For some people the right time is determined by reaching a certain age, while others work towards reaching a certain amount of pension and savings as the trigger to move into the ‘golden years’.

But whatever the prompt, planning your finances to be sustainable for the long term is key.

Certainly the turbulent times we’re living through have given many people pause for thought to consider their work life balance and think more seriously about what their future holds. Here Fairstone Independent financial adviser Jennifer Fraser looks at six considerations for anyone looking to retire.

Inflation is a major factor when planning for retirement as it can reduce the purchasing power of your money over time.

Not only does inflation affect the eventual value of your pension while you’re making contributions, it can also affect how long the pot you’ve built up will last when you stop contributing and start drawing an income.

If the amount you receive in retirement is based on a fixed income, it will not be able to keep up with future inflationary rises, meaning that you may likely be unable to afford the same lifestyle that you enjoyed before retirement.

Therefore, it is essential to plan for retirement by ensuring that your savings and investments are able to grow in real terms, above the rate of inflation. This can be done through a combination of investing in assets that aim to provide returns above the rate of inflation, as well as ensuring that your retirement income is not linked to a fixed amount but instead grows with inflation over time.

Life planning is key to a successful retirement and when planning for your golden years, it’s best to get a strategy in place well in advance of your intended retirement date. This will provide you with sufficient time to get a full understanding of your financial situation as well as to recognise any potential issues or opportunities for improvement.

You should consider everything from age, income level and lifestyle when considering your retirement timeline as they will all have an impact.

People who have given serious time and thought to what they will do after they retire will generally experience a smoother transition than those who haven’t. Dreams and goals that cannot be achieved with a single trip or project may translate into long-term, part-time employment or volunteer work. But it is never too soon to begin mapping out the course of the rest of your life.

Ideally, you should start saving for retirement in your 20s and 30s, even though your retirement will seem years away. By doing this, it will give you the added time to build your savings and ensure that you have enough money to comfortably fund your retirement.

And of course, if you find yourself nearing retirement without a plan in place, you can seek professional financial advice to help you optimise your retirement plans.

Retirement cash flow modelling is very useful in making assessments about your future requirements. It enables you to consider all of your potential sources of income in retirement and how they can best be used to meet your expenditure needs.

Cashflow modelling can show you what is possible, what isn’t possible and what you can do instead to get you to where you want to be. It provides a graphic representation of your personalised roadmap, highlighting your goals and objectives along the way.

This means considering a number of factors such as your underlying investments, tax and, most importantly, how well your different income streams are protected against inflation. Another benefit of using cash flow modelling is that you can easily change those assumptions if your circumstances change, factoring in different investment returns, tax rates and inflation. This allows you to assess how much you need to have accumulated prior to your retirement.

Retirement is an important milestone in life, and it’s essential to make sure you have enough money to ensure a comfortable lifestyle afterwards. One option is to consider an annuity.

With fewer employers now offering the guarantee of a final salary pension, annuities could be an appropriate option to consider. An annuity provides a regular income for the rest of your life, and can make sure you have enough money to last you throughout retirement. One drawback to them though is that they typically do not provide lump sum death benefits and in most cases, your annuity dies with you.

But in order to decide whether an annuity is right for you, it’s important to look at the different types of annuities available, consider the tax implications and other factors such as inflation. To offer protection from future inflation, it could be worth considering an inflation-linked annuity, where annuity payments increase each year in line with rising costs. Other factors that can influence the returns from an annuity are your health and smoker status. If you are in poor health or are a smoker, the rates offered tend to be higher.

Even during periods of high inflation, investments that are in real assets can provide a hedge against the erosion of wealth. Whilst it is important to maintain a suitable emergency fund in cash to cover unexpected bills and other eventualities, high levels of cash holdings are ill-advised in this situation as the current interest rates barely meet inflation and its real value is guaranteed to decrease. Investing in assets is one of the best ways to safeguard your retirement savings against the effects of inflation.

Inflation can erode the value of your savings over time. By investing in real assets, you can help to ensure that your retirement savings remain secure even in a rising inflation environment. Investing in assets can provide you with the opportunity to create a sustainable and secure retirement plan that is protected from the effects of inflation. Ultimately, investing in real assets is an important part of any comprehensive retirement savings strategy.

When making investment decisions, you need to determine the level of risk that you are comfortable with. This will vary from person to person, so it is important to obtain professional advice to help you assess your risk tolerance. Understanding your attitude to investment risk is an important factor when planning for retirement and taking the time to learn about how you respond to different kinds of market volatility and levels of risk will help you create a more informative and effective retirement plan.

