For investors, the perennial question of whether to ‘stick or twist’ with their current investments or pivot towards the perceived safety of cash is fundamental. Numerous factors influence this decision, which plays a pivotal role in the journey towards financial prosperity.

The appeal of cash, particularly in uncertain times, is clear; however, a judicious choice to remain invested frequently emerges as the more astute strategy.

The argument for maintaining an investment stance centres on the potential for long-term growth. Historically, investment options such as stocks have consistently outperformed inflation and delivered significant returns over prolonged periods.

The magic of compound interest, where your investments earn returns that, in turn, generate their own earnings, can dramatically increase the value of your initial stake, potentially leading to exponential growth over time.

The endeavour to time the market, shifting to cash in downturns and returning in upswings, is beset with difficulty. Even the most experienced professionals often fail to make consistently accurate timing decisions – a fact highlighted by Warren Buffett, who attributes his success to a mere dozen ‘truly good’ investment choices.

Predicting market movements can be challenging, especially in bull markets – when the prices of stocks or other assets generally rise over a sustained period of time, usually accompanied by optimism and confidence among investors. It’s like a market on the rise, where people expect good things to continue happening. Investors may sell at low points and miss subsequent recoveries or remain in cash during bull markets, thereby forfeiting potential gains. This underscores the principle that ‘time in the market, not timing the market’ is a more reliable pathway to capturing long-term growth.

Diversification is a key tenet of sound investing. By allocating resources across a variety of asset classes, sectors and themes, investors can mitigate the risks associated with specific market segments.

Staying invested allows for the upkeep of a diversified portfolio, which serves as a buffer against market volatility. Such portfolios often experience smoother performance trajectories, as positive returns from certain assets can help offset losses in others. This proves particularly beneficial during economic slumps when specific sectors might lag.

Holding cash may seem like a prudent financial safety net, offering immediate liquidity and a sense of security. However, this approach has drawbacks, as it effectively sidelines the potential for higher returns from other investment avenues.

Embracing a long-term investment strategy is key to preserving and enhancing the real value of your wealth over time, navigating past the limitations imposed by cash holdings.

The investing journey can be fraught with emotional upheaval, particularly during market volatility. By committing to a long-term investment stance, investors are better equipped to sidestep the behavioural pitfalls of fear and greed, which often precipitate rash decisions.

A robust investment strategy, centred around long-term objectives, can help instil confidence that enables investors to endure the tempests of market fluctuations with composure.

The influence of taxation on investment outcomes cannot be overstated. Liquidating assets could trigger a Capital Gains Tax payment, potentially carving a significant slice from your profits. A commitment to remain invested, deferring the realisation of these gains, offers an avenue to mitigate tax liabilities, thereby bolstering the efficiency of your investment portfolio.

The annals of financial history are replete with instances of market resilience and the inevitable cycles of downturn and recovery. Although economic setbacks, such as recessions and market crashes, are inescapable, they can potentially set the stage for subsequent periods of growth. Staying the course allows investors to partake in the recovery, harvesting the rewards of economic upturns.

In light of the compelling arguments for long-term growth prospects, the psychological steadiness afforded by a consistent investment approach, tax advantages and the historical patterns of economic recovery, the logic for remaining invested becomes incontrovertible.

While maintaining a reserve of cash for emergencies or imminent expenditures is wise, the strategy of continued investment is eminently sensible if it matches your risk profile, needs and circumstances.

We’re here to assist if you are seeking more detailed guidance or looking to deepen your investment knowledge. We’ll provide tailored advice, equipping you with the tools and insights necessary to navigate the complexities of the investment landscape. Contact us to discover how we can help you achieve your financial goals and maximise your investment potential.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS CAN GO DOWN AS WELL AS UP, AND YOU MAY GET BACK LESS THAN YOU INVESTED.

THE TAX TREATMENT IS DEPENDENT ON INDIVIDUAL CIRCUMSTANCES AND MAY BE SUBJECT TO CHANGE IN FUTURE.

A recent study has spotlighted women and investing, offering critical insights that aim to empower women to take the reins of their financial destinies and forge paths toward a prosperous future. Notably, an impressive majority of women (68%) engage in investment activities at least once a month, with over two-fifths (42%) diligently monitoring their savings and investments via online platforms or apps at least once weekly[1].

This proactive stance leads to nearly one in five (19%) women having a precise understanding of the value of their investments at any given time. However, the distribution of investment vehicles among women reveals a tendency towards traditional savings accounts (61%) and Cash ISAs (35%), with a notably smaller segment (17%) opting for Stocks & Shares ISAs, in stark contrast to 30% of men.

