How much do you value your time?

This is not a philosophical question, but a practical one.

I find it especially useful to think in these terms when I’m considering how and what to spend my time on.

It’s something all of us can do – and I’ll show you how.

First of all, think about how much you earn at work.

Some people are paid hourly, many people charge hourly rates for their work while others of us can work out our effective hourly rate by dividing a month’s salary by the number of hours worked.

Once you’ve got that figure, then consider how much you would charge or would want to be paid for working outside your normal hours – in the evenings, at weekends, or on Bank Holidays, for example.

I’d imagine that ‘out of hours’ work figure is quite a bit more than your normal hourly rate.

That’s why it’s important to spend that time wisely, whether that’s with your family, your friends, relaxing or enjoying hobbies.

If you spend your time wisely, I’d imagine you’d also want to spend your money wisely too – particularly when it comes to investing that money for your family.

When time and money are of the essence, is it a good idea to spend both at once?

I ask the question because that is what DIY investing essentially consists of.

Investing can be hugely rewarding, but it is also hugely complicated with significant consequences if you get things wrong.

As we always say whenever we talk about investing, the value of your investments can go down as well as up and you may not get back the full amount that you invested.

As a DIY investor, you can buy any publicly traded share, fund or bond anywhere in the world with no checks and balances and, thanks to technology, you can trade at the touch of a button anywhere you want.

If you manage to swerve the siren voices of social media influencers peddling questionable crypto and get rich quick schemes, how do you choose what to invest in?

You’re going to have to spend a lot of time researching investments – and if you use the ‘out of hours’ calculation, that process alone could cost you a lot of money.

For example, which country should you invest in?

If it isn’t the UK, how will you factor in exchange rate fluctuations? What effect will such investments have on the tax you pay, here and potentially in another country?

If you’ve chosen a country, which sector or sectors have the best growth prospects within that country and which individual companies are the best performers within those sectors?

Let’s say you decide not to invest in individual companies and countries but in an investment fund.

Which one of the 16,000+ funds should you choose?

Can you be sure that a fund that’s performed well previously will do so now?

Have the market conditions changed since that fund did well?

Do you know whether the people who were in charge of the fund when it was successful are still there now or have moved on somewhere else?

Add up the ‘out of hours’ time you need to put in to find the answers to these and myriad other investing questions and you can see you’re basically doing a second job to invest some of the money you make from your main full-time job.

With raising a family and making a home a job in itself, you’ve now got three full-time jobs to fit into your 24 hours a day.

And what happens if you’ve invested a lot of your family assets, future wealth and your precious time in something which turns out to be disastrous?

Did you really know the risks before you put your money into an investment and did those risks match up with how you feel about the potential of losing money?

Behavioural economics tells us that people feel losses twice as strongly as they do equivalent gains – do you want to feel personally responsible for losing money for your family and financial future after you have spent so much time trying to get it right?

There is no such thing as a foolproof investment but there are certain things which can help when it comes to investing:

Experience.

Expertise.

Knowledge.

Access to market and company intelligence and analysis.

Extensive support and guidance.

Constant research and updates.

This is what you get when you spend some of the money you have earned on bringing in an expert professional financial adviser like those at Fairstone.

While you deal on a one-to-one basis with your adviser so that he or she can really get to know you and understand your financial goals, in reality at Fairstone there is a whole team of people behind that adviser.

From researchers to paraplanners, portfolio managers to investment analysts, your adviser can call on a whole host of fully qualified experts to assist you.

In fact, what you have is essentially an “always on” adviser to help you negotiate not just the investment world but also assist in areas such as retirement planning, estate planning and financial protection, all while keeping an eye on important aspects of wealth building such as taxation.

And guess what?

All of this means you don’t have to get that ‘second job’ as a DIY investor – instead you can concentrate on the job which earns you money and the job of raising your family and making a home.

And as for that ‘out of hours’ time, you can spend it doing something you really love – rather than something you have to do.

That’s surely worth a lot, not just to you but also to your family and friends.

For expert professional help with your financial future, get in touch with one of our advisers.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

You may have noticed a familiar pattern in recent years.

A government unveils a controversial budget.

A prime minister resigns unexpectedly.

A new spending plan unsettles investors.

Within hours, financial headlines begin repeating the same phrase: “gilt yields are rising”.

But what does that actually mean, and why should you care?

To understand, it helps to start at the beginning.

A bond is, at its simplest, a loan.

When a government or company needs to raise money, it can borrow from investors by issuing bonds.

In return, it promises to pay a fixed rate of interest – known as the coupon – at regular intervals and return the original sum (the principal) at a specified date in the future.

Governments issue bonds constantly to fund public services, infrastructure, and to manage national debt.

In the UK, government bonds are called ‘gilts’ – a nod to the gilded edges of the original paper certificates.

In the US they are called Treasuries; in Germany, Bunds; in Japan, JGBs. Different names, same basic idea.

When you buy a newly issued government bond, you know exactly what you’re getting: say, 4% interest per year for ten years, and your money back at the end. Simple enough.

Here is where it gets interesting.

Once a bond has been issued, it can be bought and sold on financial markets and its price moves with supply and demand, just like shares. This is where the concept of ‘yield’ comes in.

The coupon on a bond is fixed. But if the price of that bond falls in the market, the fixed interest payment represents a higher return relative to what you paid, so the yield rises.

Price and yield always move in opposite directions.

This relationship is central to understanding why politics, economics and financial markets are so closely linked.

When investors grow nervous about a government’s finances – perhaps because of an unexpected spending announcement, a chaotic budget, or signs of political instability – they become less willing to hold that government’s bonds. They sell. Prices fall. Yields rise.

This is precisely what happened in the UK in September 2022, when the then-Chancellor’s mini-budget spooked markets with unfunded tax cuts.

Gilt yields spiked sharply, sending tremors through pension funds and mortgage markets.

More recently, periods of political uncertainty have triggered similar, if less dramatic, reactions.

Importantly, rising gilt yields are not just a market story. They have real-world consequences.

Higher government borrowing costs can feed through to higher mortgage rates, more expensive business lending, and increased costs for servicing national debt.

When bond markets move, the broader economy often feels the effects.

The UK gilt market, while important, is one part of a much larger global picture.

US Treasuries are considered the bedrock of the global financial system – the ultimate “safe haven” asset.

In times of global crisis, investors typically pile into Treasuries, pushing prices up and yields down. They are the benchmark against which almost every other bond in the world is measured.

German Bunds play a similar role within the eurozone. Their yield is used as the reference point for European sovereign debt, with the borrowing costs of countries like Italy or Spain measured by how much more they pay compared to Germany – a gap known as the “spread.”

Emerging market government bonds – issued by countries in Latin America, Asia, or Africa – tend to offer higher yields to compensate investors for taking on greater political and economic risk.

Across the bond market, the relationship between risk and return remains fundamental: the greater the perceived risk, the higher the yield investors demand.

