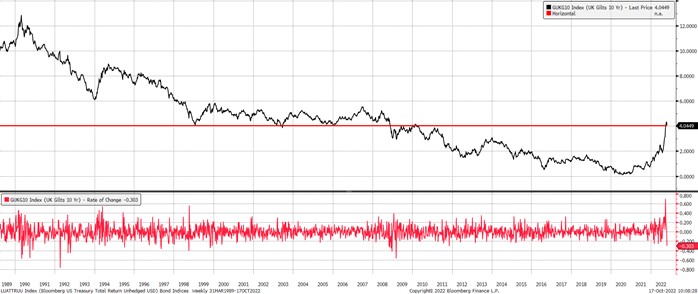

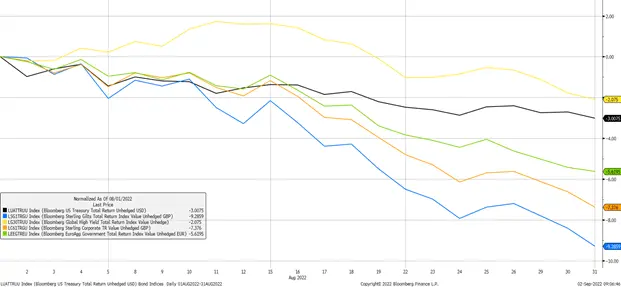

In fixed income markets, Gilts have seen truly extraordinary moves. The top panel of the chart below plots the yield of the 10-year Gilt from 1989 onwards, with the red horizontal line showing that today’s yield is now back to levels not seen since 2008. The bottom panel of the chart shows the rate of change of the 10-year Gilt yield, where it can clearly be seen that at no point in this data series’ history have larger short-term shifts been seen:

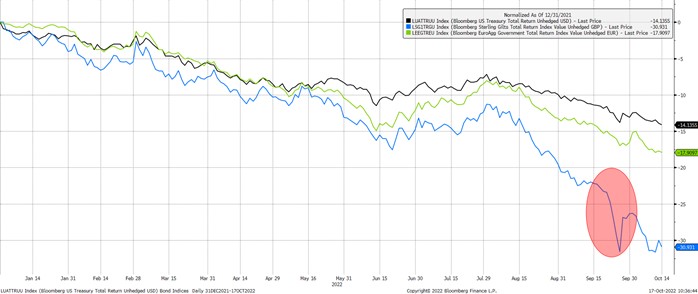

That on its own is dramatic enough but given the very low starting point of this recent upwards move in yields, and therefore with a very high level of duration, or interest rate risk, baked in, when translating the change in yields to price movements, we can see that substantial losses have occurred, per the next chart.

This shows the broad Gilt index in blue through 2022, with equivalent government bond indices for the US (black) and Europe (green) also plotted for context. Despite the recovery since seen due to the Bank of England’s intervention, Gilts have fallen by nearly 31%, with much of that loss suffered in a very short space of time:

As mentioned above, the BoE were forced to step back into the Gilt market to ensure its stability, committing to buying up to £10bn of Gilts and index-linked Gilts every day until 14th October, in a return to emergency quantitative easing in all but name.

This action was required as parts of the UK defined benefit pension market saw highly stressed conditions relating to their holdings of long-dated Gilts; without this intervention they faced a potentially acute funding crisis related to the very sharp price falls illustrated above.

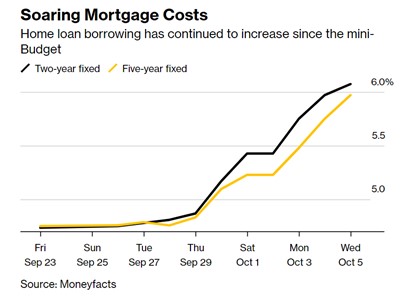

In terms of further real-world impacts, we have already observed that mortgage rates are very sharply rising due to the rise in government bond yields, with a 2-year fixed rate mortgage now costing more than 6% for the first time since November 2008, and a 5-year fixed rate mortgage nearing the 6% mark.

Similar moves have been seen in the corporate lending space, with companies looking to issue new debt facing much higher rates of repayment than just a month ago. While the BoE’s intervention has calmed the worst of the market’s nerves, these higher rates will have a negative impact on future demand:

Events have been especially fluid over the past few weeks. The extent of the market moves above and the pressure this placed on the new government led first to a U-turn on the elimination of the top rate of income tax, followed closely by the sacking of Chancellor Kwasi Kwarteng on 14th October, and the appointment of Jeremy Hunt in his place.

Then, on 17th October, an astonishing emergency statement was made by the new Chancellor (the fourth in 2022), which essentially reversed all of the planned measures introduced by the Prime Minister in September, bar two: the abolition of the health & social care levy (cut to National Insurance) and the cuts to stamp duty.

Hunt announced that corporation tax would now be rising in April 2023, the basic rate of income tax would not be falling to 19%, and would stay at 20% ‘indefinitely’, and, most significantly for consumers, that the energy price guarantee would now only run in its current, open-ended form until April 2023. After this point, a new scheme would be put in place to better target those who need the support.

Financial markets’ reaction to this series of U-turns, culminating in the near-complete reversal of the mini-budget, has been positive, with Gilt yields moving down from their peaks, and the pound making something of a recovery against other major currencies.

The road ahead remains uncertain however, with plans still needing to be announced on identifying deliverable spending cuts, and with consumers and businesses now potentially exposed again to extremely high energy prices next year assuming no change in circumstances in energy markets or a resolution in eastern Europe.

Politically the UK’s future is more uncertain, with the credibility hit to the UK and its assets undeniably large. Shockwaves from the internal fallout will spread far from here and may raise questions about the long-term viability of the government.

It has already been suggested that Prime Minister Liz Truss is now a lame duck after just 40 days in power, with others waiting in the wings to take control. Should this happen, we suspect it may just raise more questions – can the UK be led by another unelected leader, or should there be a general election?

We expect there will be more twists and turns in the weeks to come, but for now we certainly welcome the hint of stability in the pound and Gilt yields that we currently see on our screens. As always, though, the need for portfolios to be well diversified is absolutely critical to avoid any over-exposure to one particular market.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

After musing last month as to whether July’s positivity was a ‘relief bounce’ rather than the beginning of a sustained recovery, August’s price action provided little evidence to confirm the latter at the expense of the former.

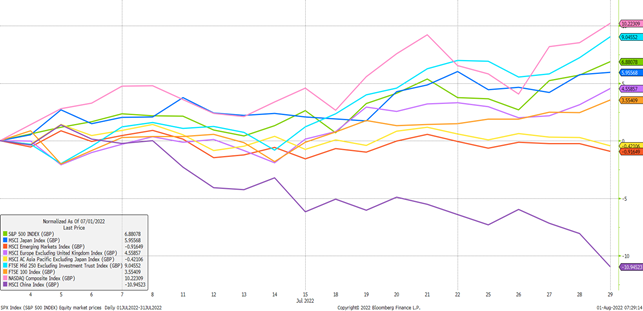

Equity markets held steady for the first half of the month before beginning to roll over as the first chart shows below in local currency terms. Continuing the back-and-forth theme of this year, Asian and emerging market equities were once again the relative winners versus developed market equities. The MSCI China index rose by 0.75%, dragging the broad emerging markets and Asian indices with it, though both recorded small losses.

Japan was by far the best of the developed markets, eking out a 0.07% gain, while US and European indices were further behind, falling by 3.97%-4.93%. The UK saw its large-cap FTSE 100 index performing relatively well, while its mid-cap, domestically focused FTSE 250 more losses, reversing its more positive July in dropping by 6.40%:

However, for UK investors, this chart doesn’t tell the full story. Again continuing one of 2022’s themes, the second chart below shows that the pound fell precipitously versus all major currencies bar the Japanese yen during August; including by more than 5% against the US dollar:

This meant that when equity returns were translated from local currency back into pounds, the results were markedly different as the third chart shows. Returns almost across the board were positive, with only the UK and European indices still languishing in negative territory.