When it comes to selecting a savings or investment product, an equal number of women (37%) value ‘easy access to funds’ and the protection offered by the Financial Services Compensation Scheme (FSCS) above other factors. Additionally, ‘low or reasonable fees’ are paramount for nearly one in four (23%), while digital accessibility is deemed essential by almost one in five (19%).

Alarmingly, a substantial proportion of women (37%) report not investing at all, a figure that exceeds that of men (24%). The reasons cited for this abstention are diverse, with the most common being a lack of disposable income for investment purposes (45%), followed by concerns over high risk (18%), complexity (10%) and liquidity (9%). These findings underscore an urgent need for bespoke financial education and empowerment initiatives for women.

The study further reveals a commendable balanced approach to investment risk among women, with a significant majority (85%) describing their investment strategy as either medium (35%) or low (50%) risk. This cautious yet strategic approach is laudable, especially in light of evidence suggesting that female investors often outperform their male counterparts over the long term, thanks to a patient and disciplined investment style.

In an age where financial independence is a coveted goal for many, it becomes crucial to address and surmount the unique obstacles that women may encounter in the investment landscape.

The journey towards becoming an adept investor commences with the acquisition of a solid grounding in financial literacy. This foundational step involves understanding diverse investment concepts, terminologies and strategies, thereby enabling one to make well-informed decisions.

Articulating your immediate and long-term financial aspirations is paramount. These objectives not only direct your investment strategy but also keep you concentrated on your ultimate financial targets. The decision to save or invest is pivotal; while savings offer security, their value may diminish due to inflation. On the other hand, investments seek to grow your wealth, though they come with the risk of potential loss.

Before embarking on investment ventures, setting up an emergency fund is wise. This acts as a financial buffer for unexpected expenses, ensuring that you are not forced to liquidate investments during unforeseen circumstances. How much you put aside will depend on your circumstances. If you have three to six months’ worth of essential outgoings in your account to fall back on, this will give you a financial buffer if you need it.

A critical investment principle is diversification – the practice of spreading investments across various assets, funds and tax-efficient vehicles. This strategy aims to mitigate risk and foster long-term wealth growth. Interestingly, the research indicates that only 7% of women engage in diversified investing compared to 18% of men, highlighting the need for greater awareness and participation among female investors.

An informed investor keeps abreast of local and international market trends and emerging opportunities that could influence investment decisions. Regular portfolio reviews are crucial to ensure your portfolio remains aligned with your financial goals and risk tolerance. Adjustments may be necessary in response to personal financial changes or shifts in the market landscape.

Understanding your risk tolerance is essential for creating an investment portfolio that reflects your comfort level with risk, balancing it against the potential for returns. It’s important to remember that investments can fluctuate, resulting in both gains and losses.

We’re here to assist if you are seeking more detailed guidance or looking to deepen your investment knowledge. We’ll provide tailored advice, equipping you with the tools and insights necessary to navigate the complexities of the investment landscape. Contact us to discover how we can help you achieve your financial goals and maximise your investment potential.

| Match me to an adviser | Subscribe to receive updates |

Source data:[1] Research conducted by Censuswide between 10–12 January 2024 of 2,003 general consumers, aged 16+, national representative sample. Censuswide abide by and employ members of the Market Research Society which is based on the ESOMAR principles.

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS CAN GO DOWN AS WELL AS UP, AND YOU MAY GET BACK LESS THAN YOU INVESTED.

THE TAX TREATMENT IS DEPENDENT ON INDIVIDUAL CIRCUMSTANCES AND MAY BE SUBJECT TO CHANGE IN FUTURE.

With the ever-evolving landscape of investment, it’s not hard to see why it might appear daunting. The investment world is equivalent to a living, breathing entity constantly evolving and changing. It’s a landscape that never remains static, mirroring the dynamic nature of global economies and financial markets.

Market conditions are like shifting sands, unpredictable and often beyond control. They can be impacted by many factors, such as political events, economic indicators, corporate earnings reports and even natural disasters.

In addition to the ever-changing market conditions, investors are inundated with a ceaseless news stream. Breaking news, financial analysis, expert opinions and economic forecasts are examples of the information barrage investors face.

While beneficial for making informed decisions, this constant flow of information can also lead to information overload. Sifting through the noise and identifying valuable insights that can genuinely impact one’s investment strategy can be challenging.

One of the most effective ways to accumulate wealth is to start investing early. It’s not about waiting until you’ve amassed a significant sum of cash or savings; it’s about leveraging the power of compounding.