Governments are not the only borrowers. Large companies – from airlines and pharmaceutical firms to supermarkets and technology giants – also borrow money through bond markets to fund operations and growth.

Corporate bonds function much like government bonds, but they usually offer higher yields because companies generally carry a greater risk of default. Governments can raise taxes or issue more debt; companies do not have the same flexibility.

To attract investors, companies must therefore offer higher yields than comparable government bonds.

The additional return investors receive for taking on this extra risk is known as the “credit spread”. When economic conditions deteriorate or investors become more cautious, these spreads tend to widen.

Simple, in theory. But how do bonds actually fit into an investment portfolio?

The traditional answer is: as a counterbalance to shares.

Equities offer the prospect of strong long-term growth, but they are volatile – markets can fall sharply and take time to recover.

Bonds, by contrast, provide a steadier income stream and tend to be less volatile. When equity markets fall sharply, investors often move into bonds, pushing their prices up.

This logic underpins the famous “60/40 portfolio” – a rule of thumb that suggests holding 60% in equities and 40% in bonds.

For decades, this split was the backbone of cautious investing: equities driving growth, bonds providing stability and cushioning losses in downturns.

However, the 60/40 model faced a serious test in 2022, when surging inflation dragged both equities and bonds lower at the same time – a painful reminder that no investment rule survives every environment.

Yet the underlying logic remains sound: spreading risk across different asset classes still makes sense over longer time horizons, and within bonds themselves, active asset allocation – adjusting where you are invested as conditions change – can make a meaningful difference when markets turn turbulent.

Where bonds really earn their place, though, is in shaping a portfolio around an investor’s stage of life.

In earlier years, with decades of growth ahead, it makes sense to accept more volatility in pursuit of higher returns from equities.

As retirement draws closer, the calculus shifts: a gradual move towards bonds trades some of that upside for steadier income and greater predictability – a reasonable bargain when you have less time to ride out a market storm.

Bond markets can seem dull, remote and technical – the preserve of traders and economists.

But as recent headlines have shown, they sit at the heart of how governments are held accountable for their finances, and how the cost of borrowing ripples through the economy.

For investors, understanding bonds is not merely academic.

Whether held directly, via funds, or as part of a pension, bonds are almost certainly part of your financial life already.

Knowing what moves them, and why, is a good step to understanding what your money is actually doing.

An expert financial adviser can help you to decide on what role bonds could play in your portfolio, taking into account your circumstances and your approach to investment risk.

Get in touch with one of our advisers today to find out more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

A bond is a loan made by investors to a government or company in exchange for regular interest payments and repayment of the original amount at maturity.

Gilt yields are the returns investors receive from UK government bonds. When gilt prices fall, yields rise.

Bond yields and prices move in opposite directions because the fixed interest payment becomes more valuable relative to a lower purchase price.

Bonds are generally considered less volatile than shares, but they still carry risks including inflation risk, interest rate risk and default risk.

Government bonds are issued by countries to fund public spending, while corporate bonds are issued by companies to raise capital for business activities.

A 60/40 portfolio is an investment strategy that allocates 60% to equities and 40% to bonds to balance growth and stability.

Government bond yields influence borrowing costs across the economy, including mortgage rates and business lending rates.

Yes. Beginners can invest in bonds directly or through bond funds, ISAs, pensions and diversified investment portfolios.

“Sell in May and go away” is one of the oldest sayings in the investment world.

But is it really a good idea?

Here we look at why following this maxim may cost you money instead of making it.

“Sell in May and go away” has been part of market folklore for the best part of three centuries.

The full version – “Sell in May and don’t come back until St Leger’s Day” – dates back to a time when London’s bankers, brokers and aristocrats would shut up shop in May, head to their country estates for the summer, and return to the markets only after the famous horse race at Doncaster in September.

Trading volumes really did thin out, and a seasonal pattern of weaker summer returns became part of investing lore.

This idea then stuck around.

Academic work from Bouman and Jacobsen’s 2002 study in the American Economic Review, examined data from 37 countries and confirmed that in many global markets, returns between November and April have, on average, been higher than those between May and October – a pattern the authors found in UK data going back as far as 1694.

So the seasonal effect is real, but, as we will see, the practical lesson investors draw from it is usually the wrong one – and times have changed.

Today’s markets look nothing like the time that gave us the rhyme.

Trading is global, electronic and continuous; corporate earnings, central bank decisions and major economic news arrive throughout the year; and the average investor is a long-term saver building a pension, not a banker decamping to a country house.

Crucially, even where a small seasonal pattern survives in the average, the gap is far too narrow to overcome the cost of being out of the market when summers turn out to see strong returns.

Research from American Century Investments, published in April 2026, puts this in numbers that make it a little easier to understand.

Looking at 50 years of S&P 500 data from 1976 to the end of 2025, the study shows that a $1,000 investment left alone the whole time would have grown to roughly $294,800.

The same $1,000 switched out of the market each May and back in each November would have grown to just $46,400 – less than a sixth of the total secured by staying invested.

This is quite a staggering difference in returns that really shows the weakness of blindly following this phrase.

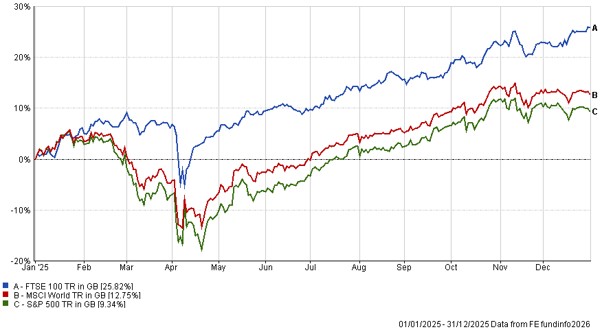

If any year was made to test the “Sell in May” theory, it was 2025.

Markets started that year on somewhat shaky ground. The Trump administration’s “reciprocal” tariffs sent the S&P 500 down nearly 19% from its February peak by early April, and headlines were dominated by fears of a global growth shock, sticky inflation and a brewing trade war.

For an investor watching the news on the morning of 1 May, the temptation to follow the adage and step away might have been understandable.

It would also have been very costly.

From the end of April through to the S&P 500’s new all-time high on Christmas Eve, the index, in GBP, returned 24%, and finished the full year up 9.8% – a strong return even after meaningful sterling appreciation against the dollar.

The below chart shows the returns over the full year, along with the volatility we saw in March and April.

In sterling, the MSCI World rose 13.2% and the FTSE 100 25.8%. The summer months – the very period the saying tells investors to avoid – carried a lot of the returns that year.

The table below shows total returns in GBP from 30 April to year-end for the three major indices, across four recent years that all had reasons to be nervous in the spring.

| Year | S&P 500 | FTSE 100 | MSCI World |

| 2020 | +20.4% | +11.8% | +22.5% |

| 2023 | +14.1% | +0.8% | +11.7% |

| 2024 | +17.9% | +2.7% | +13.5% |

| 2025 | +23.1% | +19.4% | +21.7% |

Each of these years had a clear excuse to head for the exit in May: a pandemic in 2020; lingering inflation and recession fears in 2023; election uncertainty and high valuations in 2024; tariff shocks and geopolitics in 2025.