The pound’s weakness came even as the Bank of England’s (BoE) Monetary Policy Committee (MPC) raised interest rates again by 0.5% in their ongoing attempt to bring inflation under control. In theory, this action should have provided some support for the pound, however in making their rate hike decision the BoE made a number of additional pronouncements that undermined this support, expressing worries over the potential for entrenched high inflation, forecasting a recession in 2023, and announcing a reversal of its quantitative easing programme from September onwards.

The bank has been unusually and not always helpfully forthright in its communications this year, with other major central banks striking more nuanced tones.

Bond markets suffered another tumultuous month as central banks remained resolutely hawkish; indicating their willingness to risk damaging economies to bring down inflation. Towards the end of the month, the US Federal Reserve Chair Jerome Powell made his eagerly anticipated annual speech at the Jackson Hole Economic Symposium in Wyoming, where he unambiguously stressed the importance of inflation control, and stated that he was prepared to use the central bank’s toolkit ‘forcefully’.

These comments impacted equity markets as seen above but also bond prices as can be seen below. In both cases, investors had been cautiously pricing in the start of a central bank ‘pivot’ away from its current trajectory – a notion that was firmly put aside by Powell. Government bonds were particularly badly affected, with UK Gilts falling by more than 9% during August, European government bonds by 7.38% and US Treasuries by 3.00%. All eyes will now be on monthly inflation data as to central banks’ next moves:

Building on the points we made in last month’s note, as we move into the autumn and winter months, we would caution on the outlook for risk assets should the economic situation deteriorate further from here, despite equity market valuations already looking attractive. Without substantial government intervention consumers and businesses will face a squeeze on incomes and margins due to high inflation; particularly with regards energy prices in the UK and Europe.

Consumers will need to make hard spending choices, with signs that personal debt is already increasing in response to price rises, while businesses will be forced to internalise additional costs themselves or try to pass them on to consumers, resulting in an unpleasant negative feedback loop.

Of course, nothing is certain, and there are many distinct possible pathways from here through to 2023 and beyond. From this month, the UK has a new Prime Minister who has a singular opportunity to enact radical supply side reforms which could be the catalyst to recovery – we hope to be pleasantly surprised.

In light of these risks, as always we would encourage diversification across portfolios, particularly as we look ahead towards the colder months.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

Equity markets furnished investors with some better news through July as we saw a concerted recovery most notably in those developed markets that had previously struggled in 2022. As the first chart below shows, the tech heavy NASDAQ and the midcap biased FTSE 250 were strongest, rising by 10.2% and 9.0% respectively, with other developed markets arranged behind them also generating positive returns:

We don’t yet know how sustainable this recovery in developed market equities is, but for now, it has the feel of a ‘relief bounce’ given the swathe of negativity we’ve seen. Over the past few weeks, markets have begun to react less negatively to poor macroeconomic data and hawkish central bank news; an indication that relatively bearish expectations may already be priced in to a certain extent. This being said, there are still clear reasons to remain cautious.

In contrast to June, Asian and broad Emerging Market indices were relative laggards, falling by 0.4% and 0.9% respectively. This underperformance was driven by Chinese equity losses of 10.9%, erasing last month’s stellar outperformance. Despite some positivity in China around Covid reopenings and the potential for stimulus to be brought forward, volatility is persisting because risks still remain to that more positive view.

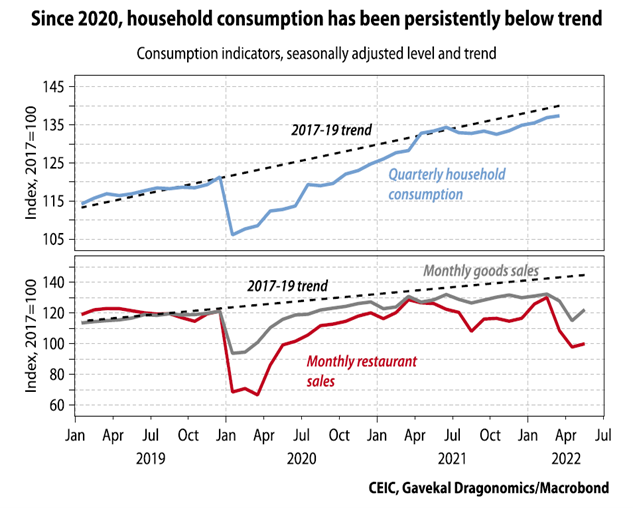

The authorities are still persevering for now with their ‘dynamic zero-Covid’ policy, which is proving a barrier to full recoveries in consumer spending and the labour market.

In the second chart below we can see aggregate household consumption in the top panel still firmly below its trend, whilst the bottom panel highlights more granular weakness in consumption data relating to goods and restaurant sales which have also fallen away again recently:

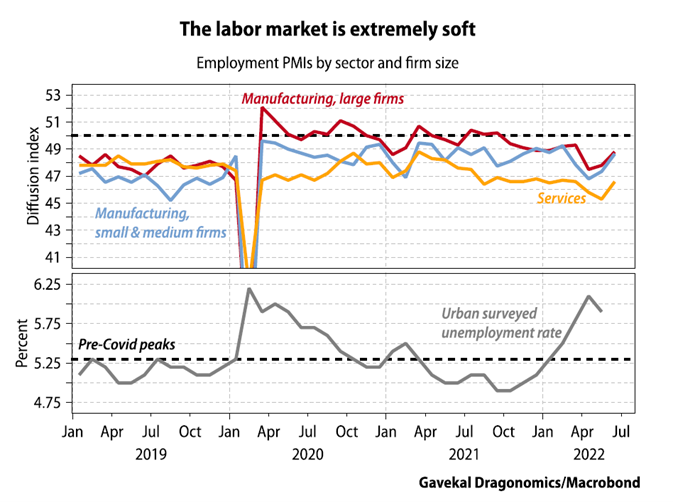

The third chart below shows the state of the Chinese labour market. The top panel shows employment survey data for manufacturing and services companies, with each of the survey components indicating that employment has been in contraction now for several months. Indeed in the case of services and small & medium sized manufacturing businesses, the contraction has been extensive.

As a corollary, the unemployment rate in the bottom panel shows a substantial rise in 2022, the effects of which have included increased consumer uncertainty, dampened confidence and impaired spending plans:

Geopolitical machinations in Taiwan may distract from the domestic picture temporarily, but it is clear that mounting economic uncertainty means investors are now looking for clearer signals on policy, which are yet to emerge after the Politburo’s quarterly economic meeting in July.

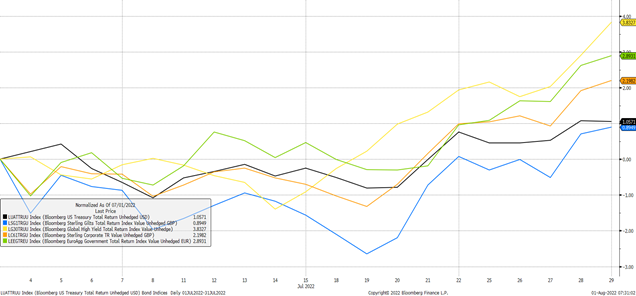

Bond markets also saw a welcome recovery in prices across the board in July, with riskier parts of the credit market outperforming government bonds as the fourth chart below shows. Global high yield bonds and sterling corporate bonds rose by 3.8% and 2.2% respectively, whilst UK Gilts rose by 0.9%:

These positive returns may seem strange given the prevailing central bank narrative is very much geared towards higher interest rates and generally tighter monetary policy to combat inflation, but as indicated above, it has been a change in market expectations that has driven this change in price action.