Compounding is equivalent to a snowball effect, where the money you earn through investments generates more earnings. You’re growing your initial investment and any accumulated interest, dividends and capital gains. The longer you stay invested, the more time there is for your returns to compound.

Investing regularly is as important as starting early. Doing so ensures that investing remains a priority throughout the year rather than a task confined to specific deadlines like year-end tax planning. This disciplined approach can aid in wealth accumulation over time. Regular investments also allow you to easily navigate different market conditions (rising, falling, flat), eliminating the need to time your investments perfectly.

By consistently investing a fixed amount, you can buy more when prices are low and less when they’re high, potentially reducing your long-term investment cost. Moreover, investing small amounts continuously can help balance returns over time and decrease overall portfolio volatility.

Knowing how much to save today is key to achieving your long-term financial goals. Whether you’re saving for a property, education or retirement requires careful thought and decision-making. Your current income is a valuable benchmark for calculating long-term goals like retirement savings.

The more you earn today, the more savings you’ll likely need to maintain your lifestyle post-retirement. To determine how much you need to save, ask yourself: What is your goal (e.g., retirement, travel, starting a business)? How long will it take to reach your goal? How much money will you need? What savings do you currently have in place?

The investment world offers a simple yet powerful mantra to manage risk and enhance the likelihood of success – diversify your portfolio. This strategy involves spreading your investments across various asset classes, geographical markets and industries. But what makes this approach so crucial?

Financial markets are not uniform entities; they do not move in sync. Different types of investments or asset classes, such as cash, fixed income and equities, will lead or lag at different stages in the market cycle. They may also react differently to environmental factors such as inflation, corporate earnings forecasts and interest rate changes.

Diversifying your portfolio places you in an advantageous position to seize opportunities across various investments as they emerge. This strategy usually results in a smoother investment journey. But how? The answer lies in the balancing act that diversification encourages. Investments that appreciate in value can offset those that are underperforming.

Applying these principles of successful investing can help ensure that your portfolio is poised for long-term growth, equipped to navigate temporary market volatility and ready to capitalise on opportunities as market conditions evolve.

Despite these challenges, it’s crucial not to let this deter you from embarking on your investment journey. While investing may seem daunting at first glance, it’s a journey that can lead to substantial financial growth and security when undertaken with due diligence and strategic planning. If you require further information or want to discuss your investment journey, we’re here to help you navigate the complex investing world and achieve your financial and life goals.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH.

TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Gain a comprehensive overview of the market’s unexpected twists and turns, followed by a look into what to anticipate in the coming year.

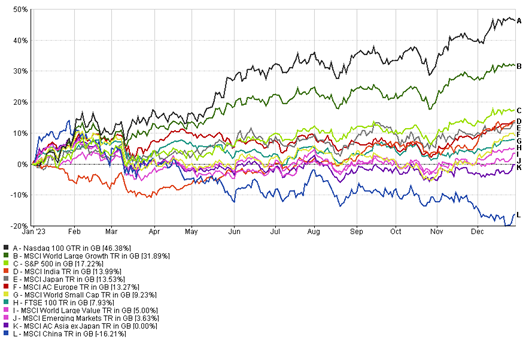

Many readers will remember that coming into 2023, it was consensus from economists that we would see some, if not all, of the developed world enter a recession. A poll by the FT showed that in December of 2022, 80% of economists polled thought that we would be in a recession by the end of 2023, while some thought we were already in one at the time. We can now safely say that those predictions were wrong. Instead, throughout 2023, we saw unemployment stay low, consumer spending remain resilient and revisions for full year GDP, particularly in the US, revised consistently upwards.

So, the recession never came and economic data across the developed world was better than expected. This therefore sets up for a good backdrop for equities – and it turns out, despite not feeling like it for much of the year, that 2023 was a good year for most risk assets. Below, we are showing returns, in sterling, for some major indexes across the full year. We have the Nasdaq that gained 46%, driven by excitement around Artificial Intelligence (AI) and the hope that we will soon be seeing lower rates in the US as inflation came under control. Followed by the, also tech heavy, World Growth index at 32%, then the broader S&P with a gain of 17%, India, Japan and Europe around 13%, global smaller companies at 9%, the FTSE 100 at a lower, but respectable, 8%, and then emerging markets up 4%. Asia finished flat and then the major outlier of Chinese equities, down 16%.