In each case, every one of the three indices delivered a positive return from 30 April to year-end – and in most cases a meaningful one.

An investor who sold in May and waited would have missed real returns in every year shown.

None of this is to suggest that markets only ever go up, or that volatility through the summer should be ignored.

Drawdowns happen, sometimes sharply, and a well-constructed portfolio should already reflect a sensible balance between growth assets and diversifiers.

But the lesson of the last decade, and emphatically of 2025, is that the cost of being wrong on a market-timing call has been far greater than the cost of riding out the noise.

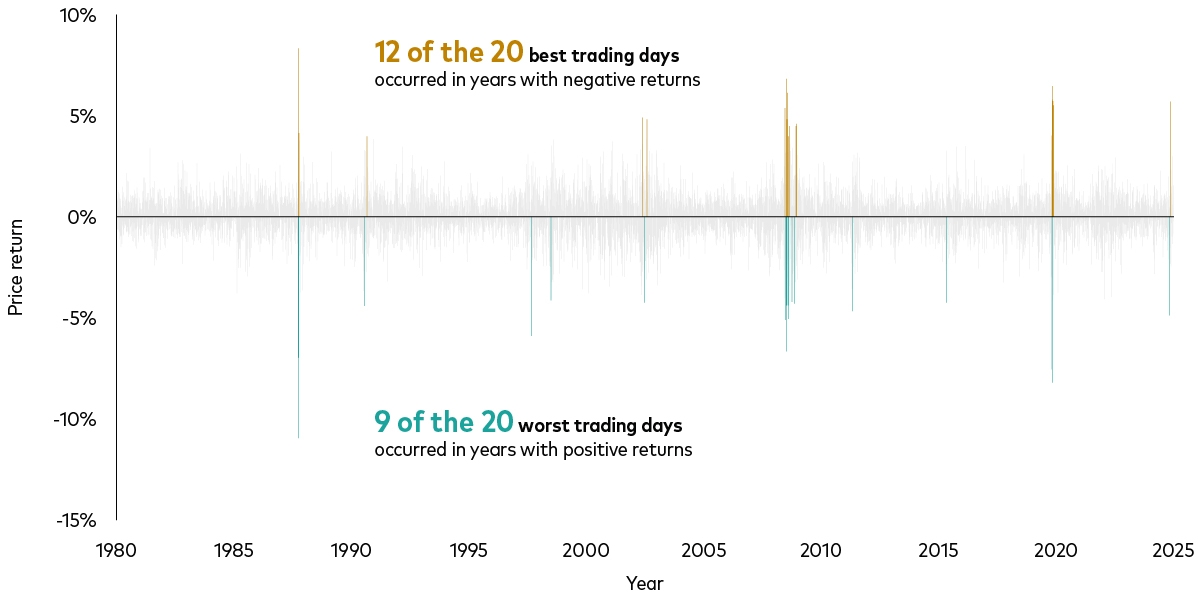

The best days in markets tend to cluster around the worst, and missing only a handful of them has historically taken a heavy toll on long-term returns.

A portfolio spread across regions, sectors and asset classes reduces the temptation, and the need, to react to short-term headlines.

Active rebalancing within a clear strategic framework – not wholesale switches in and out of the market – is what tends to help compound wealth over time.

Catchy as it is, “sell in May and go away” belongs to a different era.

The investors who have done best in recent years have been those who tuned out the seasonal noise, stayed broadly invested in line with their long-term plan, and let their portfolios do the work they were designed to do.

An expert financial adviser can help you to decide on an investment plan, taking into account your circumstances and your approach to investment risk.

They can also help you to stay focused on your financial goals rather than reacting to short-term or seasonal market movements.

Get in touch with one of our advisers today to find out more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

The phrase refers to an old investment strategy where investors sell shares in May and return to the market later in the year, traditionally around September.

While the seasonal trend has existed historically, modern markets are far more global and continuous. Many investors who followed the strategy in recent years would have missed strong market gains.

Historical data generally shows that long-term investors who stay invested tend to outperform those who frequently move in and out of the market.

Remaining invested allows investors to benefit from compounding growth and avoid missing the market’s strongest recovery periods, which often occur unexpectedly.

Selling during market downturns can lock in losses and increase the risk of missing rebounds that may significantly boost long-term returns.

“Timing the market” involves trying to predict short-term movements, while “time in the market” focuses on long-term participation and compounding growth.

Diversification spreads investments across different regions, sectors and asset classes, helping reduce overall portfolio risk and reliance on any single market event.

Rather than making reactive decisions, investors are often better served by following a long-term investment plan aligned with their goals and risk tolerance.

Yes. A financial adviser can help investors build a suitable portfolio, manage risk and stay focused on long-term objectives during uncertain market periods.

In times of market volatility – such as those we have seen in recent weeks – it’s natural to get nervous.

However, ups and downs in markets are a normal part of investing. Periods of uncertainty regularly cause markets to rise and fall in the short term.

Market volatility can trigger emotional responses such as fear or panic. Making decisions based on short-term emotions can lead to poor outcomes.

History shows that while markets can be volatile, they have tended to recover over time. Long-term growth has been delivered despite setbacks, recessions and global events.

Fairstone Investment Management have worked with Vanguard and J.P. Morgan Asset Management, two of our partners, to provide insight into why staying invested is normally the right thing to do.

A common reaction during market falls is to move into cash and wait for a better time to invest again.

While this may feel reassuring, evidence shows that timing the market is extremely difficult.

Some of the strongest market days often occur close to the weakest. Missing these recovery days can significantly reduce long-term returns.

Past performance is not a reliable indicator of future results.

Source: Vanguard calculations in GBP, based on data from Refinitiv, as at 31 December 2025.

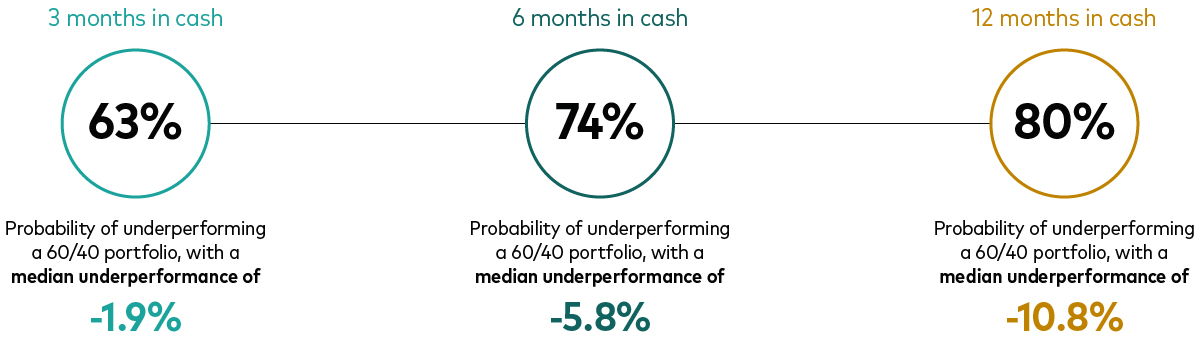

As a result, moving to lower risk investment such as cash might feel reassuring but understanding when to reinvest is a tough decision.