We do, however, think there are a number of risks to the market’s current viewpoint.

The first and most obvious risk is that inflation can still surprise to the upside, and for now does appear to be doing so. Even though the headline rate will probably moderate by the end of this year, it will still be very high, and many component parts of the inflation basket appear to be rising in a persistent manner. The US Federal Reserve made it very clear at their most recent meeting that they will be data dependent in terms of their rate hiking cycle from now, meaning that if inflation prints are worse than expected in the coming months, markets will need to readjust their expectations.

Second, wages are still rising strongly in nominal terms, if not currently in real terms, and the longer this persists, the greater the risk of sticky or persistent inflation. In the US, employment costs rose more than expected in Q2 by 5.3% y/y, which again implies the possibility of a more hawkish Federal Reserve. Here in the UK, we have the threat of more strike action across multiple sectors unhappy with their pay settlements.

Finally, a more negative scenario centred around Russian energy supply is still on the table. European countries, particularly Germany, are preparing for a full removal of supply which would require huge fiscal support and energy rationing into the winter. While that doesn’t sound immediately bullish for inflation, the rises that would be seen in various prices, combined with massive fiscal support would see a shift in market expectations.

In light of these risks and in spite of the more recent positivity, we would encourage diversification across portfolios, particularly as we look ahead towards the colder months.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Equity and bond returns swung back into negative territory through June as uncertainty around Ukraine continued to weigh on sentiment. In addition, investors voiced increasing concerns around rapidly tightening global monetary policy, high inflation and historic lows in consumer confidence surveys.

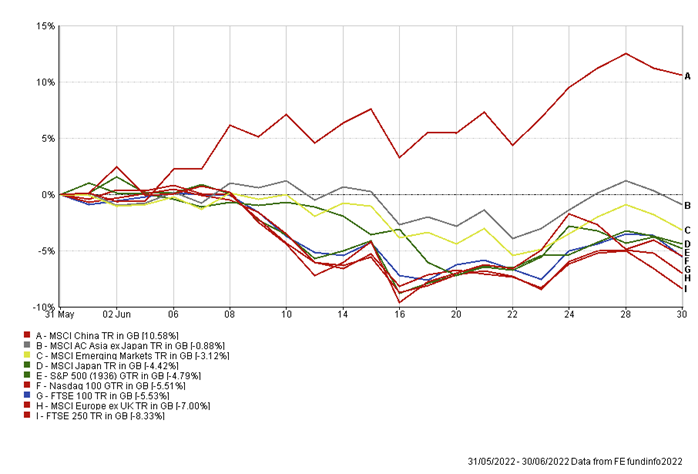

As the first chart below shows, developed market equities in particular struggled, with the large-cap European, Japanese and US indices falling by 7.0%, 4.4% and 4.8% respectively in pound terms. UK equities struggled this month; the FTSE 100 index lost 5.5% and the mid-cap FTSE 250 8.3%, affected by its more domestically focused composition:

Asian and broader Emerging Market equities were relative outperformers over the month, boosted by extremely strong performance from Chinese stocks which rose by 10.6% over the month (chart). These outsized gains come as a welcome relief to the weakness seen earlier in the year as numerous major cities suffered through Covid lockdowns. At one point in March 2022, the MSCI China index was down by nearly 30% in pound terms – it has subsequently recovered to be down just 0.5%.

Investors’ confidence in Chinese equities has been severely tested over the last year. Growth in China has deteriorated due to the Government’s zero-Covid policy, regulatory crackdowns across a swathe of diverse industries and weakness in the real estate sector.

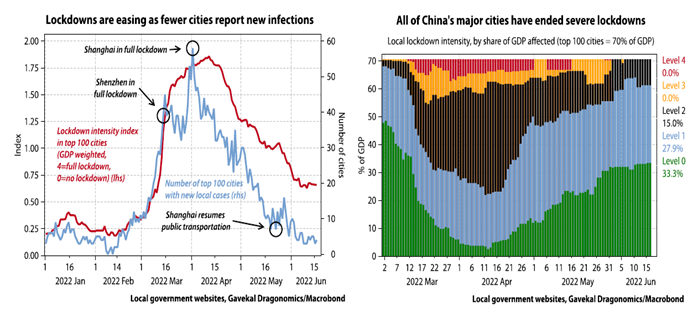

While restrictive Covid policy remains a risk, for now at least the picture has calmed, with the charts below showing that lockdown ‘intensity’ has significantly receded in recent weeks as new infections have fallen.

Importantly, the chart on the right shows that no cities are currently under the harshest Level 3 or 4 lockdowns as imposed on Shanghai earlier in the year:

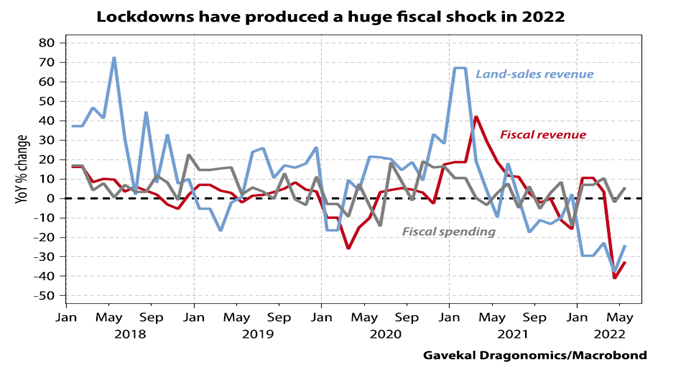

Additionally, it now seems that the Chinese authorities are ramping up fiscal and monetary stimulus after an initially lacklustre response. Extremely weak labour market data as a direct result of lockdowns has bled into consumer spending numbers, the impact of which has been a huge fiscal shock as tax revenue has plummeted per the chart blow.

In response to this, various fiscal and monetary measures are being enacted to boost growth through the remainder of 2022 and 2023. This presents an interesting counter-cyclical opportunity for investors relative to developed markets, which in general are only just beginning their respective slowdowns:

Developed market government bonds suffered another month of negative outturns as illustrated below. UK Gilts fared worse realtive to US and European counterparts, but the performance differential was much narrower than last month, with something of a recovery in prices being seen from mid-month onwards.

The US Federal Reserve remains committed to bringing inflation down, raising rates by 0.75% in June and expected to do similar in July. The Bank of England also raised rates by 0.25% to 1.25%, again citing the delicate balance between inflation management and economic growth.

The European Central Bank remains stuck at rock bottom levels, though has guided towards a first rate hike in July. Again, the ECB is stuck between a rock and hard place, with the rate of inflation still increasing month-on-month and ahead of expectations, reaching 8.6% in June, while the fragility of individual nations’ debt pictures is still very much apparent.

After a tough first half of 2022, July will be pivotal for the future direction of markets amid corporate earnings data, key inflation numbers and further central bank meetings. Should we see surprises to expectations, we would expect volatility to persist. As always, this speaks to the importance of diversification within portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

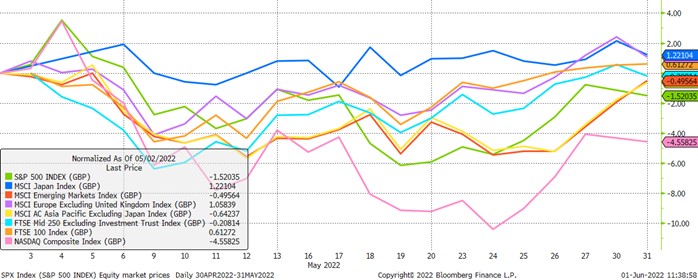

Equity and bond returns were muted again through May as uncertainty around Ukraine and Chinese Covid lockdowns were the predominant narrative drivers. The first chart below shows global equity indices over the month in pound terms, with developed markets generally outperforming emerging markets. This was despite a strong rally into the end of the month for the latter group, driven by a recovery in Chinese stocks as the authorities continued to signal support for an economy battered by extremely harsh and increasingly irrational lockdowns:

Japanese and European equities were strongest with returns of 1.2% and 1.1% respectively, while US equities fared worst as richly valued technology stocks were shunned by investors, exemplified by the Nasdaq’s 4.6% fall. Investors here are still coming to terms with the highly inflationary environment in combination with a much more hawkish Federal Reserve which insists it will seek to aggressively combat inflation and inflation expectations with tighter policy.