Knowing what kind of investor you are – conservative, balanced or aggressive – will enable you to make informed decisions about where to invest your money and how much risk you are comfortable taking on. It can also help you avoid some of the common pitfalls associated with retirement planning, such as being too conservative or overly aggressive in your approach. This will help you to save and invest more effectively, allowing you to make the most of your retirement savings.

There is no right or wrong attitude to risk. Risk is personal to you and is based on your circumstances, your goals and ultimately whether the thought of investing makes you feel nervous or completely calm or somewhere in between – and also how you react to market ups and downs.

Once you’ve worked out your approach, you can start building a pot that reflects how you feel about investment risk. Your feelings may change over time – but you can adapt your position as necessary.

Planning for retirement is a complex business and there are many different options available. Taking expert financial advice can help you sift through the many rules and product options available and help construct a portfolio to maximise your prospects and help you make sense of your future, whatever that may look like.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

A PENSION IS A LONG-TERM INVESTMENT NOT NORMALLY ACCESSIBLE UNTIL AGE 55 (57 FROM APRIL 2028 UNLESS PLAN HAS A PROTECTED PENSION AGE).

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

YOUR PENSION INCOME COULD ALSO BE AFFECTED BY THE INTEREST RATES AT THE TIME YOU TAKE YOUR BENEFITS.

That’s why it’s important to have an understanding of how inflation could be impacting your retirement plans and how best to respond. With the right strategies in place, you can still make progress towards achieving your goals and remaining financially secure during retirement.

The first thing to know is that inflation won’t necessarily derail your retirement plans. The important thing is to recognise the impact it has on long-term savings and investments and take proactive steps to keep your goals in sight.

One option is to review your investment portfolio and consider assets that have the potential to outperform inflation. It may also be worth assessing and identifying further opportunities for growth and investment diversification.

Although inflation may have an impact on short-term finances, its effects are typically less dramatic over the long term. Regularly reviewing your financial objectives and taking steps such as increasing contributions to a pension plan or Individual Savings Account (ISA) can help ensure your retirement plans remain on track.

When it comes to managing cashflow, paying off debt should take priority over building up savings if you want to keep pace with inflation. Reducing interest payments can free up more money each month which can then be put into a retirement fund or other investments.

If you find yourself falling behind on your retirement savings, it is important to take action now to get back on track. A useful first step could be to review your budget and identify any areas where you can reduce discretionary spending in order to maintain or even increase how much you are regularly contributing towards your pension.

This increased contribution will benefit from tax relief at your marginal rate of Income Tax up until age 75, making it an especially valuable move. However, make sure you only contribute what you can really afford, as pension money is locked away until age 55 (rising to age 57 from April 2028).

It is worth remembering that the amount you contribute should reflect what you can realistically afford in order to avoid taking on more financial commitments than you can manage over the long term.

Phasing into retirement is an option to consider. It would mean you can still maintain relationships and stay engaged with the professional world. Also, by working part-time or flexibly, you might be able to keep your pension fully invested and draw on other savings and investments to top up your lower income and still be able to retain benefits such as healthcare. This could help to provide additional financial security in your later years.

Additionally, a phased retirement gives you time to explore new opportunities and interests outside of work, while still earning money. It can also be a way to transition out of the professional world slowly and give yourself time to adjust to life after work. Whatever your motivations for a phased retirement, make sure it’s right for you and that you fully understand the implications for your finances. Do your research and consider all scenarios before making any decisions about when you will retire.

Remember that no matter what your decision is, it’s important to review all aspects of your finances. This will help ensure that you have the best chance at achieving a comfortable retirement lifestyle. With the right planning, phasing or delaying retirement could be a choice that helps you to have the retirement that you want.

Before deciding whether to take a tax-free lump sum from your pension, professional advice should always be sought so you fully understand the implications of withdrawing large sums in one go. You will need to consider not only the immediate financial benefit, but also how it might affect your future retirement income.

This means looking at your options, discussing potential risks, suggesting appropriate strategies and explaining possible tax consequences so that you can make an informed decision about your pension. Ultimately, receiving professional advice will help you decide whether taking a lump sum from your pension is the best decision for you and your long-term financial security.

Individual Savings Accounts (ISAs) are another tax-efficient way to supplement your income in retirement. Unlike pensions, the proceeds you withdraw from an ISA are completely tax-free. So if you have any savings that you can put aside relatively safely and access when necessary, this could be an ideal solution for managing your finances during retirement.