Long periods out of the market can reduce returns:

Past performance is not a reliable indicator of future results.

Notes: The chart shows the distribution of excess returns of cash over a global 60% equity / 40% fixed income portfolio for the 3-, 6- and 12-month periods after 2-month total returns of global equities were below 5%

Source: Vanguard calculations in GBP, based on data from Refinitiv, as at 31 December 2025.

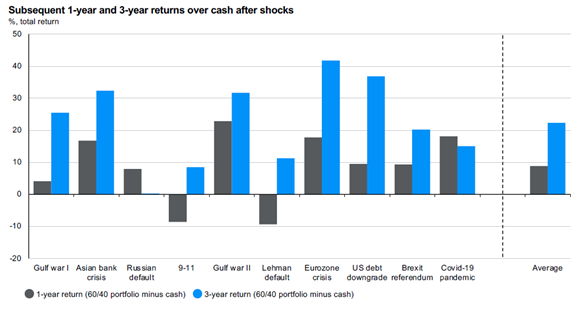

Even based on valuations the day before a market downturn the returns after 1 and 3 years have usually been positive:

Past performance is not a reliable indicator of future results.

Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. 60/40 portfolio is constructed using S&P 500 Index and S&P 10-year US Treasury Note Futures Index. Cash: ICE USD LIBOR (3M). Return calculation begins at the end of the month prior to the shock. Guide to the Markets – UK. Data as of 31 December 2024.

Holding cash can feel safe during turbulent markets, but cash comes with its own risks — particularly inflation.

Over long periods, inflation can erode spending power. Historically, diversified investment portfolios have tended to perform better than cash over time:

J.P. Morgan Asset Management. For illustrative purposes only, assumes no return on cash and an inflation rate of 2%. Past performance is not a reliable indicator of current and future results. Guide to the Markets – UK. Data as of 31 December 2024.

Investment plans are built to anticipate both good and difficult markets.

If your long-term goals and circumstances have not changed, short-term market movements alone rarely justify major changes.

The objective is not to avoid downturns, but to manage them sensibly in pursuit of long-term goals.

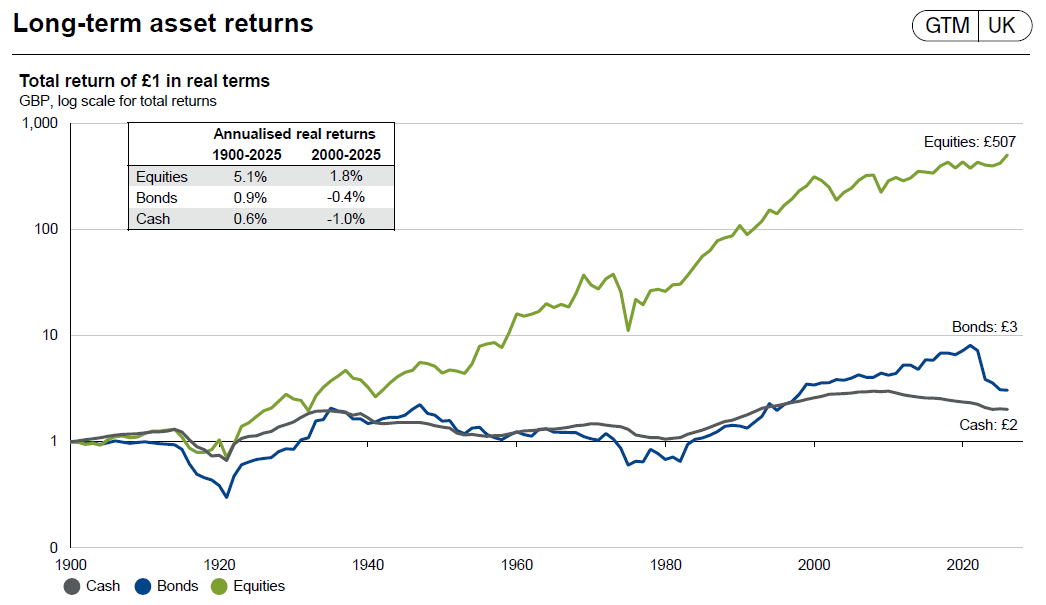

Historical performance shows value in investing in equities over the long term:

Past performance is not a reliable indicator of future results.

Source: Bloomberg, Dimson, FactSet, FTSE, J.P. Morgan, Marsh and Staunton ABN AMRO/LBS Global Investment Returns calculated from the Yearbook 2008, J.P. Morgan Asset Management. Equities: FTSE 100; Bonds: J.P. Morgan GBP Government Bond Index; Cash: three-month GBP LIBOR (prior to 2008 cash is short-dated Treasury bills). Guide to the Markets – UK. Data as of 31 December 2024.

Portfolios run by Fairstone Investment Management are managed tightly within certain risk targeted constraints.

This of course does not mean that a portfolio might not reduce in value but it does mean that downturns should be aligned with your long term goals and your own attitude to risk.

Further, our portfolios are well-diversified. Investing across different asset types and regions helps manage risk.

Diversification cannot eliminate losses, but it can reduce the impact of individual market events and support staying invested.

Market volatility can trigger emotional responses such as fear or panic. Making decisions based on short-term emotions can lead to poor outcomes.

A Fairstone adviser can help you to stay focused on goals rather than short-term market movements. If you have any concerns at all, please speak to an adviser.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

Over the past few years, the investment landscape in the UK has changed dramatically.

Recent research shows that around 38% of UK adults now invest – just over one in three.

This is a figure that has risen steadily since the beginning of the decade when around one in four UK adults invested.

Some of these new investors are using technology in the form of investment platforms to do it themselves.

While this approach can be appealing, it does have its limitations, as we explore in this article.

Starting on your own is simple, accessible, and gives you control.

DIY investing appeals because of flexibility, lower fees and the ability to learn as you go.

For many people, that’s exactly what they need to build confidence and it’s a great starting point.

But as your financial life becomes more complicated, the question often shifts from “How do I start?” to “What’s the smartest way to move forward?”

That’s where informed planning and professional advice begins to make a meaningful difference.

DIY investing can be a great fit when:

Many people value this independence at the start of their investing journey. It builds good habits and gives you a better understanding of how your money works.

For some, that’s enough. For others, life becomes more complicated and they don’t want to get things wrong.

There’s usually a clear point where the conversation shifts from picking investments to financial planning.

In my experience, people tend to look for guidance when one or more of the following starts to apply:

Multiple pensions, ISAs, workplace schemes, cash savings and investment accounts can make it increasingly difficult to stay organised.