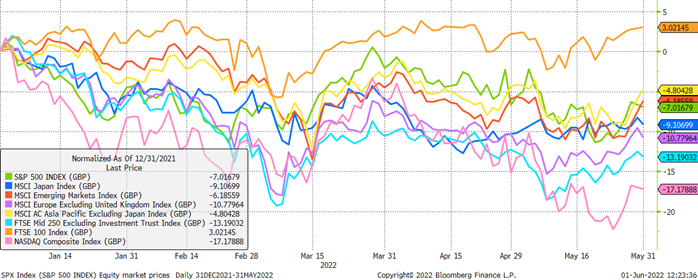

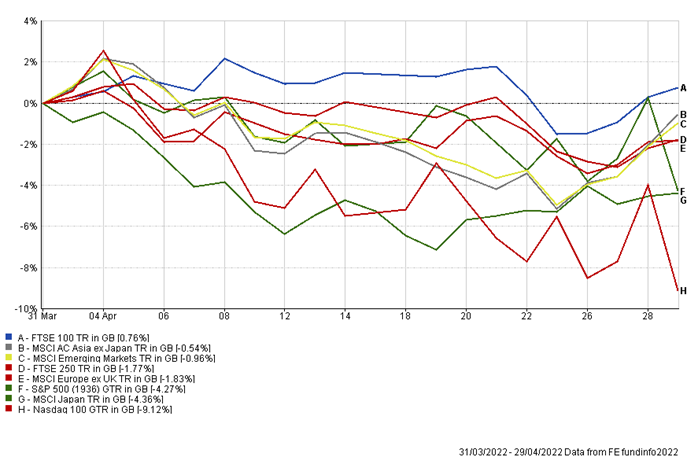

The FTSE 100 posted another positive return of 0.6% to continue a fine run of form in 2022. As the second chart below shows, the UK large-cap index is the standout performer amongst the major global indices, rising by just over 3%, versus -7% for the S&P 500; this in spite of a much weaker pound benefitting the translated returns of overseas equity investments.

The index is heavily tilted towards beneficiaries of the current macroeconomic environment, with more than 40% of its members sitting in the energy (13%), materials (12%) and financial (16.5%) sectors; weightings that are at odds with other developed market indices in particular. In previous years this has hindered relative performance, but in the face of significant commodity supply chain disruption and rising interest rates, it is proving to be an optimal mix:

The strong relative performance for the FTSE 100 has come as the UK economy has begun to struggle under the weight of a dual slowdown in consumer and business activity amidst very high inflation – 9% in April – and geopolitical uncertainty. To illustrate this, the FTSE 250 index of mid-cap, more domestically focused UK companies has struggled this year, falling by 13.2%. The Bank of England’s latest forecasts paint a gloomy picture of the year ahead, with Governor Andrew Bailey’s comments on the Bank’s ‘helplessness’ in combating inflation highlighting the difficulties facing the economy.

In response to the increasing cost of living crisis centred around energy prices, Chancellor Rishi Sunak unveiled a new package of financial support for households worth in the region of £15bn (0.6% of GDP) and weighted towards those households in most need of relief through the colder winter months.

However, alongside the additional spending, the Chancellor introduced a controversial, temporary windfall tax on energy companies’ ‘excess profits’; a measure that he had repeatedly criticised in the months leading up to the plan’s announcement, having previously argued that the obvious impacts of a windfall tax would be to deter investment, undermine competition and kill off jobs.

The levy is expected to raise £5bn in tax revenue this year, offsetting just one third of the Government’s planned outlay, and further, in direct contradiction to its intention, has already resulted in business investment plans being placed on an uncertain footing per comments from BP immediately following the announcement.

The UK is certainly not alone in its cost of living crisis driven by high energy prices, and now joins many European countries in providing fiscal handouts to struggling consumers. But, rather than simultaneously encouraging investors to pour much-needed capital into the oil and gas sector to combat Russia’s systemic importance in global energy and manufacturing supply chains, the Government has succumbed to an optically popular but regressive short-term policy option that will potentially exacerbate the problem rather than help to solve it.

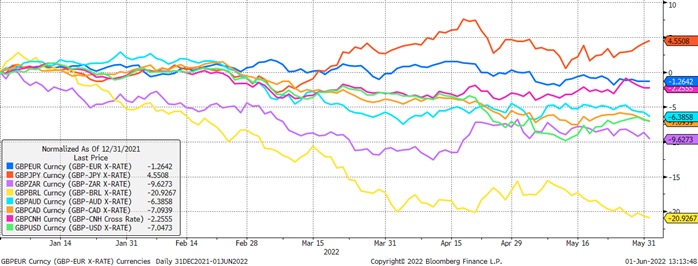

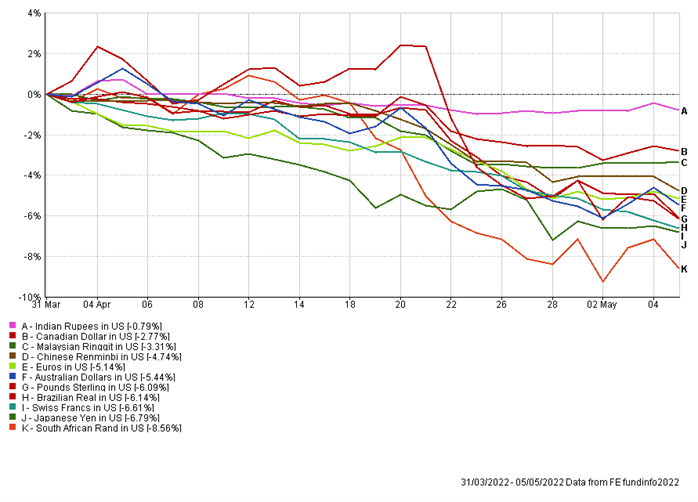

As mentioned in previous notes, investors’ perceptions of the UK economy have played out in the currency and bond markets this year, with the pound notably weaker this year versus almost all major currencies as the third chart below shows. Only the Japanese Yen (in dark orange) has fallen against the pound this year as the Government there persists with an extremely easy monetary policy stance. Elsewhere, weakness is pervasive, with falls of more than 7% against the US dollar (in green), and an extraordinary 21% fall against the Brazilian real (in yellow) which is benefitting from much higher commodities prices:

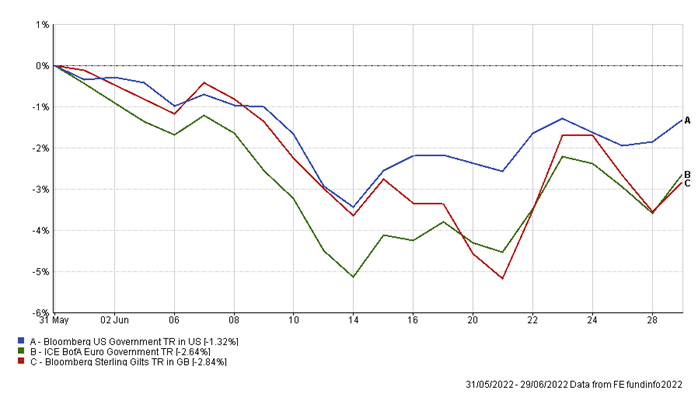

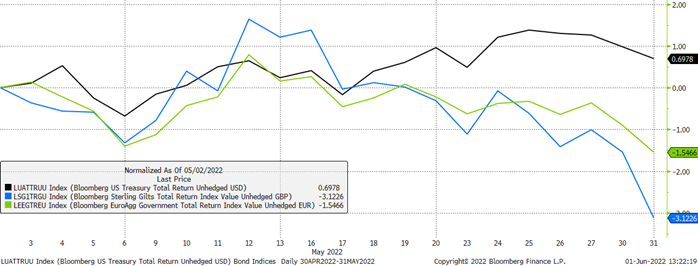

As the final chart below shows, UK government bonds have also begun to underperform global counterparts, with the Gilt index falling by 3.1% in May versus a fall of 1.5% for Eurozone government bonds and a rise of 0.7% for US treasuries. This is despite a hawkish Bank of England keen to carry on with rate hikes and shows weakening confidence in the UK economy:

As per last month, uncertainty will reign until a genuine improvement occurs in Europe. While commodities prices may not rise precipitously from here, they are unlikely to fall back to previous levels until a firm resolution has been agreed: something we sadly see few signs of at the time of writing. As always this speaks to the importance of diversification across portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Both equities and bonds were weaker in April as the conflict in eastern Europe, Chinese lockdowns and the prospect of tighter monetary policy weighed heavily on investor sentiment.

As the first chart below shows, only the large-cap, value-biased FTSE 100 index was positive for the month, rising modestly by 0.8%. Asian and Emerging Market indices were close behind, though negative, with the worst numbers seen in the US, with the S&P 500 falling by 4.3% in pound terms, and the tech-heavy Nasdaq by just over 9%:

In fact, returns for US equity holders would have been significantly worse had it not been for the strength of the US dollar over the same time period, as the currency benefitted from safe-haven flows, and anticipation of higher interest rates. As the second chart shows, the US dollar rose against all major currencies; substantially in many cases, including by 4.3% against the pound. This move meant that returns for UK investors were improved when translated back to pounds:

Fixed income markets fared little better, and in several cases suffered more than equities. Buffeted by high levels of inflation and hawkish central banks, bond yields rose, and prices fell across the board, from government to high yield bonds.

Expectations for the path of monetary policy have seen a major shift this year, with markets now pricing in interest rates of well over 2% in both the US and the UK by the end of 2022, while Eurozone rates are expected to move into positive territory later this year.

As the chart below shows, major global bond indices suffered falls of between 3-6% over the month, with the assumed relationship between bonds and equities breaking down spectacularly; government bonds were certainly not a safe haven asset in this instance:

Bonds have proved unusually weak throughout 2022 to date, with the chart below illustrating this for the US government bond market – arguably the most important bellwether available given the asset class’s importance as pristine, US dollar denominated collateral within the global banking system.

The chart shows percentage point, quarterly return bars for the US government bond price index going back nearly 50 years, with the final two highlighted red bars denoting returns for Q1 2022, and Q2 2022 to date. Q1 2022’s return was the worst in the index’s history, with the quarter-to-date return also proving negative thus far; a scenario that played out elsewhere within bond markets, if not quite to such an extreme extent:

Central bankers are stuck between a rock and hard place. On the one hand it is imperative that they be seen to be responding to levels of inflation not seen in 30 years. On the other they are aware that growth is already slowing for a multitude of reasons, not least among them a severe and growing cost of living crisis for consumers. They are increasingly aware that rapid and concerted interest rate hikes – which in isolation may well be needed to tame inflation – might tip economies into recession.

For now, labour markets remain robust and large amounts of pent-up savings mean that consumers’ balance sheets remain relatively robust, but downside risks appear to be growing. As per last month, uncertainty will reign until a genuine improvement occurs in Europe, and we see signs of restrictions being loosened in China. As always this speaks to the importance of diversification across portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Summary

News flow from Ukraine stabilised during the latter half of March, though the situation remains troubling. Fighting continues around the major cities with reports of extreme brutality emerging on a daily basis, and while negotiations between Ukraine and Russia are ongoing, little progress seems to have been made.

After a difficult start to the month, global equity markets made decent progress as the first chart below shows. US stocks led the way with the S&P 500 index rising by 5.7% in pound terms, helped by a strengthening dollar which rose by nearly 2% against the pound. Other developed market equity indices were further back though benefitting from a strong rally from the middle of March. Unsurprisingly, emerging market equities lagged given the ongoing geopolitical risk. Here, too, though, strong gains were made from the mid-point, coinciding with the aforementioned stabilisation:

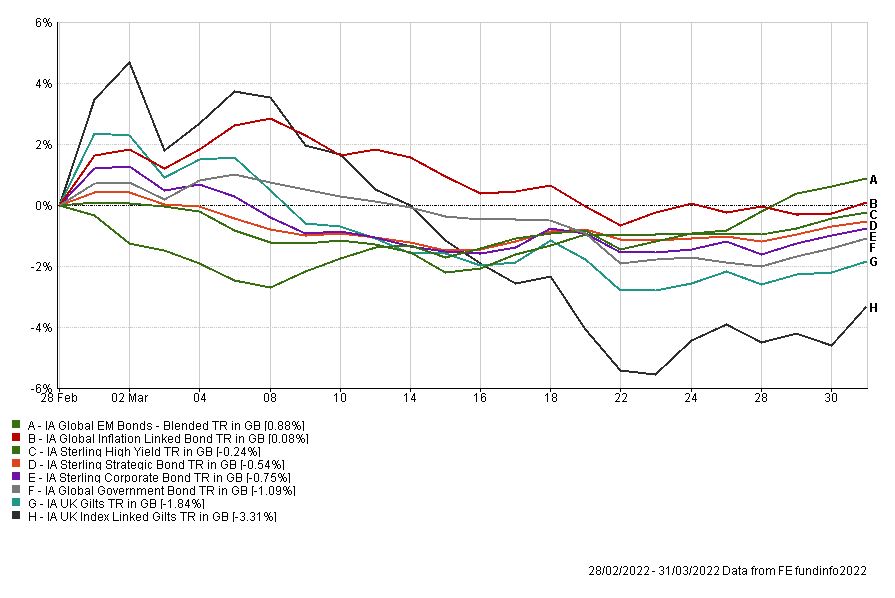

Bond market returns directly contrasted those seen in equities. Safe havens gained in the first 10 days of March before aggressively giving those gains up. Sharp drawdowns were seen particularly in government bonds as the chart below shows, with Gilts falling by just over 5% from peak to trough, and index-linked Gilts by nearly 10%. These losses were driven first by the lack of escalation in Eastern Europe, and then exacerbated as investors turned their attention back towards rapidly pivoting central banks which find themselves increasingly behind the curve on the inflation front:

The US Federal Reserve in particular has only become more hawkish in its latest public remarks. CPI sits at the highest level since the 1980s at 7.9% while the labour market remains strong. The unemployment rate fell to 3.6% in March – the lowest since February 2020 – and the participation rate rose to 62.4%. After beginning their rate hiking cycle with a 0.25% move, commentators now expect a more aggressive pathway involving consecutive 0.5% rate rises in May and June before ending the year above 2%.