It may also be appropriate for you to consider investing in stocks or bonds, as these could provide even greater returns over time with some risk attached. However, it’s important to remember that stock market investments carry a certain amount of risk and can go down as well as up, so professional advice should always be taken before investing large sums of money.

When planning your retirement income, make sure you factor in other sources such as inheritance or rental income. This will help to ensure that you have enough money to enjoy your later years in comfort and security. Additionally, annuities may also be a way to turn your pension pot into a regular income stream. An annuity is an insurance policy taken out with an insurer that pays out a fixed sum each year until the policy matures or you pass away.

Overall, you should consider all of your options when planning for retirement. Using professional advice and understanding the different types of investments available can help you make informed decisions and maximise your income during the golden years of life.

To discuss the measures necessary to protect your long-term savings and investments from inflation to achieve your retirement goals, please contact us for more information.

| Match me to an adviser | Subscribe to receive updates |

A PENSION IS A LONG-TERM INVESTMENT NOT NORMALLY ACCESSIBLE UNTIL AGE 55 (57 FROM APRIL 2028 UNLESS PLAN HAS A PROTECTED PENSION AGE).

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

YOUR PENSION INCOME COULD ALSO BE AFFECTED BY THE INTEREST RATES AT THE TIME YOU TAKE YOUR BENEFITS.

Personal tax planning should be at the top of your agenda as the end of the current tax year is not too far away. Taking action now may give you the opportunity to take advantage of any remaining reliefs, allowances and exemptions.

At the same time, you should be considering whether there are any planning opportunities that you need to consider either for this tax year or for your long-term future. We’ve listed a few reminders of the issues you may want to consider as worthy of including in your 2022/23 tax health check to- do list.

Married couples should consider utilising each person’s personal reliefs, as well as their starting and basic rate tax bands. Could you make gifts of income-producing assets (which must be outright and unconditional) to distribute income more evenly between you both?

This is an especially tax-efficient way for you to make pension contributions, to save and reduce your Income Tax and National Insurance. Have you considered exchanging part of your salary for payments into an approved share scheme or additional pension contributions?

Unless you are an additional rate taxpayer or have already accessed pension benefits then you are entitled to make up to £40,000 of pension contributions per tax year. Have you fully utilised your tax-efficient contributions for this tax year or any unused allowances from the three previous tax years?

A stakeholder pension is available to any United Kingdom resident under the age of 75. Children can also make annual net contributions of £2,880 per year, making the gross amount £3,600 regardless of any earnings. It is also a very beneficial way of giving children or grandchildren a helping hand for the future. Is this an option you or a family member should be utilising?

The Lifetime Allowance (LTA) is currently £1,073,100 and has been frozen at this level until the 2025/26 tax year. The maximum you can pay in is £40,000 per annum unless you pay tax at 45% in which case the annual limit could be as low as £4,000. Inflationary increases by the end of the current tax year could also have an impact on your pension funds. Do you have a plan in place to protect your money from this?

If you’re are 55 or over you could access 25% tax-free cash from your Defined Contribution (also known as Money Purchase) pension pots and invest the rest. However, drawing large amounts in one tax year can lead to a larger tax bill than if spread over a longer period. Do you know the implications of taking money out of your pension pots?

Usually called a ‘spousal by-pass trust’, although the recipient may not always be a spouse, this is a discretionary trust set up by the pension scheme member or pension holder to receive pension death benefits. Are your pension death benefits written in trust?

An ISA allows you to save and invest tax-efficiently into a cash savings or investment account. The proceeds are shielded from Income Tax, tax on dividends and Capital Gains Tax. The government puts a cap on how much you can put into your ISA or ISAs in any tax year (from 6 April to 5 April). The ISA allowance for 2022/23 is set at £20,000. Have you fully utilised the maximum annual allowance?

This is a long-term tax-efficient savings account set up by a parent or guardian, specifically for the child’s future. Only the child can access the money, and only once they turn 18. Have you invested the maximum £9,000 allowance for your child or children?

The Lifetime ISA (LISA) is a tax-efficient savings or investments account designed to help those aged 18 to 39 at the time of opening to buy their first home or save for retirement. The government will provide a 25% bonus on the money invested, up to a maximum of £1,000 per year. You can save up to £4,000 a year, and can continue to pay into it until you reach age 50. Could you be taking advantage of this very tax-efficient option?

There are two different rates of CGT – one for property and one for other assets. If your assets are owned jointly with another person, you could use both of your allowances, which can effectively double the amount you can make before CGT is payable. If you are married or in a registered civil partnership, you are free to transfer assets to each other without any CGT being charged. It is currently £12,300 but will be reduced to £6,000 from 6 April 2023 and £3,000 from 6 April 2024. Have you fully used your current £12,300 annual exemption?