Choosing the right tax wrapper, managing allowances and understanding how to make money work harder after tax can have a huge impact over decades.

One of the hardest parts of investing is staying calm when markets fall or headlines turn, as has been the case in recent weeks with the unrest in the Middle East.

A lot of long-term damage happens when decisions are driven by emotion, not strategy.

Investing isn’t just about buying funds, it’s about aligning decisions with life goals, whether that’s retirement, children’s education, or future financial independence.

It’s often at this point that people realise the difference between having investments and having a plan.

The value of advice is well documented.

Analysis from Vanguard shows that professional advice delivered consistently and in a structured way can add around 3% per year in long term value.

This isn’t through beating the market, but through:

It’s the combination of these elements that makes the difference.

Good advice isn’t about predictions or timing. It’s about giving you confidence, structure and clarity so you can focus on the parts of life that matter more.

Taking your first steps through a DIY platform is a great place to begin.

It builds confidence and gets your money working.

But as your financial situation evolves, the decisions naturally become more layered and more impactful.

You don’t need advice to start investing.

But many people find it helpful when the decisions get bigger.

For more information on how investments can fit into your financial plan, get in touch with one of our advisers.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

Yes, DIY investing can be a great way to start, especially if your finances are simple and you want to learn. It offers flexibility, control, and lower costs.

You should consider a financial adviser when your finances become more complex, tax planning becomes important, or you want a structured long-term plan.

Investing focuses on selecting assets, while financial planning aligns your investments with long-term goals like retirement, education, and wealth preservation.

Yes, research suggests financial advice can add long-term value through tax efficiency, behavioural coaching, and cost management rather than market outperformance.

Yes, many investors use a hybrid approach—managing some investments themselves while seeking advice for complex decisions or long-term planning.

Common risks include emotional decision-making, poor diversification, tax inefficiency, and lack of a clear long-term strategy.

Over recent months, we have seen commodities investing move firmly into the spotlight.

Gold has been front and centre of the conversation, but it’s not the only area attracting attention.

We have also seen growing interest in energy, industrial metals and agricultural markets, as these assets tend to re-enter the discussion when investors are thinking about inflation resilience, geopolitical uncertainty, or simply improving diversification in a balanced portfolio.

Commodities can play a useful role in portfolios, but they are also easy to misunderstand.

Prices can be volatile, different commodities behave in very different ways, and the route you choose – owning the commodity itself versus investing in the companies that produce it – can materially change the risk and return profile.

Here we set out the key points to help investors and advisers frame the discussion sensibly.

Gold has a long history as a defensive asset.

Unlike shares or bonds, it isn’t linked to the fortunes of a single company or government, and it doesn’t rely on an issuer’s promise to pay.

The “no-one else’s liability” feature is one reason investors often gravitate towards gold when confidence is shaken.

Gold is also scarce, durable and globally recognised, which helps explain why it has been treated as a store of value over time.

In periods where inflation worries rise, geopolitical risk intensifies, or markets become unsettled, gold can attract demand as a form of insurance within a broader portfolio.

Interest rates are another important influence.

Gold doesn’t produce an income, so it can look more attractive when the return available on cash and bonds (after inflation) feels less compelling.

When that “opportunity cost” falls, investors can be more willing to hold an asset whose value is driven primarily by supply and demand, rather than by income.

The key caveat is that “safe haven” does not mean “always goes up when markets fall”, and it certainly does not mean “low volatility”.

Gold can experience sharp drawdowns, and there are periods where it falls alongside risk assets – particularly when investors are rushing to sell all assets, the US dollar strengthens, or real (inflation-adjusted) interest rates rise.

Recent price action is a timely reminder of this volatility.

Gold’s strong rise has been accompanied by larger day-to-day moves than many investors associate with a defensive holding.

When investor positioning becomes crowded, or when flows into and out of exchange-traded products accelerate, price action can become more reactive and caught up with broader shifts in sentiment.

The key message really is that gold can be a useful diversifier and a potential stabiliser in certain environments. However, but it should be held with realistic expectations.

It is not a guaranteed hedge, and it can be volatile.

When investors talk about “commodities”, they can be referring to a wide range of assets.

Broadly, the exposure tends to fall into a few categories as follows:

These are closely linked to global growth, manufacturing and infrastructure spending.

They can benefit when global growth is positive, activity is strong and are often associated with long-term themes such as electrification, grid upgrades and more recently the data-centre build-out.

The trade-off is cyclicality: industrial metals can fall sharply when growth slows, or demand expectations weaken.

These are typically among the most economically sensitive commodity exposures.

Energy prices respond quickly to supply disruptions, geopolitics and production decisions – as we have seen in recent weeks with events in the Middle East.

For investors, energy can sometimes offer inflation sensitivity, because energy costs feed directly into wider price pressures.

However, energy markets are among the most volatile, with rapid swings driven by events rather than gradual fundamentals.

Risks can therefore be driven quite dramatically by timing, and reversals can be sudden.

Agriculture is driven by a different set of factors – weather patterns, crop yields, fertiliser costs and trade policy. This can make it appealing from a diversification perspective.

The drawback is unpredictability: weather and seasonality can create sharp price moves, and local disruptions or policy decisions can have outsized effects.

These metals can behave quite differently from gold.

Silver, for example, has both “monetary” characteristics and meaningful industrial demand (solar panels and datacentres as examples). This can make it more sensitive to the economic cycle.

Platinum and palladium have also historically been tied to industrial uses and evolving technology trends.

These markets can be smaller and less liquid than gold, which can mean more volatility.

Commodities are rarely a “core” holding like equities or bonds, but they can play valuable supporting roles when used thoughtfully and sized appropriately.

Commodity returns are often driven by different forces, supply constraints, weather, geopolitics and inventory cycles.

This can help diversify a portfolio that is otherwise dominated by equity and interest-rate risk.

Commodities sit closer to the real economy. In certain inflationary environments, they can help offset the impact of rising input costs and price pressures. This is particularly the case with energy and some industrial commodities.

That said, outcomes vary significantly by period and by commodity.

Gold can provide a form of insurance in certain types of market stress, especially where confidence in currencies or financial stability is questioned.

However, insurance is not free: gold can underperform for long stretches and may disappoint in some equity drawdowns.

Commodities can deliver strong returns when supply is constrained, demand surprises to the upside, or inflation shocks push prices higher.

However, these periods can be episodic rather than steady. It is important not to extrapolate short-term performance into a long-term expectation.

There are two main ways investors can access exposure to commodities with each having its own advantages and disadvantages.

This is typically achieved through exchange-traded products or funds that provide exposure either to the physical commodity (more common for precious metals) or via futures markets (common for energy, industrial metals and broad commodity baskets).

Direct exposure can provide a cleaner link to commodity prices and may be more effective for diversification and inflation sensitivity.

However, futures-based exposure can introduce additional drivers of return, particularly the mechanics of rolling futures contracts.

The alternative route is to invest in the companies that produce the commodity.

This can provide potentially higher returns and operational leverage when commodity prices rise.

However, it also introduces equity market risk and company-specific factors such as costs, debt levels, regulation, politics, management decisions and broader market sentiment.

Commodities can be a helpful portfolio tool, but they require careful sizing and clear expectations.

Volatility can rise quickly, individual commodities can behave very differently, and product structure matters.

For UK investors, currency is another consideration. Many commodities are priced in US dollars, so currency moves can materially influence returns.

Commodities can offer diversification, inflation sensitivity and, in the case of gold, a potential form of portfolio insurance.

But they are not a one-way bet, and recent moves in gold are a reminder that even “defensive” assets can be volatile.

The most important decisions are not just whether to invest in commodities, but which exposures to use, how to access them, and how much is appropriate given an investor’s objectives and risk tolerance.

An expert financial adviser can help you decide whether investing in commodities is right for you, your circumstances and your approach to investment risk.

Get in touch with one of our advisers today to find out more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

Gold is often considered a safe haven because it is not tied to any single government or company and has historically retained value during market stress. However, it can still be volatile and does not always rise during equity downturns.

Some commodities, particularly energy and industrial metals, can perform well during inflationary periods because rising input costs push prices higher. However, performance varies by commodity and economic cycle.

Direct commodity exposure (often via ETFs or futures) tracks the price of the commodity itself. Mining or energy stocks are equities and carry company-specific risks such as management decisions, debt levels and broader stock market movements.

Commodities can play a supporting role in a diversified portfolio, particularly for inflation sensitivity and diversification. They are typically not core holdings and should be sized appropriately given their volatility.

Because most commodities are priced in US dollars, currency movements can significantly impact returns for UK investors. A strengthening pound can reduce returns, while a weakening pound can enhance them.

The acronym HENRY – High Earner, Not Rich Yet – has gained in popularity in recent years – and for good reason.

The term describes a growing cohort of people who look financially successful from the outside but feel increasingly stretched once the real numbers are laid out.

HENRYs are:

Yet many describe the same frustration: earning more doesn’t feel like getting ahead.

The reason, more often than not, appears when children arrive.

The UK tax system creates a sharp financial turning point around £100,000 of adjusted net income.

This is known in many circles as the £100k tax trap.

Once that threshold is crossed, families can lose access to key childcare support, including 30 hours free childcare and Tax-Free Childcare.

This support can be worth roughly £7,000 to £8,000 per year for a typical nursery-age child, depending on fees and location.

At the same time as losing this support, the tax-free personal allowance begins to taper away, reducing by £1 for every £2 earned above £100,000.

When you combine the loss of childcare support with higher effective tax rates, families can find themselves in a situation where earning more produces very little improvement in real disposable income – the £100k tax trap.

Recent commentary has highlighted how this is influencing real-life decisions.

Some professionals are now openly questioning whether progressing beyond certain income levels actually improves their standard of living.

From my perspective, this is not theoretical. It shows up in meetings I have with clients every week.

You can see how crossing £100,000 can actually leave some families feeling worse off, which feels completely counter-intuitive.

The consequences are real: some delay having children, others decide to stop at one child.

When financial systems create disincentives around family life, behaviour changes.

Is Elon Musk right? He has repeatedly warned about declining birth rates and long-term population trends, and while his views are often debated, the underlying point is hard to ignore: financial pressure increasingly influences family decisions.

The typical story is familiar.

A promotion or bonus pushes income above the threshold.

Nursery fees are already high and suddenly support disappears. Monthly outgoings rise just as income is supposed to bring more comfort.

The emotional response is usually confusion rather than tax planning ambition.

Clients aren’t trying to avoid success. They simply expected that earning more would make life easier.

Instead, they feel stuck.

This is the core HENRY experience: high income, high fixed costs and very little sense of momentum. Caught in the £100k tax trap.

What many families don’t realise is that the threshold is based on adjusted net income, not simply salary.

Pension contributions and other reliefs can materially change that figure.

This is where proper financial planning changes the conversation.

I regularly see situations where restructuring income or increasing pension contributions improves long-term wealth while also preserving access to childcare support.

On paper, it may look like a short-term sacrifice. In reality, it can significantly improve both current cashflow and future financial outcomes – and free you from the £100k tax trap.

When you model these decisions properly, the results are often surprising.

Families can see clearly how a relatively small structural adjustment today can reshape the next 10 or 20 years.

Childcare is simply exposing a broader issue facing high earners.

Income alone does not create financial security. Without structure, even strong salaries can leave households feeling dependent on the next payslip.

The childcare years are temporary, but they are often when you make the biggest financial decisions.

Done well, they become a period of acceleration rather than pressure.

Many high earners assume that financial comfort arrives automatically once income reaches a certain level.

In reality, the system becomes more complex exactly at the point where family life becomes more expensive.

The solution is not to avoid earning more or to step back from progression. It is to understand the rules well enough to work with them, not against them.

Because ultimately, the goal is not simply to earn well. It is to feel in control of what that income actually delivers.

Sitting down with a professional financial adviser and looking carefully at your income and outgoings will help you to create a robust, flexible financial plan – not only for when children are young, but also for your future after they have grown up.

It could free you from the £100k tax trap and help you see financial success for what it is – a boon and not a burden.

Get in touch with one of our advisers today to find out more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

The £100k tax trap occurs when adjusted net income exceeds £100,000, triggering the loss of personal allowance and childcare benefits, creating a 60% effective marginal tax rate for some earners.

Families can lose access to 30 hours free childcare and Tax-Free Childcare once adjusted net income exceeds £100,000.

Adjusted net income is your total taxable income minus certain reliefs, such as pension contributions and Gift Aid donations.

Yes. Pension contributions can lower adjusted net income, potentially restoring childcare eligibility and reducing effective tax rates.

High fixed costs, tax tapering, childcare fees and reduced allowances can significantly reduce real disposable income despite six-figure salaries.

No. The better approach is structured financial planning to optimise income and long-term wealth rather than limiting career progression.

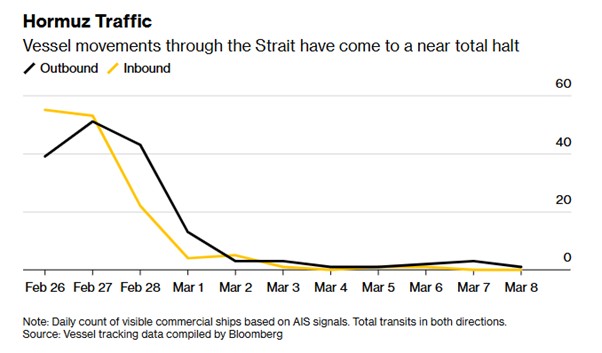

The last couple of weeks have delivered a steady stream of unsettling headlines from the Middle East.

Oil prices spiked, some equity markets fell, and commentators rushed to predict what happens next.

It’s natural to feel uneasy in moments like this. But for long‑term investors, the best response is usually the most straightforward: keep calm, stay diversified, and stick to the plan you built around your goals.

Recent military escalation in and around Iran has disrupted shipping through the Strait of Hormuz, a narrow channel that normally carries a large share of the world’s oil and gas:

When those flows look threatened, energy prices can jump quickly and knock confidence across wider markets.

We’ve seen exactly that pattern: crude oil briefly pushed into triple‑digit territory before easing back as talk of strategic stockpile releases and naval escorts helped steady nerves.

Equity markets sold off at first, then showed signs of resilience as energy prices backed off their highs.

In short, it has been a fast‑moving situation – but not an unfamiliar one for markets.

Diplomacy continues in the background and policy responses are on the table.

Authorities have discussed reserve releases to cushion supply, and any reopening of shipping lanes would help prices normalise.

The timing is uncertain, it remains a fast-moving situation and headlines may stay volatile for a while yet.

That said, markets often adjust faster than the news flow, especially when investors can see a path to stabilisation.

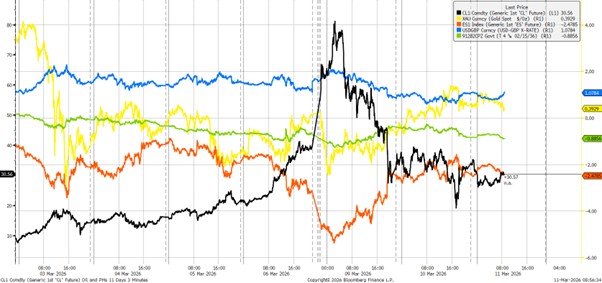

Oil jumped (black line in the chart below) as shipping slowed, before retracing a good portion of the move when signs of policy support and limited tanker escorts emerged. Large daily swings have been common.

The initial “risk‑off” reaction hit most equity regions. Energy companies outperformed on the way up, then gave back some gains as crude eased.

US equities (orange line in the chart below) have been relatively resilient versus other regions as the US is seen as less exposed to the volatility.

Government bonds (10-year US Treasuries in green line), which often rally when shares fall, were tugged in two directions – by safe‑haven demand on the one hand and by renewed inflation concerns on the other (higher oil can keep inflation sticky). That’s one reason returns have varied by market and maturity.

The US dollar firmed as investors sought safety, which matters for UK investors holding overseas assets (USD/GBP in blue line).

Gold was volatile (yellow line)—useful as a diversifier over time, but not a guarantee of gains on every risk‑off day.

As oil pulled back from its peak, market anxiety measures cooled from their initial spike, reminding us that conditions can change very quickly when policy signals improve.

None of this is to minimise events; it’s to put them in context.

Markets have navigated many geopolitical shocks over the decades, and while the path is rarely smooth, the longer‑term pattern has been one of recovery as fundamentals reassert themselves.

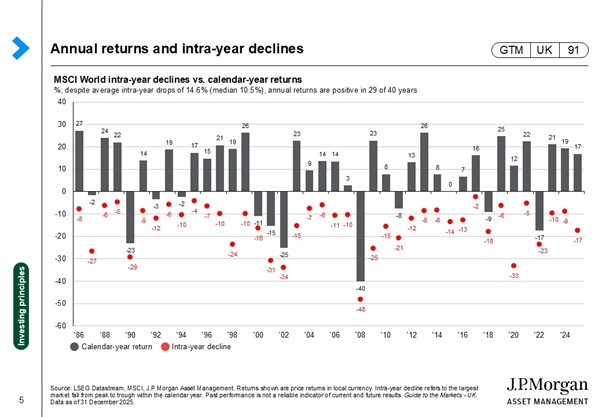

Every year experiences pullbacks. A long-running analysis by J.P. Morgan Asset Management (see chart below) shows that, despite an average intra‑year decline of roughly 15% in global equities (red dots in the chart below), calendar‑year returns (grey bars) have still been positive most of the time.

In other words, setbacks are common, recoveries are too.

Selling after markets fall often locks in losses and risks missing the recovery.

Fund‑flow data show investors tend to withdraw money near market troughs – exactly when patience is most valuable.

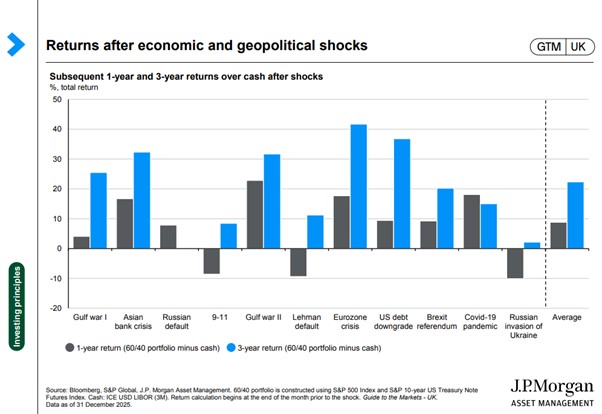

More importantly for today’s environment, the chart below shows that a simple 60/40 mix of shares and bonds has beaten cash after past geopolitical and economic shocks more than 70% of the time over the subsequent year – and every time over the subsequent three years in the sample J.P. Morgan studied:

The longer you stay invested, the lower the historical odds of losing money—particularly in a balanced portfolio.

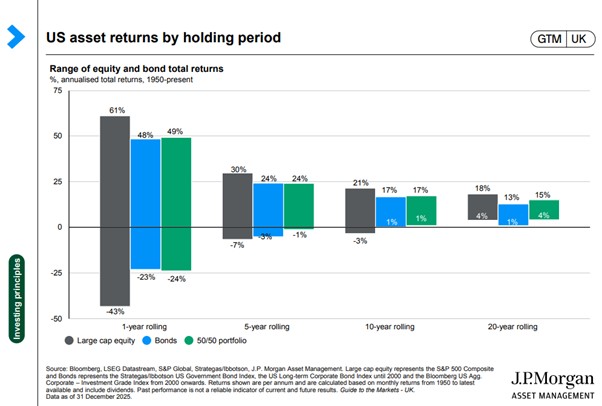

Combining time, compounding and regular reinvestment has been a powerful driver of long‑term outcomes as the final chart below shows; while over short time periods the range of returns can be wide and sometimes negative, the longer the investment time period the more predictably positive returns become.

Whilst the current time is unsettling for investors, it is important to remember that the fundamental principles of investing remain the same.

Your portfolio was built around your personal objectives and time horizon.

Short‑term market moves – especially those driven by geopolitics – don’t usually warrant wholesale changes to a long‑term plan.

A balanced approach helps cushion the journey and has historically rewarded patient investors, including through past crises.

Cash has a role for near‑term needs and as a stabiliser, but moving large amounts out of markets after shocks typically hurts long‑term results – and inflation quietly chips away at purchasing power.

Rather than making big directional calls, periodic rebalancing back to your agreed mix naturally trims assets that have risen and adds to those that have fallen, keeping risk aligned with your goals.

We are monitoring developments daily – including energy market dynamics and any policy responses – and we’ll adjust where needed within the discipline of your strategy.

If your circumstances change, please let us know so we can reflect that in your plan.

Get in touch with an adviser to discuss your current situation, any concerns you have or adjustments you’re thinking about making.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

With Easter just around the corner, I’d like to talk about chocolate.

In fact, one particular type of chocolate: the Freddo bar.

Those of a certain age may remember this piece of confectionery with great fondness – not so much for its taste, which was, well, chocolatey, but more for its value for money.

Freddos were cheap.

So cheap in fact that right up until 2006 you could buy one for as little as 10p.

Sadly those days are long gone.

A Freddo these days will set you back around 35p and, in some cases, as much as £1 a bar.

Even with increases in pocket money, that chocolate hit is no longer as attainable as it once was.

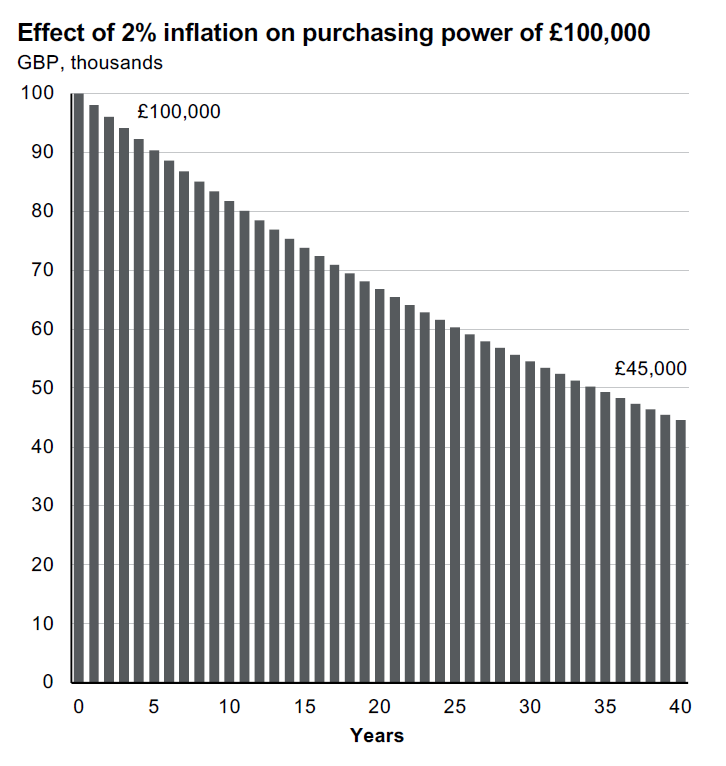

The plight of the once-cheap Freddo illustrates an important point about the value of money: it never stays the same.

Inflation is the silent assassin of your wealth, affecting everything from buying a once in a lifetime holiday to grabbing a sweet snack.

While the rate of inflation fluctuates, it rarely if ever recedes. Just like the oceans continually erode the coastline, inflation does the same to cash in bank accounts.

The effect on your cash over time really adds up – in a bad way. This picture tells the real story:

It’s a sobering illustration of the power of inflation – even more so when you realise that this is inflation at just 2% rather than the 3% it was in January, let alone the 10%+ it hit in January 2023.

If you still think that ‘cash is king’ or that your money is always ‘safe’ in cash, you may want to think again.

The unfortunate fact of the matter is that interest rates on bank or building society deposits rarely keep pace with inflation.

Your money may be ‘safe’ in a savings account (providing you have deposits of £120,000 or less and your account provider is covered by the FSCS deposit guarantee). However, the value that it represents is not.

Building up an ‘emergency’ fund of savings which you can quickly and easily access is a great idea, but putting all your ‘rainy day’ money in such an account risks losing some of the value of what you have put aside, particularly over a longer timescale.

We in the financial services sector rightly have to warn of the risk involved in investing – that returns are not guaranteed, the value of what people invest can go down as well as up and people may not get back the full amount they invest.

However, there is also a type of risk involved in placing all your spare funds in a savings account: you may find your money is not worth as much as you had thought and, with tax rates on interest from non-ISA savings accounts increasing, you may not earn as much in interest as you had anticipated.

You may also miss out on the additional returns which could have come with investing over the long term – while past performance does not mean the same will be repeated in the future, it remains a fact that over a long period of time, returns from equities have typically outperformed cash by several multiples.

Financial decisions should always take into account your individual circumstances, but taking a balanced approach to saving and investing could help to mitigate both types of risk involved.

And you could end up being able to buy a Freddo or two.

It’s easy to find out more about how investing has the potential to improve your financial future, what products are out there and how to match your goals with your appetite for risk.

Get in touch with a Fairstone adviser to discover more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

The deadline to maximise your investment in tax-free ISAs (Individual Savings Accounts) is rapidly approaching.

The ISA deadline comes at the end of the current 2025/26 tax year, which is April 5, 2026.

This is the last chance to use up your annual allowance before it expires, with the new tax year starting on April 6, 2026.

You can invest up to a maximum of £20,000 per person in any ISA in any one tax year.

This allowance has to be used during the course of that tax year and cannot be “rolled over” into the subsequent tax year.

It is a “use it or lose it” allowance.

At the current moment in time, the £20,000 maximum can be invested across any number of ISA types, including cash ISAs, stocks and shares ISAs or Lifetime ISAs.

You can invest in more than one ISA account during any tax year.

However, your total ISA investments cannot add up to more than £20,000.

No. Putting money into a Junior ISA does not affect your personal adult allowance of £20,000 per tax year.

The Junior ISA has its own separate £9,000 annual limit that any adult can contribute to.

This means that grandparents, family and friends can all contribute to a Junior ISA without it affecting their own personal ISA allowance.

Find out more about Junior ISAs in our guide.

Yes. From April 2027, people aged under 65 will only be allowed to invest a maximum of £12,000 in a cash ISA in any one financial year.

The remaining £8,000 of their annual £20,000 allowance has to be invested in a stocks and shares ISA.

Those aged over 65 can still use all of their £20,000 annual allowance to invest in a cash ISA.

Maximising the amount you can invest tax-free in ISA accounts can help to make your money work harder.

It allows you to retain the proceeds of your investment tax-free.

This is particularly important as the 2025 Budget announced rises in taxation rates on dividend income from 6 April 2026 and on savings and property income from 6 April 2027.

Keeping your investments in a tax-free ISA wrapper shields them from these rises.

Every person’s financial situation is different so there may be a good reason why you might want to wait until April.

However, if you want to maximise your ISA allowance and can do so at a time of your choosing, investing as early as possible will allow you to shelter your money tax-free for longer.

It is also the case that many ISA providers are extremely busy the closer the deadline approaches so investing earlier will enable you to avoid the rush.

Taking independent financial advice can help you decide whether an ISA is right for you and what types of ISA could best suit your circumstances and attitude to risk.

To start your ISA journey, get in touch with an adviser today.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.