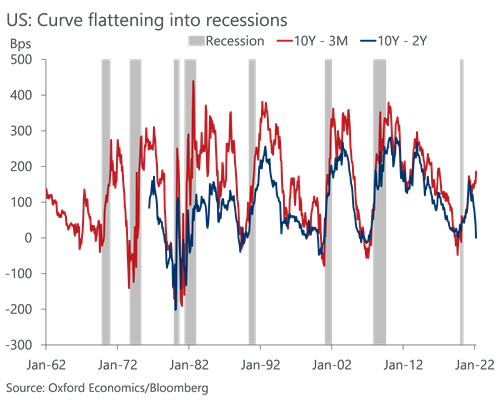

As this information is priced into markets and expectations, indicators of recession risk have been rising, with participants showing concern around the speed of rate rises and their potential impact on growth. The chart below for example shows two measures of US government bond yield curve steepness that have traditionally been useful for forecasting recessions. When these approach and pass through the zero bound to the downside, they indicate dampened growth and inflation expectations on a forward-looking basis as a result of heightened shorter-term interest rates.

Though useful, their lead times from inversion to recession have been highly variable, ranging from around nine months to nearly three years, but despite this it has been foolish to ignore the importance of their warning on almost every occasion going back many decades:

The situation is more difficult in Europe where the same inflationary pressures are apparent, but within an environment much more exposed to negative externalities stemming from the Russia/Ukraine crisis. These have already resulted in heavily dampened growth outlooks and worsening consumer sentiment, meaning that any hawkish central bank behaviour will be coming even as conditions are worsening – a poor combination:

For now, forecasts are generally to the downside, particularly looking to next year, but commentators in this space are at pains to point out that all have very large margins of error to the up and downside given uncertainties.

Similar to last month, looking at financial markets, uncertainty will reign until a genuine improvement occurs in Europe. High levels of volatility are likely to persist with a swathe of commodity prices likely to remain elevated. In this environment we would continue to favour ‘real’ assets linked in some way to inflation or inflation expectations – in this case particularly commodities. As always this speaks to the importance of diversification across portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Match me to an adviserSummary

February was dominated by news of Vladimir Putin’s deranged invasion of Ukraine. As we previously wrote, Russian forces attacked cities across the country overnight on 24th February, with little let up in fighting since. Other macroeconomic events naturally paled.

For the month as a whole, most equity regions fell in pound terms, with the FTSE 100 performing best, eking out a small positive return. Other regions were arranged behind, generating varying levels of negative returns, with European equities understandably worst hit with a 3.9% drop.

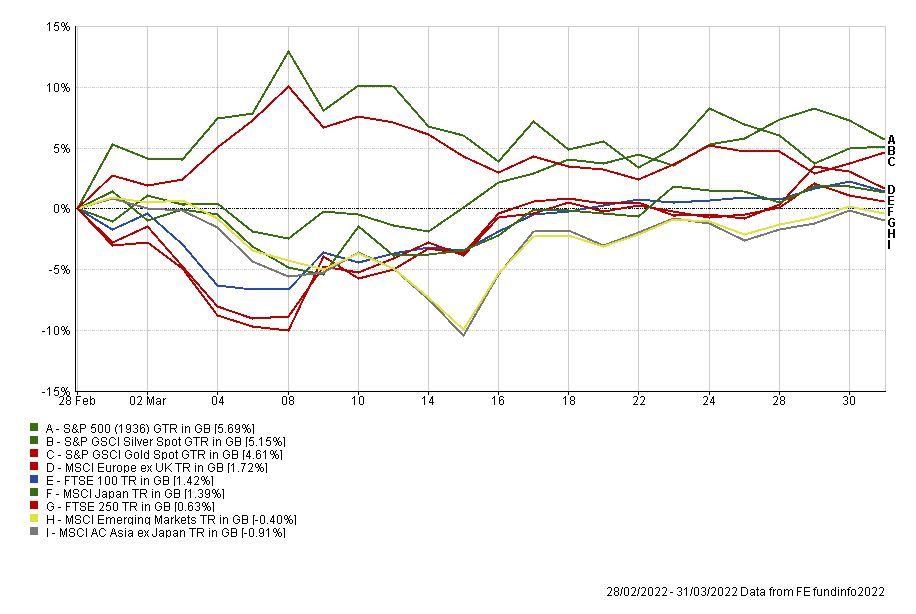

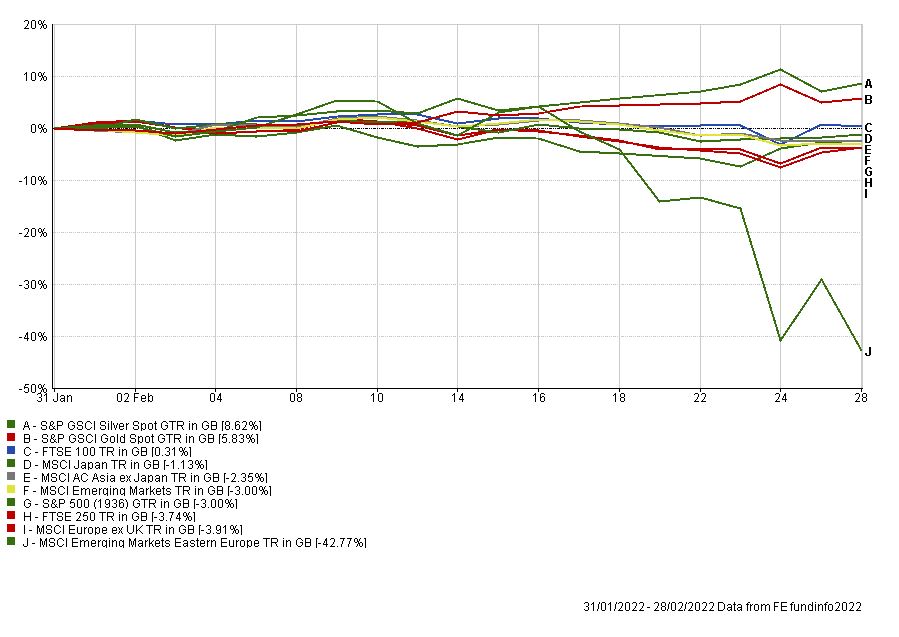

Safe havens performed well, with developed market government bonds retracing some of their year-to-date losses, and precious metals in the form of gold and silver moving sharply higher as the chart below shows.

The chart below also shows the stunning collapse in Russian equities through February as illustrated by the MSCI EM Eastern Europe Index that Russia dominates (c.61%). Almost all of those losses came in the last three weeks as the Moscow Exchange has shuttered with no immediate plans to reopen.