IHT must be paid on the value of any estate above £325,000, or up to £1 million for married couples including the residence nil-rate band). However, certain business assets, including some types of shares and farmland, in private trading companies can qualify for 100% relief from IHT. The government has frozen the IHT thresholds for two more years to April 2028. Are you taking advantage of the reliefs available to you?

This allowance was introduced during the 2017/18 tax year and is available when a main residence is passed on death to a direct descendant. The allowance is currently £175,000. When combined with the nil-rate band of £325,000, this provides a total IHT exemption of £500,000 per person, or £1 million per married couple. If you are planning to give away your home to your children or grandchildren (including adopted, foster and stepchildren) the RNRB must be claimed. There is a form for this purpose – IHT435. The form is available on the Gov.uk website. If applicable, have you applied for the RNRB?

If you leave at least 10% of your net estate to charity a reduced inheritance rate of 36% applies rather than the usual 40%. Other exemptions apply for inter- spousal transfers, transfers of unused annual income, business and agricultural assets, and for various other fixed, small amounts. Are you intending to make gifts before the end of the current tax year?

These help protect your assets and guarantee that your loved ones have financial stability for their future. Crucially, a trust can help to avoid IHT and ensure that the majority of your money, shares and equity are passed on in the most efficient way. Should you consider setting up a trust?

Future legislation could potentially result in changes to tax law, which could in turn require adjustments to your plans.

We hope you find this checklist useful, but please bear in mind that this only provides a summary of the options available and not all options will be suitable for everyone. Therefore, for more information in respect of the ideas outlined, please contact us.

| Match me to an adviser | Subscribe to receive updates |

A PENSION IS A LONG-TERM INVESTMENT NOT NORMALLY ACCESSIBLE UNTIL AGE 55 (57 FROM APRIL 2028 UNLESS PLAN HAS A PROTECTED PENSION AGE).

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

YOUR PENSION INCOME COULD ALSO BE AFFECTED BY THE INTEREST RATES AT THE TIME YOU TAKE YOUR BENEFITS.

THE VALUE OF YOUR INVESTMENTS CAN GO DOWN AS WELL AS UP AND YOU MAY GET BACK LESS THAN YOU INVESTED.

THE FINANCIAL CONDUCT AUTHORITY DOES NOT REGULATE TAXATION AND TRUST ADVICE. TRUSTS ARE A HIGHLY COMPLEX AREA OF FINANCIAL PLANNING.

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FAIRSTONE ARE NOT TAX ADVISERS. FOR GUIDANCE ABOUT HOW CAPITAL GAINS TAX EFFECTS INDIVIDUAL CIRCUMSTANCES, SEEK SPECIALIST TAX ADVICE

If you’re currently receiving or have been looking into the State Pension, then you’ve probably heard of the ‘triple lock’. But what is it?

The triple lock was introduced in 2010. Its purpose is to make sure that the State Pension doesn’t lose value over time. The triple lock aims to protect pensioners against the impact of inflation. If the State Pension didn’t change but the price of goods and services continued to increase over time, then you wouldn’t be able to buy as much with it. Meaning you’d be losing money in real terms.

In the 2022 Autumn Statement, the Chancellor confirmed that the triple lock will be reinstated from 6 April 2023. This means the State Pension will rise in line with last September’s inflation rate – 10.1% – in the 2023/24 tax year. Anyone receiving the State Pension will benefit from the triple lock.

To make the guarantee even more secure, it included three separate measures of inflation, hence ‘triple lock’. The three-way guarantee was that each year, the State Pension would increase by the greatest of the following three measures: average earnings; prices, as measured by the Consumer Prices Index (CPI) and 2.5%. The government usually compares the three rates in September, be- fore implementing the correct rise the following April.

The State Pension triple lock has proved to be a burden for successive governments, as it has proven costly for the taxpayer. Because of people earning much less during the lockdowns of 2020, there was a big leap in average earnings of 8% come 2021 as people returned to work. The government announced that the triple lock would be suspended for the 2022/23 tax year.

It’s never too early to be planning ahead. We can help you create a robust and flexible retirement plan. A plan that will consider your future expenditure and the impact of inflation, as well as making the best use of tax allowances.

To find out more, please get in touch.

| Match me to an adviser | Subscribe to receive updates |

An extended government scheme which allows consumers to fill historic gaps in their National Insurance record, comes to an end in less than three months.

Under normal rules, people can fill in gaps in their National Insurance record for a period of six years and after that point, the year becomes a permanent gap and could affect the ability for someone to build up a full state pension by retirement age.