2023 has just shown how difficult it is to predict markets and economies, particularly as we still unwind issues from the pandemic and the considerable stimulus that came with it. We simply just don’t have precedent for an environment like this and how it may affect asset classes. So, despite many major events happening, accompanied by lots of very negative headlines, equities actually performed pretty well. The key therefore is to remain invested, stick to long-term planning, and allow the power of compounding to work in your favour.

As previously mentioned, a lot of the gains in markets this year have been driven by the rise of Chat-GPT, and what that could mean for wider use of AI advancements and who the winners of that story would be. Thus far, the main winners have been named as the “Magnificent 7”, which as a group consists of Apple, Microsoft, Alphabet (Google), Nvidia, Amazon, Meta (Facebook) and Tesla. These 7 stocks are now the 7 largest in the global equity index, accounting for 30% of the US index, and as a group gained around 106% (in USD) in 2023.

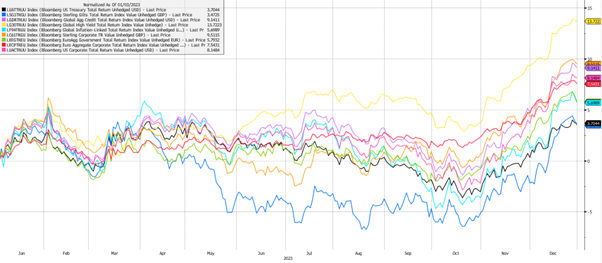

Turning to fixed income, much like equities, bonds battled through a difficult and volatile year, but ended in positive territory across all major indexes that we are showing below. The best performing index here is high yield bonds, gaining 13.7%, which came as a surprise to most investors, as this was an asset class many expected to be weak this year. This is a similar story for the equities, given the poor sentiment in this asset class coming into the year, economic resilience has really boosted returns of those invested. We have seen defaults rising through the year, but remaining low in context of history. However, despite this strong run, investors do remain somewhat cautious of high yield bonds due to spreads being very narrow compared to history and the difficulty it will likely face if the economy does begin to roll over.

We then have sterling credit, gaining 9.5%, global corporates up 9.1%, US corporates up 8.1% and European corporates up 7.5%. Again, benefitting from attractive starting yields and boosts from economic resilience.

The laggards are sterling Gilts, which rallied very strongly from November to end positive, having spent most of the year in negative territory, and up 3.4%. Around the same level of returns from US treasuries and slightly behind the global index-linked market.

As we look out to 2024, we enter with cautious optimism across equity and bond markets. The key question remains whether we have pulled forward a lot of the good news from 2024 into 2023, and whether we may still get the economic impact of the rate rises felt across the economy. Or whether we will truly enter a new growth cycle and the market has every right to be optimistic.

All eyes will continue to be focussed on inflation, unemployment and GDP growth, as a guide as to where central bank interest rates may be headed. Current consensus is that inflation will continue to move lower through this year, in a fairly stable manner, with the US and Europe ending the year close to the 2% target, and the UK still a little higher. Investors therefore hope that this will allow central banks to declare victory on their battle with inflation, and lower rates to a less restrictive level. Markets are currently pricing in around six 0.25% cuts in the US across 2024, which is double the guidelines provided by the Fed. The market is also expecting these cuts to happen in the first half of the year, maybe even in March, whereas the Fed has suggested they would come closer to the end of the year.

However, it remains key to understand what the cause of these cuts could be, as markets will react very differently based on whether the cuts are coming from a strong economic backdrop while inflation remains low, or whether we will need to cut rates to support a weaker economy. Many strategists are also making the point of why we would even want rate cuts if the economic data is still strong with low inflation, and that central banks might leave that option in their back pocket for any future issues that will inevitably crop up.

Entering 2024, we have valuations of equities looking fairly cheap in many regions, particularly the UK and Emerging Markets, which trade at a discount to the rest of the developed world and when compared against their long-term averages. We also have bonds providing very attractive yields, even at the lower risk end of the market, which should provide a good level of support for balanced portfolios. This provides investors with a relatively positive backdrop, alongside tailwinds such as AI, the green transition and potentially lower interest rates. We therefore continue to strongly believe that it is key for investors to remain diversified, and that while there are reasons to be more cheerful, there are still significant risks at play. Particularly given the fact we have both UK and US general elections likely to happen in the final quarter of the year.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

Like health, the more meticulously you manage your wealth, the longer it lasts. A growth strategy seeks to amplify your wealth over the long haul, opening up a world of possibilities for you. Whether you dream of a large retirement fund, a holiday home or providing top-tier education for your children or grandchildren, a growth portfolio could be your ticket.