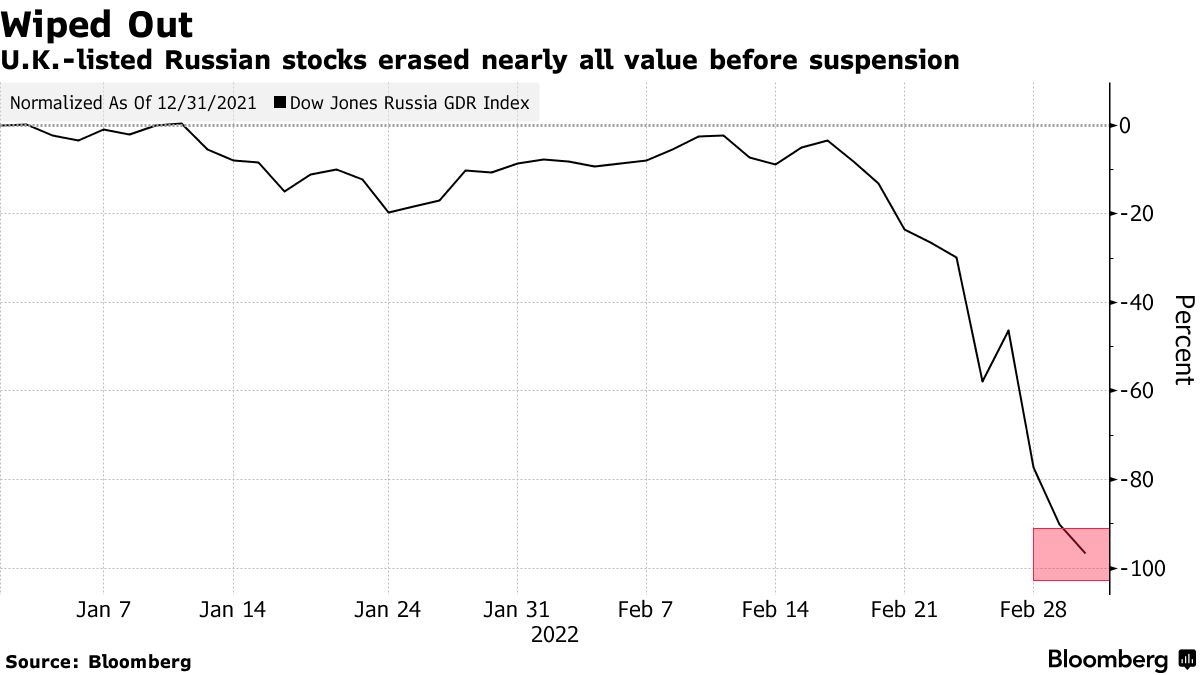

Russian stocks listed in London erased more than 90% of their value before being suspended as the second chart below shows, while global index providers announced plans to remove the nation’s shares from their indices and European companies with business exposure to the country lost more than $100bn in market value:

The Russian ruble has fallen by 23% in the last week alone versus the US dollar, while Russian government and corporate bonds have also collapsed, with ripple effects felt across financial markets.

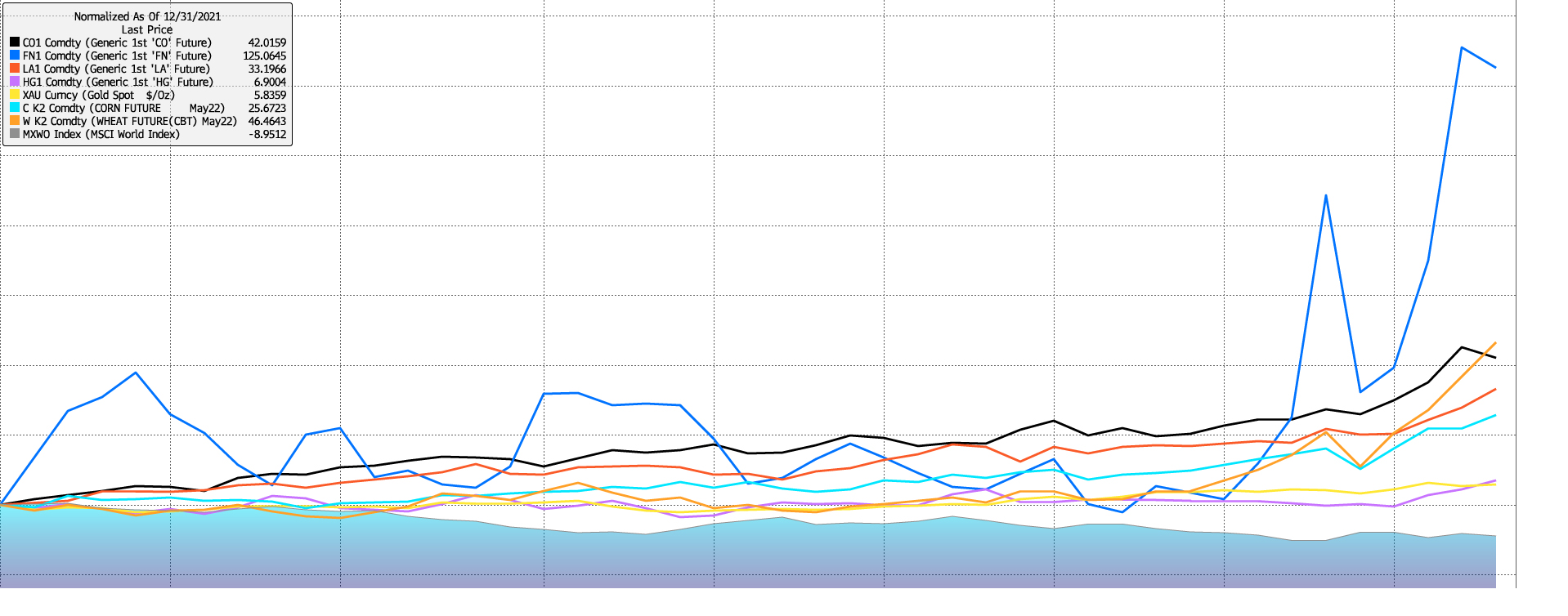

The most notable impacts have been seen in the commodities complex with the price of oil reaching levels not seen in 10 years and natural gas prices scaling previous unfathomable heights (oil denoted by ‘CO1’ and gas by ‘FN1’ in the chart below). Prices of agricultural and industrial commodities have also risen sharply, with those of corn and wheat 25.6% and 46.6% higher respectively, and those of aluminium (‘LA1’) and copper (‘HG1’) 33.2% and 6.9% higher respectively; all since the start of the year.

To highlight the magnitude of these gains, the MSCI World equity index is also included in this chart (shaded blue), with this gauge having fallen by nearly 9% over the same time period in US dollar terms:

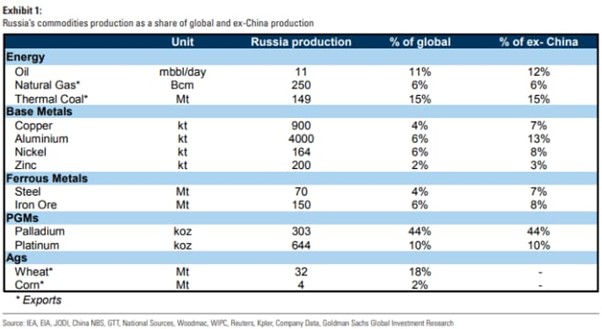

Russia, along with Ukraine, is a major producer of many crucial commodities as the table below shows, with these recent price rises commensurate with the potential disruption and uncertainty that may now follow should a resolution not be quickly achieved:

As we also wrote last month, sanctions were immediately imposed by the US, EU and UK, amongst other nations; initially on individuals and some banks, but now encompassing a wide spectrum of entities including the Russian central bank, whose foreign exchange assets have been frozen to the tune of hundreds of billions of dollars, impeding efforts to fund the war and keep the ruble under control. In addition, many western businesses have taken dramatic steps to cut off all ties with Russia across a vast swathe of sectors, from media and entertainment, to consumer goods and heavy industry.

While sanctions imposed in previous years seemed to be shaken off without much fuss, the speed and severity of what has been enacted here, along with their decisiveness and unity of implementation has caught many commentators wholly by surprise, not least the notion that western countries are prepared to sacrifice some comforts to try to stop Putin.

While Russian oil and gas imports have not been officially banned yet (though at the time of writing we note that this is now being actively discussed by the US government), we have observed that Russian crude oil is being shunned by market participants engaged in what is being termed ‘self-sanctioning’. Because of confusion around what is legally permitted, fears of reputational damage or moral objections, banks are disinclined to provide trade financing and tanker companies are reluctant to ship Russian oil, with the squeeze starting to have the same effect as an embargo. While undoubtedly bad for Russia, given their importance in global oil production, this could leave a big hole in the market.

Russian gas exports may be harder to ban or replace, unofficially or not. Infrastructure requirements are much more complex and difficult to replicate in the short term, with Europe relying on Gazprom for roughly one third of all gas it consumes.

Looking ahead, frustratingly there is little of certainty that can be said about this incredibly sad situation. Talks of some description are ongoing between the two sides though without any announcements of note, and for now we must hope for better headlines in the days to come.