But for a limited time, the Government is allowing people to go back an extra 10 years to fill in any historic gaps in National Insurance – meaning this extends the potential backfill period back to 2006/7.

Consumers have until 5 April 2023 to benefit from this extension before the usual six year window comes back into force.

Paying voluntary NI contributions can be an effective way from some people to fill in gaps they may have in their NI record to help boost their state pension.

For example, someone with a 10 year gap in National Insurance contributions could pay out just over £800 to backfill but see a boost of £5,500 in state pension over a typical 20-year retirement.

Anyone thinking of topping up their state pension for these earlier years should seek advice first as there are some situations in which paying historic contributions would not boost a state pension.

You can check with the Future Pension Centre at the DWP and if you want to discuss your situation, plans or for further information, please contact us.

| Match me to an adviser | Subscribe to receive updates |

The majority of parents want to give their children the best start in life and what better way than financially investing in their future?

Christmas is traditionally a time for giving and it could be the perfect time to gift your children and grandchildren with something that they can appreciate for years to come.

There are a number of ways you can start investing for children and even small amounts can really add up over the long-term. It could also have the added advantage of helping you to benefit from tax incentives to reduce the amount of tax paid, both now and in the future.

So what are your options?

With recent market volatility, some people are naturally concerned about their returns on investing, but with up to an 18-year horizon, putting money to work in the market can give significantly higher returns.

And investing some money, either as a one-off lump sum or on a regular basis, can be an ideal way to give a child a head start in life.

There are a range of options available when it comes to the ownership of investments for a child. Children receive many of the same tax-efficient allowances as adults, so it’s worth looking at specialist child investment accounts.

Some people prefer to keep investments for children in their name so that they have the option to access them in the future should they need to. It’s worth noting that if you keep personal ownership of the investment, it will be your tax rates that apply, not the child’s. Also, if the investment remains in your estate on death, more taxes could be payable, so be aware of this.

One option to consider is a Junior Individual Savings Account (JISA). Introduced in the UK in November 2011, a JISA is as long-term savings account set up by a parent or guardian and lets you save on behalf of a child under 18, without paying tax on income or gains.

With a Junior Stocks and Shares ISA account, you can put your child’s savings into investments like funds, shares and bonds. Any profits you earn by trading investment funds, shares or bonds are free from tax.

Investments are riskier than cash. They could give your child a bigger profit but always remember that the value of a Junior Stocks and Shares ISA can go down as well as up.

The JISA limit for the tax year 2022/23 is £9,000 and the money in the account belongs to the child, but they can’t withdraw it until they turn 18, apart from in exceptional circumstances. They can start managing their account on their own from the age of 16.

When the child turns 18, their account is automatically rolled over into an adult ISA and they can choose to take the money out and spend as they like. Therefore, it’s also important to make sure that children are given financial education from a young age so that they use their funds wisely when they get their hands on them.

A trust is a legal arrangement in which assets can be settled by a parent or grandparent for example, for the benefit of someone else, such as a child.

Assets settled into a bare trust are held in the name of the trustee(s) and when the child is 18, they have the right to all the income and gains from the trust. These are taxed as if they belong to the child, often meaning little or no tax. There are however special rules in respect of income tax when the trust is established by a parent and therefore it is important to take financial advice first.

There are no limits to how much you can put into a bare trust and unlike a JISA, the money can be accessed at any time before the child is 18, as long as it is for their benefit.

Trusts can be complicated though, so it’s always worth seeking professional advice first.

A discretionary trust can be a flexible way of providing for several children, grandchildren or other family members.

For example, you might want to set up a trust to help pay for the educational costs of your grandchildren.

The trust can have a number of potential beneficiaries and the trustees can decide how the income is distributed.

However, it’s worth keeping in mind that the tax rules can become complex when using a discretionary trust.

If you’re six, your focus might be more on Barbie and Lego than whether you will have enough money to retire, but starting an early years pension can help set them on the right path to ultimately enjoy their golden years.

And it’s never too early to start as the sooner someone starts saving the more they will gain from the effects of compounding returns.

Children have an annual pension allowance of £3,600 with contributions benefiting from 20 per cent tax relief. So that means a parent or grandparent can invest up to £2,880 which would then be topped up by the Government by £720 and as with all pensions, returns are also tax-free.

However one thing to be mindful of is that the current minimum age at which personal pensions can be accessed is age 55 and this is set to rise to 57 by 2028 and so it’s a much longer term approach to investing.