Choosing a growth investment strategy hinges on factors such as age, investment timeframe, risk tolerance and life goals. Given its long-term nature, growth investing tends to be a good fit for younger investors – those in their 20s, 30s, or 40s – eager to optimise their investments by targeting the higher returns that growth portfolios aim to deliver.

Contrary to popular belief, a growth strategy is for more than just the young. It can also be a compelling route for seasoned investors who view their capital as a legacy to be nurtured for future generations. Growth portfolios lean towards asset classes like equities and multi-asset funds, which offer the best potential for yielding higher, long-term capital returns.

Growth investors strive for increased exposure to sectors and regions projected to experience above-average long-term growth within these asset classes and funds. This is based on meticulous analysis and stringent investment criteria and may involve carefully managed investments in emerging markets or tech stocks.

Everyone has a different risk appetite and tolerance for losses when investing. Some investors are highly risk-averse, sticking to savings accounts, while others might be drawn to higher-risk investments like stocks and shares.

Staying invested for the long haul, rather than attempting to trade and time the market actively, is one of the most effective ways to mitigate risk. The age-old wisdom of diversifying your investments – essentially, not putting all your eggs in one basket – rings true here. Betting all your funds on one particular stock or sector is more akin to gambling than investing.

Growth investment strategies also capitalise on the power of compounding by reinvesting capital and dividends. You may have reached a stage where you want to convert your assets into regular payments that support a comfortable lifestyle or afford life’s luxuries. This tends to be especially crucial for those planning retirement, funding care costs, supplementing their primary income or financing education.

There’s no universal answer, as the level of income you need is as unique as you are. It depends on your lifestyle, age, health and goals. Your regular expenses can range from bills and food to significant expenditures like mortgage payments and maintenance costs. And that’s before considering discretionary spending on holidays, hobbies or education.

Striking the perfect balance involves drawing sufficient income from your investment without undermining its value. Our role is to guide you in achieving this equilibrium through a diversified investment strategy crafted uniquely for you.

Dividend and interest payments alone may not meet your cash flow needs. Hence, our attention is concentrated on achieving an ideal income level, all while ensuring that the risk involved aligns with your comfort zone.

Another critical aspect to consider is making provisions for inflation within your strategy. The goal is to develop a strategy to preserve the real-term value of income derived from your portfolio. We’ll help you explore options and structure your portfolio to cater to your needs.

Withdrawing large amounts from your savings and investments portfolio will inevitably reduce your base capital. Your remaining funds must then work harder and could run out sooner than anticipated. Inflation will also significantly threaten long-term savings, making incorporating this factor into your strategy essential.

After thoroughly understanding your specific needs, including your preferred investment timeline, risk tolerance and ability to withstand potential losses, we will design a custom investment portfolio that aligns with these goals. To find out more or to discuss your requirements, get in touch.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Embarking on the journey of investing can seem intimidating initially, but with a long-term perspective, it can significantly accelerate the achievement of your financial goals.

It’s normal to feel a mix of excitement and apprehension as a first-time investor. There’s a lot to navigate – stocks, bonds, mutual funds, market trends and a sea of unfamiliar jargon. Remember, every successful investor started right where you are now.

The stock market is known for its fluctuations, with dips and rises being part and parcel of the game. However, history evidences that shares often outperform cash over extended periods and stay ahead of inflation.

Here are five essential tips to help you take the first step and beyond.

The first step of your investment journey involves setting concrete goals. A relatively long-term target helps your investments weather market volatility. Your goal could be anything from saving for retirement to securing your children’s future.

During temporary market downturns, keeping your eyes on the prize reduces the likelihood of selling out and incurring losses.

Contrary to popular belief, you don’t need a mountain of money to begin investing. Regularly investing manageable amounts each month or gradually investing a lump sum can prove beneficial, especially during times of economic uncertainty and stock market turmoil.

Your money purchases more shares when the market is down and fewer when it’s up. This strategy averages out your investment cost and may contribute to smoother portfolio performance over time.

Remember your Individual Savings Account (ISA) allowance, which resets annually on 6 April. For the current 2023/24 tax year, this is £20,000. An ISA allows your investments to grow tax-efficiently, enabling more of your money to contribute towards your future.

Allowing emotions to guide your investment decisions is not a wise strategy. It’s natural to feel nervous when the stock market dips, especially for novice investors. However, maintaining your composure and staying in the market once you’ve entered can be crucial.

A well-rounded investment portfolio will typically include a mix of equities, bonds and cash. Diversification is beneficial, as different assets react differently under varying market conditions. This can help balance returns and lessen the impact of a specific asset’s value decline.

For beginners, diversification can be a challenging task. That’s where expert professional financial advice is crucial. We can help you distribute your money across various investments tailored to your unique needs and risk tolerance. We can also ensure you’re making the most of your tax allowances and reliefs, giving you confidence that your money is working as hard as it should.

Ready to embark on your journey to financial growth? Get in touch today.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH.

THE VALUE OF YOUR INVESTMENTS CAN GO DOWN AS WELL AS UP AND YOU MAY GET BACK LESS THAN YOU INVESTED.

THE TAX TREATMENT IS DEPENDENT ON INDIVIDUAL CIRCUMSTANCES AND MAY BE SUBJECT TO CHANGE IN FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

With UK inflation the highest in the G7 and more than two percentage points higher than the US, our expert Adviser Tim Ross discusses why it could be time to diversify your portfolio as the value of cash diminishes.

The mantra ‘Cash is king’ has echoed through the investment world for years. Cash forms the backbone of our society – it pays for our purchases, settles our debts and serves as a liquid asset in tough times.

As long as money spins the globe, many will uphold cash as the reigning monarch. However, this crown has been slipping off lately. This raises a question – is it wise to lock into a rate that incurs losses in real terms merely to avoid the short-term volatility of financial markets?

The circumstances for each saver are unique. But the argument for holding cash over investments, especially over the longer term, simply because savings rates are on the rise, is flawed. In the face of still high inflation, the value of cash diminishes, while investments can potentially offer higher returns. Therefore, evaluating whether holding on to cash is the best strategy, especially in the long run, is essential.

With inflation showing only muted signs of letting up, the real worth of your wealth held in cash may continue to be chipped away. The dilemma then lies in figuring out what proportion of cash should remain in the bank, exposed to inflation, and what portion should be invested.

Deciding on the amount of cash to retain in the bank and the amount to invest with the aim of outpacing inflation is a complex and highly individual decision. What works for one person might be entirely unsuitable for another, hence the importance of receiving professional advice.

If you depend on employment income to cover living expenses, it may be prudent to maintain a larger cash buffer in case of job loss. Conversely, those with a guaranteed income, such as a final salary pension, might benefit from investing more and banking less. Your living costs also play a role. Those with higher expenses might prefer to have more saved on deposit for emergencies, especially given the rising cost of living.

Your life stage may also influence your decision. For example, individuals with dependents and a mortgage might prefer to have more banked on deposit for unexpected events than those with fewer responsibilities. Any planned capital expenditure in the next three years (like property purchases or gifting adult children) should be reserved in cash.

Regardless of wealth level, some people may find comfort in having a sum of cash in the bank. But it’s worth considering whether keeping excess money in the bank, thus subjecting it to inflation, can be a higher-risk strategy than investing in a diversified portfolio. This is because when inflation outstrips interest rates, the value of cash diminishes, while the value of an investment portfolio has the potential to increase over time.

There’s no one-size-fits-all answer to the question of how much money is too much to keep in the bank. The appropriate amount varies greatly depending on numerous factors. To discuss your options or to find out more, please get in touch with us.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Considering gilts as part of a balanced investment portfolio, especially in uncertain financial times, can be an attractive option to investors says Ryan McLaren, one of our expert advisers.

High interest rates make gilts an attractive option for some investors, especially higher rate taxpayers who benefit from the tax exemption from capital gains. What exactly are gilts? These UK government bonds, or debt securities, are issued to finance public expenditure. Their appeal lies in their low-risk nature and guaranteed income.

Gilts are considered one of the safest investment options because the British government fully backs them. Think of a gilt as an IOU from the Treasury. Investors receive regular interest payments in return for lending money to the UK government. Most gilts offer a fixed cash payment (or a coupon) every six months until maturity, when the final coupon payment is made along with the return on the original investment.

Investors have two options: hold on to the gilts until maturity or sell them on the secondary market, much like company shares. Short-term gilts mature between one to five years, medium-term gilts have a lifespan of five to fifteen years, while long-term gilts exceed fifteen years, some even extending up to fifty years. Generally, gilts with longer lifespans have higher interest rates than those maturing soon.

The annual return an investor gets for holding a gilt over the next 12 months is known as the yield. It’s calculated by dividing the annual coupon payments by the current market price. Various factors influence gilt yields, including the outlook for interest rates, inflation and market demand for gilts. Interestingly, bond prices and yields move in opposite directions.