Looking at financial markets, uncertainty will reign until said better headlines appear, with high levels of volatility likely to persist and further sharp moves in global commodities markets to be expected. In this environment, safe havens are more likely to outperform, along with ‘real’ assets linked in some way to inflation or inflation expectations – in this case particularly commodities. As always this speaks to the importance of diversification across portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

Sign up to our Intelligent Wealth newsletter to receive the latest industry news, articles and updates directly in your inbox.

Sign up to Intelligent Wealth

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Match me to an adviserRussian forces attacked cities across Ukraine overnight (23rd/24th February) after President Vladimir Putin ordered a ‘special military operation’ to support separatists in the Donbas region of Ukraine. Moscow confirmed that it is targeting military facilities in an attempt to demilitarise Ukraine, with reports of conflict in the capital, Kyiv.

The situation is extremely fluid, but President Putin has claimed he does not plan to occupy the country, and that energy supplies to Europe via Ukraine will not be disrupted.

Unsurprisingly the latest moves have been met with widespread condemnation from international leaders, with US President Biden announcing his intent to impose ‘severe sanctions’ on Russia and vowing a united and decisive response from Ukraine’s allies.

At the time of writing, global stock markets and government bond yields have moved lower, the price of Brent crude oil has passed $100 per barrel for the first time since 2014, while gold and silver prices have sharply increased. Outside of Russia itself, European equities have been hardest hit, with indices down up to 5% on the day, with the UK and US outperforming in relative terms thus far, falling by 2.5-3%.

We would expect volatility to persist until the situation becomes clearer. Additional sanctions will undoubtedly be announced by the US, Europe and UK in the coming days, most likely related to the movement of capital and goods. This in turn raises the probability that Russia will seek to respond in kind, with its main weapon being the supply of oil and gas to Europe.

As has been well-reported, Russia has already been restricting the flow of natural gas into Europe, and the aim of any further restrictions here would be to cause enough economic pain that Western leaders are forced to accept that Ukraine becomes a Russian client state within Moscow’s exclusive sphere of influence.

For now, we continue to watch the situation closely and will report on any further developments. Over a rolling 12-month period, developed market equities are still broadly in positive territory per the chart below, with emerging market and Asian equity indices providing strong relative returns in recent months, despite being negative over the past year in aggregate:

Within portfolios we are not planning any immediate changes, and we remain focused on finding long-term valuation opportunities across asset classes. Should a peace deal be struck in the coming weeks, a good buying opportunity will be presented to investors, although downside risks to that view remain. As always, diversification is of paramount importance, with real assets in the energy and commodities space performing particularly well at the moment.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Match me to an adviserAfter a strong end to 2021, both equities and bonds had a tough start to 2022, with negative returns driven by a confluence of higher energy prices, inflation worries and hawkish central bank rhetoric.

As the first chart below shows, global equity markets generally fared poorly despite a brief respite towards the end of the month, with US, European and Japanese indices falling particularly hard in Pound terms amidst very high intraday volatility. Emerging markets were a relative regional bright spot, falling by 1.2%, but the standout performer was large-cap UK equities, with the FTSE 100 rising by 1.1%:

Albeit over a very short time horizon, this outperformance was welcome following a miserable period for UK equities which have been desperately unloved for some time, despite earnings growth being solid. Valuations attributed to large and mid-cap UK equities are now below long-term averages, with both the FTSE 100 and 250 indices looking cheap in absolute and relative terms.

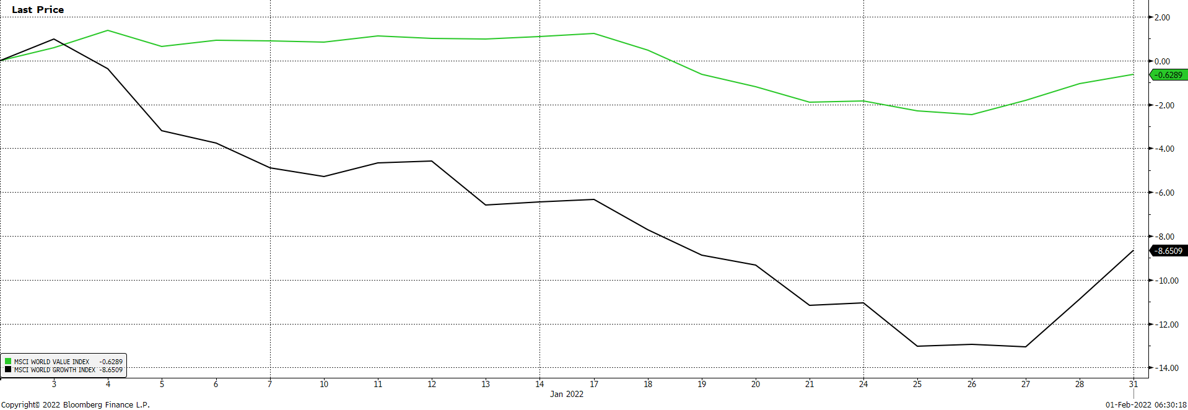

While headline equity index moves were volatile, beneath the surface we saw extremely aggressive rotations at the sector level, with investors choosing to sell more richly valued companies in areas like technology in favour of optically cheaper financial and energy stocks. The chart below captures this phenomenon, showing the relative performance of the MSCI World Growth and Value indices over the month, with the latter outperforming the former substantially:

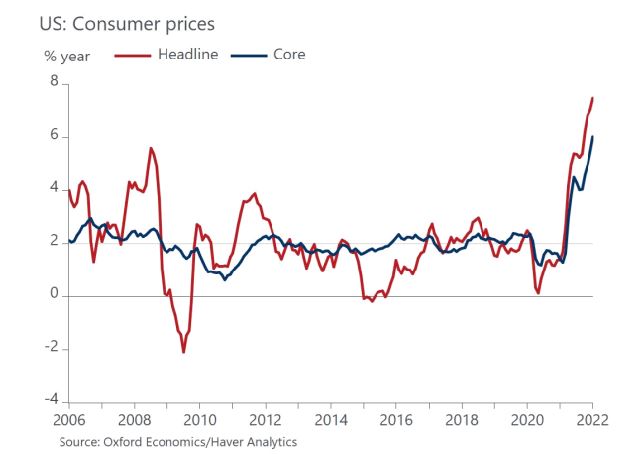

These gyrations were in part driven by a growing conviction that global central banks are set to concertedly raise interest rates materially from the zero bound in response to growing worries around inflation. CPI gauges have continued to precipitously rise across the developed world in particular, as excess demand driven by pandemic response fiscal and monetary stimulus meets constrained supply chains and poorly managed energy policies.

US inflation has now hit 7.5% year-on-year – the fastest rate of increase in nearly 40 years, and while prices are still forecasted to fall later this year, they are expected to remain above 2% targets for some time. Similar is occurring in the UK, where the Bank of England has already moved to raise interest rates, and in Europe, where inflation surprised strongly to the upside in January:

This has led to falling government and corporate bond prices as higher borrowing costs are priced in and investors reduce their positioning across the board. As illustrated below, sharp losses were felt across fixed income asset classes, leaving few safe havens for investors in which to seek shelter:

High volatility across asset classes has continued into February, as commentators become increasingly vocal about central bank largesse having a damaging impact on prices. The risk of a central bank policy mistake appears to be rising, with markets pricing in an increasingly aggressive rate hiking cycle most notably in the US. While a sensible policy normalisation should be welcomed, it seems unclear whether aggressive rate rises will help unblock global supply chains or reduce the price of natural gas, except through explicit demand destruction, which is undesirable.

While elevated risk in equity and bond markets may persist, it is important to note that macroeconomic data remains solid, though less positive than 2021. GDP should rebound in this quarter from an Omicron-impacted Q4 2021, while consumer and business balance sheets look robust. As always, we see intelligent portfolio diversification as the route through this period of relative uncertainty; gaining exposure to a number of differentiated risk and return drivers is of paramount importance.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Match me to an adviser