Putting money aside for a child is not only a great way to prepare for their future, it can also teach valuable lessons about managing their finances – and arguably that’s the best financial gift you can give.

We develop our attitudes and beliefs about money in childhood. And by talking about money, budgeting and good money management habits, you can start the foundations to setting your children up for a future of financial success.

If you are unclear on how you can get started, we’re here to explain your options

| Match me to an adviser | Subscribe to receive updates |

Fairstone chartered financial planner Sandra Corkhill discusses the gender pension gap and steps you can take to help reduce it.

Being a volunteer for the PFS, I help to teach financial literacy in colleges and universities. Client case studies are used to teach good financial habits. Astute audience members will often ask, how much could I earn in my lifetime? Or why are we so old when we get a State Pension? At this point all debates get lively but it got me thinking…

We’ve all heard about the gender pay gap, but very few discuss the gender pensions gap, despite the fact so many women experience it. Women’s pensions at retirement are half the size of men’s, regardless of the sector they work in, new research has highlighted [1].

The gender pension gap is the percentage difference in income between men’s and women’s pensions and it begins at the very start of a woman’s career.

The research found that every single industry in the UK has a gender pensions gap, even those dominated by female workers. Considering women are likely to live four years [2] longer than men, this issue deepens as they need to have saved around 5% to 7% more at retirement age.

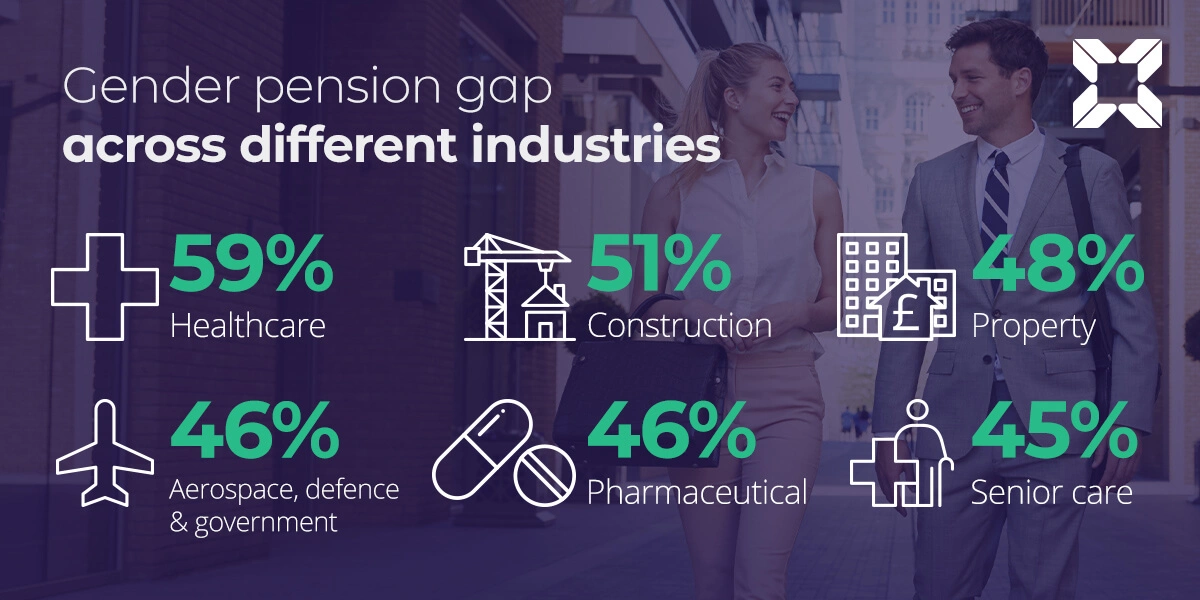

According to the research, the gender pensions gap exists regardless of average pay across different sectors, and ranges from a gap of 59% in the healthcare industry, to 13% in courier services. The healthcare (59%), construction (51%), real estate/property development (48%), pharmaceutical (46%), aerospace, defence and government services (46%), and senior care (45%) sectors were found to have the largest gender pensions gaps. Of these six sectors, three are key industries for female employment – healthcare, pharmaceuticals and senior care [3].

There are many reasons for the gender pensions gap, ranging from women holding fewer senior positions and being paid less, resulting in lower pensions contributions, to the fact they are more likely to take career breaks due to caring responsibilities. Of those that have taken a career break, 38% did not know the financial impact it had on their pension contributions [4].

Another potential driver is a significant gender confidence gap when it comes to managing pension pots. More than a quarter (28%) of women said they had confidence in their ability to make decisions about their pension, compared to almost half (48%) of men [5].