Since the pandemic, interest rates have skyrocketed as the Bank of England tries to control inflation. Interest rate changes significantly impact bond prices, especially when they are forecasted to keep increasing. As interest rates increase, bond prices generally fall, and vice versa. This inverse relationship is due to new bonds with high coupon rates being issued at higher interest rates than older bonds that have been issued at lower rates.

While Income Tax applies to the interest earned from gilts, they are entirely exempt from Capital Gains Tax (CGT). This means there’s no CGT to pay on any profits from selling a gilt or when it matures. This exemption is especially beneficial for higher rate taxpayers who’d otherwise have to pay a 20% CGT. Moreover, there’s no tax on gilts held in a tax-efficient wrapper like an Individual Savings Account (ISA) or a Self-Invested Personal Pension (SIPP).

For investors concerned about inflation, inflation-linked gilts offer a reliable way to protect their capital if held to maturity. The principal and interest are tied to inflation, ensuring investors receive a return that keeps pace with the cost of living.

Gilts provide a safer alternative during uncertain times, and their low correlation with stock markets makes them an alternative diversifier. By including gilts in a diversified portfolio, investors can mitigate risk and balance their exposure to different asset classes as the coupon is fixed at the outset.

Don’t hesitate to get in touch for further information or advice on adding gilts to your portfolio. We’re here to help you make informed investment decisions. To find out more, contact us – we look forward to hearing from you.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Fiona Ruck, one of Fairstone’s expert financial advisers, discusses the merits and considerations of investment bonds in light of recent tax regulation changes.

Investment bonds offer several benefits that some investors may be missing out on, and have become even more beneficial due to recent changes in tax regulations following the Chancellor’s decision to reduce the Capital Gains Tax (CGT) Allowance from £12,000 to £6,000 this year and to £3,000 in April 2024.

These changes will likely appeal to investors who want to minimise Inheritance Tax (IHT) liabilities when passing on wealth. The IHT nil-rate threshold has remained at £325,000 since 6 April 2009, with no indications of future increases. As a result, more individuals are considering trusts to keep their money outside their estates.

Investors who have already utilised their ISA allowances and other tax-efficient wrappers, or those who have received substantial windfall payments, such as inheritances, could benefit from using investment bonds. Investment bonds primarily fall into two categories: onshore and offshore. The key difference is their tax treatment, which can significantly impact returns.

Onshore bonds are subject to UK Corporation Tax. However, this tax is offset by your provider, which means you, as an investor, do not have to worry about it directly. While this may seem like an advantage, it’s important to note that the tax could lower your return compared to an offshore bond.

On the other hand, offshore bonds are issued from outside the UK. The returns from these bonds roll up gross of tax in the funds, with the exception of Withholding Tax. This can potentially offer higher returns compared to onshore bonds, depending on your personal tax situation.

Despite these advantages, the research reveals that only a minority of investors fully understand investment bonds. However, there is potential interest among certain demographics. For example, 18% (9 million) of non-bond investors would consider investing in bonds. This interest is particularly prevalent among mass affluent consumers, those with children aged between 0 to 10, and individuals with a household income of £100,000 and above.

It is worth noting that only 10% of UK adults claim to have a clear understanding of the tax rules regarding bonds. This lack of knowledge could hinder investors from fully capitalising on the benefits offered.

One of the key advantages of investment bonds is that they are not subject to CGT. Onshore bonds are treated as having already paid 20% tax on any gains when calculating a chargeable gain. In reality, the actual tax deducted is likely to be less than this amount.

In addition, investment bonds can be beneficial for IHT planning. If held in a trust, they can be exempt from IHT after seven years. However, despite this potential advantage, only a quarter of bondholders have written their bonds in trust, which means the bonds would still be considered part of their estate for IHT purposes.

Investors can withdraw up to 5% of their initial investment each year without triggering a chargeable event or incurring immediate tax liability.

Furthermore, top-slicing relief is available to reduce tax liability when a chargeable event occurs. This relief can eliminate or significantly reduce any tax liability, which can be advantageous for individuals in the accumulation phase and those preparing for retirement. For example, someone may be a higher rate taxpayer while owning the bond but can become a basic rate taxpayer when encashing it.

Investment bonds also offer options for assigning them between spouses. From a tax perspective, the assignment is generally treated as if the new owner had always owned the bond. This can be particularly beneficial if one spouse is a basic rate taxpayer, as they may have no tax to pay upon encashment.

Overall, investment bonds present numerous advantages, including tax benefits, that investors should consider. However, it is crucial for individuals to fully understand these benefits and the tax rules associated with bonds in order to make informed investment decisions.

If you’re interested in taking advantage of investment bonds but need the security of expert tax advice on these products, get in touch. Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Source Data: [1] LV= research – Don’t forget the benefit of bonds – published 23 May 2023.

THE VALUE OF YOUR INVESTMENTS CAN GO DOWN AS WELL AS UP, AND YOU MAY GET BACK LESS THAN YOU INVESTED.

THE TAX TREATMENT IS DEPENDENT ON INDIVIDUAL CIRCUMSTANCES AND MAY BE SUBJECT TO CHANGE IN FUTURE.

ESTATE PLANNING IS NOT REGULATED BY THE FINANCIAL CONDUCT AUTHORITY.

If you’re looking to ensure that your investments give you peace of mind while trying to reduce societal imbalances and promote positive environmental practices, Fairstone Portfolio Manager, Imogen Hambly, shares some tips on what you need to consider before selecting your portfolio of investments.

Environmental, Social and Governance (ESG) investing is a strategy that focuses on companies that prioritise environmental, social and governance factors in their operations. Investing in these businesses aims to support responsible practices and contribute to a sustainable future.

By focusing on companies that pay heed to these factors, investors can support sustainable businesses while enjoying the potential for superior long term financial performance.

Environmental: This criterion evaluates a company’s impact on the environment. Factors such as energy use, sustainability policies, carbon emissions and resource conservation are considered when assessing a company’s environmental performance. Companies with strong environmental practices often have lower associated environmental risks and demonstrate a commitment to reducing their ecological footprint.

Social: The social aspect of ESG investing examines how a company treats its employees and interacts with the communities in which it operates. Businesses prioritising employee welfare, workplace safety and community engagement are more likely to have a positive social impact and maintain a good reputation. Supporting companies with strong social values can promote fair labour practices and foster a more inclusive society.

Governance: Governance factors relate to a company’s leadership, management and overall corporate structure. Key considerations include executive compensation, audit processes, internal controls, board independence, shareholder rights and transparency. Companies with robust governance structures are more likely to be accountable, trustworthy and better prepared to manage potential risks.

By considering ESG factors in investment decisions, investors can support companies that demonstrate a commitment to long term sustainable growth, stakeholder alignment and strong governance. This approach allows investments to reflect positive values and can lead to long-term financial benefits, as ESG-focused companies are often better equipped to navigate evolving regulations, mitigate risks and capitalise on emerging opportunities.

ESG factors are increasingly essential for investors when evaluating companies and making investment decisions. Investing in good-scoring ESG companies can allow for responsible investments without sacrificing returns. Numerous studies have shown that companies with strong ESG performance tend to outperform their counterparts with lower ESG standards.

As noted above, good ESG scores indicate that a company is focused on long term sustainable growth, stakeholder alignment and strong governance, which in combination can lead to long-term success and reduced risk exposure. These companies are more likely to show resilience through periods of market volatility.

On the other hand, businesses associated with low ESG standards are more likely be engaging in activities that cause significant environmental harm or are participating in unethical practices. These events not only lead to real-world negative outcomes, but they increase the risk of companies being subject to regulatory penalties, reputational damage and declining share prices.

ESG investing has gained significant traction recently as investors increasingly seek to align their portfolios with positive values. However, the varying interpretations of what makes an ESG leader and the rise of ‘greenwashing’ can make it challenging for investors trying to navigate this space.

One of the main challenges of ESG investing is the subjectivity in evaluating companies based on their environmental, social and governance policies. What is considered a responsible investment for one person could be viewed as unethical by another. For instance, a sugary drinks manufacturer may have an excellent recycling policy, earning them high marks in the ‘E’ category. However, some investors might argue that sugary drinks are detrimental to society, making the company an unsuitable investment choice.

This subjectivity makes it difficult for investors to find a universally agreed-upon standard for determining whether a company or fund can truly be deemed responsible.

Another challenge facing ESG investors is the phenomenon of ‘greenwashing,’ where companies or funds market themselves as environmentally friendly or socially responsible when, in reality, they do not meet these standards. This deceptive practice can lead to investors unwittingly supporting businesses that do not align with their values.

Despite the challenges posed by subjectivity and greenwashing, the incorporation of ESG factors into investment decisions remains an essential tool for those who wish to align their financial goals with positive outcomes and/ or personal ethical values.

By taking these steps, investors can better ensure that their investment choices align with their personal values and contribute to a more sustainable and socially responsible future.

| Match me to an adviser | Subscribe to receive updates |

THE TAX TREATMENT IS DEPENDENT ON INDIVIDUAL CIRCUMSTANCES AND MAY BE SUBJECT TO CHANGE IN FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.