This lack of confidence extends further to other financial decisions, with women less likely than men to feel confident managing their investments (22% of women versus 41% of men), and their savings (56% of women versus 67% of men).

Women often have disrupted work patterns, career gaps and work part-time – this can impact their ability to save consistently for retirement without savings gaps. If you are concerned about your retirement plans and would like to review your pension options, please contact us.

| Match me to an adviser | Subscribe to receive updates |

Source data: [1] The analysis is based on LGIM’s proprietary data on c.4.5 million defined contribution members as at 1 April 2022 but does not take into account any other pension provision the customers may have elsewhere.

[3] According to the ratio of female members across the Legal & General book of business.

[4] Legal & General Insight Lab survey of 2,135 workplace members was conducted between 4–26 July 2022.

[5] Opinium survey of 2,001 UK adults was conducted between 4–8 February 2022.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless plan has a protected pension age).

Your pension income could also be affected by the interest rates at the time you take your benefits.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this article represent those of the author and do not constitute financial advice.

Over time, it is easy to lose touch with pension savings providers as we change jobs, move home and the companies we have worked for change ownership or close down. All these events over time may make it very difficult to find your valuable pension savings. So that means potentially ending up with a number of different pension pots. If you’re one of the millions of people with multiple pension pots, it may be appropriate to consider consolidating your defined contribution pension pots and bring them together.

Even if you have not had many jobs, you could still have a number of different pensions to keep track of. If appropriate, pension consolidation can simplify your finances and make it easier to keep track of your retirement savings.

Having said this, not all pension types can or should be transferred. It’s important to obtain professional advice so you know and can compare the features and benefits of the plan(s) you are thinking of transferring.

Pension consolidation is the process of combining multiple pension pots into one single pot. This can be done with a pension transfer or by opening a new pension and transferring your other pensions into it. You may want to do this to make it easier to keep track of your retirement savings, or to try and get a better rate of return on your investment.

But there are a few things to consider before consolidating your pensions, such as any exit fees that may be charged, and whether or not you will lose any valuable benefits such as guaranteed annuity rates.

If you think you might have lost a pension pot from a previous job, you can use the government’s Pension Tracing Service. This enables people to locate money previously saved for retirement, that is unclaimed. So, it is worth checking if you could have pension funds that have not been claimed.

Finally, you also need to bear in mind that pension savings are big targets for fraudsters. If someone contacts you unexpectedly offering to help you transfer your pot, it’s likely to be a scam. If you’re concerned, contact the Financial Conduct Authority (FCA) to check they’re legitimate.

You only have one retirement so you don’t want to make a costly mistake with your pensions that you could one day regret. Before you look to bring your pensions together, it’s essential to obtain professional advice. For more information about how we can assist you through this complex process, please contact us to discuss your situation.

| Match me to an adviser | Subscribe to receive updates |

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless plan has a protected pension age).

Your pension income could also be affected by the interest rates at the time you take your benefits.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this article represent those of the author and do not constitute financial advice.

And making the wrong decision could end up costing you dearly through either an unwanted tax bill or even worse, eventually running out of money in retirement!

Likewise, avoiding making decisions could cost you a lot as well.

Many people may be looking at up to 40 years of retirement and as we enter Pension Awareness Week (October 31), Fairstone Chartered financial planner Elizabeth Webb explains some of the steps you can take to help build your future income and fund the retirement you want.

Whatever your concept of a good pension pot, relying on the State Pension alone is unlikely to give you a good enough pension to live on comfortably through your retirement.

‘Will I be able to retire when I want to?’ ‘Will I run out of money?’ ‘How can I guarantee the kind of retirement I want?’ These are all hard questions to answer unless you start to review your finances early and make plans for your future.

Worryingly, it’s been well documented that many people aren’t saving enough in their pension for their retirement and probably the best bit of advice I can give is to just get started.

It’s never too early to start planning for your future. When planning for retirement, the truth is that the earlier you start saving and investing, the better off you’ll be, thanks to the power of your money compounding over time, which essentially means that your money earns interest on itself.

Think of it as a bit like a snowball: the further up the mountain it rolls down from, the more snow it picks up, and the bigger the snowball is by the time it reaches the bottom. Put simply, this is what happens to your money.

As many people’s budgets are being squeezed at the moment, it’s more important than ever to make sure your finances are in good shape. Whenever you can, try to think of the following strategy: for every pound you spend (on a daily basis) you also save one (for holidays or big expenses) and invest one (in a pension or long-term saving for example).

A bonus of using this technique is that it will make you think twice before spending anything and make sure you really value what you spend your money on.

It is impossible to precisely time market peaks and troughs, and market downturns can have an impact on the value of your retirement pot, which is directly dependent on the value of the investments your pension fund owns.

It’s important to remember that a pension is a long-term investment and while the fund value may fluctuate and can even go down, your eventual income will depend upon the size of the fund at retirement, future interest rates and tax legislation. Stay invested as history shows the important thing is time IN the market, not timING the market.

When budgets are tight, is it often tempting to dip into savings, pensions and investments. But while it may be attractive to do this in the short term, it is important to think about the long-term impact this could have on your retirement plans.

Drawing down on your pension or selling investments could leave you worse off in the long run, especially if the investments are volatile when you take money from them. So it’s important to consider all of your options, such as cash deposits, before making withdrawals from invested assets and even considering if there are other ways of reaching your goals.

A state pension forecast gives you an estimate of the amount of money you will receive from the Government once you reach retirement age.

You can obtain your forecast online through the Government’s website, visit: https://www.gov.uk/check-state-pension. When requesting your forecast, you will need to provide personal information, such as your date of birth and National Insurance number.

Once you have received your forecast, it is important to keep in mind that the amount stated is only an estimate. The actual amount you receive may be higher or lower than what is indicated on your forecast, depending on a number of factors.

If you plan to retire within the next five years or so, it’s worth taking advice to help bolster your retirement lifestyle as you approach your planned retirement date.

Cash flow modelling can help you to understand how much income you will need in retirement, work out how long your retirement savings will last, determine the best way to use your retirement savings to generate an income in retirement and find out how different life events (such as taking a career break or downsizing your home) could impact your retirement cash flow.

Some people may now need to think about the impact that inflation could have on their retirement income, and to consider whether they can afford to retire yet. Rising inflation can wipe years of retirement income off pension pots as savers must increase the amount they withdraw to maintain the same spending power each year.

To offset the impact of inflation, you may need to adjust your retirement plans. For example, you may need to save more money so that you can maintain your standard of living in retirement. Additionally, you may need to invest in assets that are less vulnerable to the effects of inflation.

It’s important to remember that retirement planning is not a one-time event. Your retirement timeline will likely change as life circumstances change.

For example, you may need to adjust your timeline if you have children or other family members who depend on you financially.

Remember, the most important step is to do something – don’t ignore your future plans, and ask for help from someone who can offer impartial, well-informed advice to help you make these plans more real and achievable.

For more information about how we can assist you, get in touch below.

| Match me to an adviser | Subscribe to receive updates |

The call from wealth management house Fairstone coincides with National Pension Tracing Day on October 30, which sheds the spotlight on the growing issue of lost pensions.

According to figures released today by the Pension Policy Institute (PPI), more than £26.6bn now sits in lost pension pots, an increase of 37% in recent years, with almost three million pots currently not matched to their owner. Meanwhile the Government predict that there could be around 50 million dormant and lost pensions by 2050.

“People should act now to track down their hard-earned money which could be sitting in missing pension pots.

“The prime causes for losing track of pensions are people changing jobs and or address but failing to notify their pension provider, meaning many people are in danger of missing out on significant sums of money.

“Research shows that while 89% of people who move home inform their GP or dentist, only one in 25 people would automatically think of letting their pension provider know, meaning many contact details are out of date.

“With each lost pot, people are losing track of their hard-earned money. An added problem is that these pots may be languishing in underperforming schemes, so it really is worthwhile taking a bit of time to try to track these down.

“This year’s National Pension Tracing Day coincides with the clocks going back, so it could be a very good way to take advantage of that extra hour.”

There are several steps you can take if you believe you may have a lost pension pot.

Peter explained that if a consumer is unsure of any previous pension provider, their first port of call should be the Pension Tracing Service. This is a free service which searches a database of more than 200,000 workplaces and personal pension schemes to try to find the contact details an individual may need.

He added: “If you do trace any missing pension pots, the next decision you will need to make is to either consolidate these or keep them as they are.

“This is really the time to take professional advice as while bringing together pension pots could provide a clearer picture of retirement assets, a pension consolidation is not always appropriate. For example, an individual may have a lost defined benefit plan and having a guaranteed income may suit the individual better. A defined contribution plan may also have valuable benefits such as a guaranteed annuity rate which could provide a high level of guaranteed income which would be lost if switched to another plan.

“A financial planner can listen to a consumer’s individual needs and objectives and then create a proposal using the pensions plans in the most appropriate and advantageous way.”

We have over 650 local advisers & staff specialising in investment advice all the way through to pensions. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |