In a recent move that has heightened global trade tensions, the US administration announced a series of sweeping reciprocal tariffs. In response, China has introduced a 34% blanket tariff on all US imports starting April 10, alongside export restrictions on critical rare earth materials and sanctions targeting key US defence and technology firms.

The purpose of this blog is to help you navigate the recent surge in global trade tensions and understand the long-term impact of these events on your financial strategy. These trade moves could have a ripple effect on markets, impacting everything from stock prices to supply chains, but the key to weathering this uncertainty lies in staying focused on your long-term goals. Remember, the secret to long-term success in investing isn’t about trying to time the market, it’s about time in the market. Despite the noise, sticking to a consistent strategy is what will ultimately drive your success.

Markets can, and do, experience periods of downturns. These moments may feel unsettling, but they’re typically short-lived. The most effective approach is to stay committed to your investment strategy, even when markets are turbulent.

History has consistently shown that drawdowns are entirely normal in any given year, and that markets recover and often bounce back just as sharply as they fall. Trying to time the market by selling in a panic or holding off on new investments until things “settle down” can significantly impact your long-term financial returns.

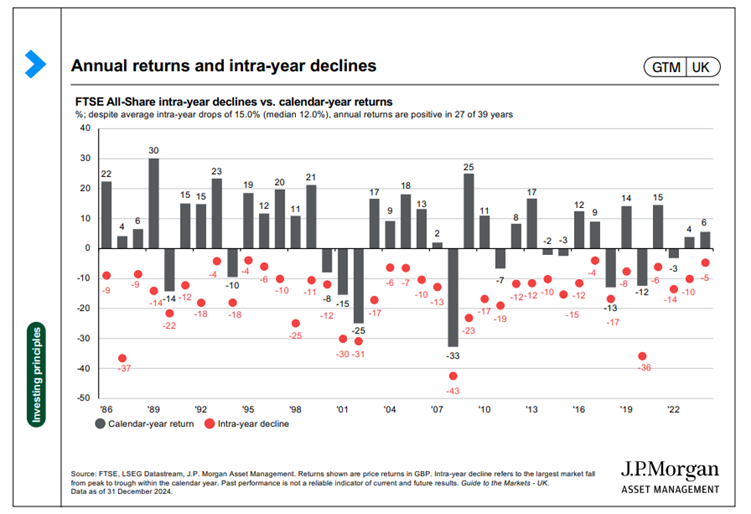

In the chart below looking at the UK FTSE All-Share index over a near-40 year period, the red dots represent the maximum intra-year equity decline in every calendar year, or the difference between the highest and lowest point reached by the market in those 12 months, while the grey bars represent the full year’s return. While market pullbacks are a normal part of investing, history shows that in most years, markets still finish in positive territory. Double-digit declines may occur, but they’re often followed by strong recoveries. Rather than trying to predict short-term dips, investors should stay focused on long-term goals.

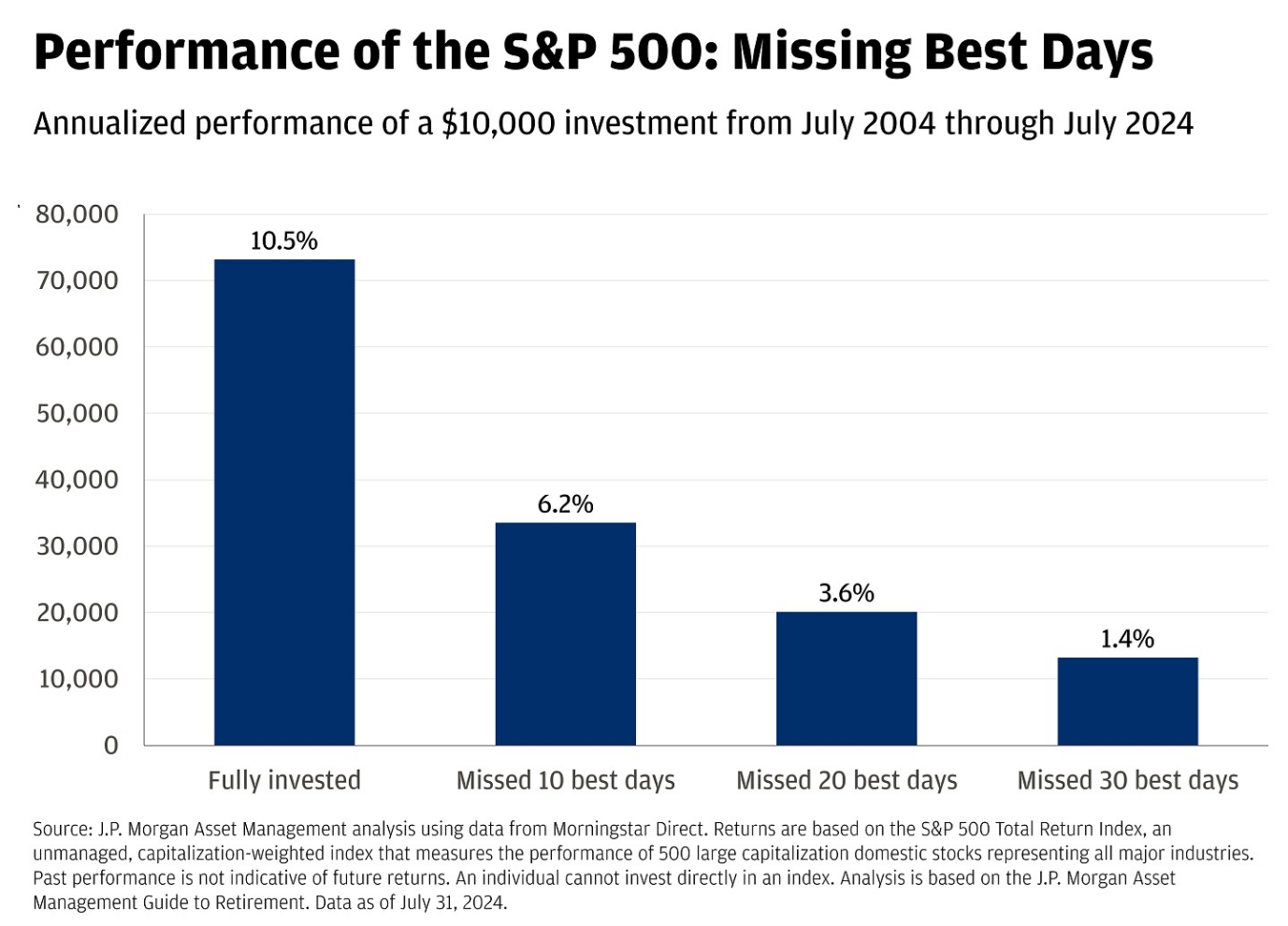

An analysis of stock market returns over a 20-year time period shows the power of remaining invested and not trying to time the market. Using data from the US S&P 500 market, the chart below shows the enormous cost of missing just a handful of the best trading days over the period, which encompasses the global financial crisis, Covid and numerous other notable market events.

Whilst the chart below illustrates values in US dollars, the same principles apply to pounds sterling. If you were to invest £10,000 in the S&P 500 in 2004 and stay fully invested through to the middle of 2024, you would have over £70,000. However, if you missed just the 10 best trading sessions, you would be left with under £35,000. The reason? Market timing is incredibly difficult. Over the last 20 years, seven of the 10 best days occurred within 15 days of the 10 worst days.

One of the smartest strategies for managing risk is diversification. Spreading your investments across various asset classes, sectors, and global markets. A well-diversified portfolio acts as a cushion during volatile periods, with strong-performing assets often helping to offset areas of your portfolio that are not delivering as strong rewards.

This balanced approach allows investors to ride out market fluctuations while still being positioned for long-term growth.

The evidence is clear: staying invested through the ups and downs of the market leads to stronger outcomes over time. Long-term investing rewards patience, discipline, and consistency. It also allows you to take advantage of powerful benefits such as compounding, tax efficiencies, and the natural rebound of economies.

It’s perfectly reasonable to keep some cash on hand for short-term needs. But for your longer-term goals, whether it’s retirement, buying a home, or leaving a legacy, the best approach is to remain invested in a strategy that aligns with your personal risk profile and objectives.

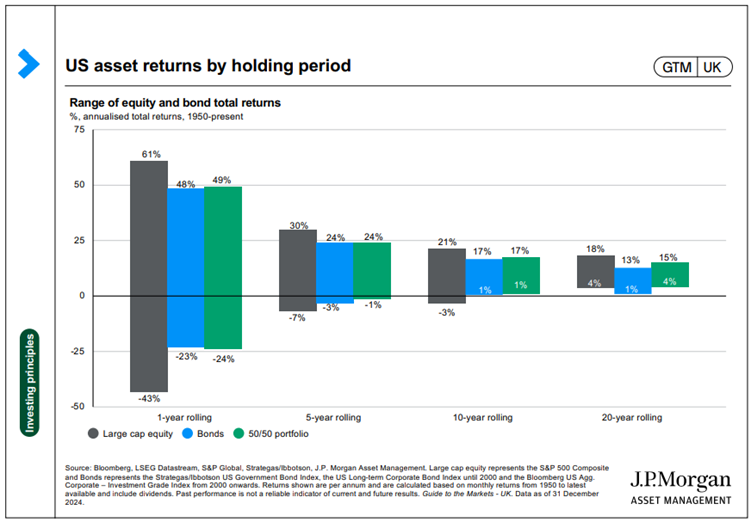

As this final chart shows, using representative data from US markets that read across directly to UK investors, while markets can always have a bad day, week, month or even a bad year, history suggests investors are much less likely to suffer losses over longer periods. It’s important to keep a long-term perspective. Investors should not necessarily expect the same rates of return in the future as we have seen in the past, but a diversified blend of stocks and bonds has not suffered a negative return over any 10-year rolling period historically, despite the great swings in annual returns we have seen since 1950:

Attempting to predict market movements often leads to missed opportunities. Staying consistently invested allows you to benefit from long-term growth and recovery periods.

Market downturns are inevitable, but history shows they are usually short-lived. Maintaining your investment strategy during turbulent times is more effective than reacting emotionally.

Even missing a few top-performing days can drastically reduce long-term returns. A disciplined, stay-the-course approach typically outperforms panic selling.

A well-diversified portfolio across asset classes, sectors, and regions—mitigates risk and provides stability during market swings.

Sticking with your investment plan through economic cycles harnesses the power of compounding and positions you for greater financial security over time.

If you’re looking to revisit your financial plan or explore new investment opportunities, we’re here to guide you. Our team can offer personalised advice and insights tailored to your unique circumstances, helping you navigate uncertainty with confidence.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Fairstone independent financial adviser Adam J Walker asks what is income protection insurance?

I never want to be the one who takes that call from a surviving partner and has to explain why there is no cover in place or why it was not considered or reviewed.

Although few wish to pay for it and no one wants to claim, it is super important to have at least some protection in place, not necessarily to protect you but to protect those who you love.

As part of our holistic review service, we want to ensure clients and their family are properly and suitably protected so they have every chance of meeting their long-term goals (the end desired outcome) and objectives (the steps to get there). A big part of this is the importance of protecting what you already have worked so hard to build.

Would your family be able to cope financially with the impact an unexpected event might have? These are not easy questions to ask but it is important to consider what would happen if an unexpected event or accident took place, and how you could protect your family from the financial effects of serious illness or death with protection insurance.

Deciding what your priorities are and understanding what options you have are key parts of the protection planning process. This helps you ensure that you have the financial protection most suitable for your circumstances.

Every family is different, but they often play a big part in our lives. It’s important to think about how we can protect them against the unexpected as best we can.

Death is an unpredictable event, so it’s important to make sure you have the right level of cover in place. The amount of life insurance you need will depend on your individual circumstances. There are many good reasons to take out a policy. For example, if you have dependents who rely on your income, then life insurance can provide financial security for them if you die.

There are different types of life insurance available, so choosing the right policy for your needs is key. Term life insurance provides cover for a set period of time, while whole of life insurance covers you for your entire life. You can also choose between level term insurance, which pays out a fixed amount if you die during the term of the policy, and decreasing term insurance, which pays out less as the policy progresses.

There is also a variation on the basic term assurance theme that is often worth considering as it can reduce the cost of cover. Family Income Benefit is a policy with a sum assured that reduces uniformly over time but provides regular payments of capital on the death of the breadwinner (the life assured).

If you have any debt, such as a mortgage, then it’s also important to review your life insurance needs and make sure that this area is covered so not to leave your loved ones burdened with debt. Without your income, the repayment may quickly become unaffordable and result in the family home needing to be sold.

There are a number of reasons why income protection insurance should be a part of your protection planning. Firstly, it can help to protect your income if you are unable to work. This could be due to illness, injury or any other reason that means you are unable to work. It can help to cover the costs of your everyday living, such as your mortgage or rent, bills and food.

If you do not have sufficient protection in place this may mean you have to rely on your savings, or on the help of family and friends. Income protection insurance is especially important if you are self-employed or have a family to support. If you are unable to work, your income protection policy will provide you with a replacement income so that you can continue to meet your financial obligations.

There are different types of income protection insurance policies available, so you should obtain professional financial advice to ensure you can compare the different options and fully understand the terms and conditions of the policy.

If you become seriously ill and are diagnosed with one of a list of specified conditions even if you are still able to work, critical illness cover could provide you with a financial safety net. It can help to pay for treatment, to make adaptations to your home or lifestyle, provide an income for your family if you are unable to work or other costs associated with your illness. In some cases, it may even pay out a lump sum if you die as a result of your condition.

There is no guarantee that you will not experience a critical illness during your lifetime, so it is important to have this type of cover in place. It will give you the peace of mind of knowing that you and your family are financially protected if the worst were to happen. Critical illness cover is not a substitute for health insurance.

Do your children, partner or other relatives depend on your income? Many families would have to cut their living costs in order to survive financially in the event of the main breadwinner falling ill or dying prematurely. If you are unclear on your protection requirements, we are here to explain your options.

| Match me to an adviser | Subscribe to receive updates |

Whilst you can make a DIY will, it is best to use a professional will drafter such as a solicitor to ensure that it is drafted correctly as the consequences of getting this wrong can be expensive.

Firstly, decide who you wish to appoint as executors to handle your estate on death. If you have children under 18 years, decide who you also want as their guardians. Then itemise any specific requests that you wish to make, noting down what they are, amount of money or percentage if applicable and the names and addresses of those that you wish to benefit. This can also include a charity.

Then decide who you wish to benefit from your remaining estate such as your loved ones, family or friends. Consider what you would like to happen if any of your beneficiaries were to die before you and who you would like to benefit in their absence.

You can work out the value of your estate by noting down and totting up the value of your money, investments, life assurance not in trust, property and possessions. Then deduct any liabilities you have such as mortgages, credit cards and car loans etc. This will give you the net value of your estate.

Most wills are straight forward and inexpensive to set up in comparison to the costs and consequences of not having one.

Most people appoint their respective spouse or partner, however it is important to consider that they could predecease you and therefore appointing an extra executor would be beneficial.

The Government will step in and decide who will benefit from your estate through the laws of intestacy. This may mean that people could benefit that you may not have wished to.

The law of intestacy doesn’t recognise partnerships; this would mean your partner would not be able to benefit from your estate under these rules.

It’s even more important that you have a will in place if you have children under the age of 18. Through a will, you can appoint legal guardians to look after and be responsible for your children until they become adults.

There is no set time period, however a good way to update your will is to do this at any major life event or anytime you wish to change how and who you want to benefit from your estate.

It is best to store your will with a solicitor. However, if you are planning on keeping it at home, it is best to store this in a fire-proof safe and register it with the National Will Register.

You will need to consider who you wish to appoint as your attorneys. This can be anyone over the age of 18 years such as relatives, friends, husband or wife. You can also appoint a professional such as a solicitor. When appointing attorneys, you should give consideration as to how well they look after their own affairs and if you would trust them to make decisions in your best interests.

It is good practice to appoint at least two people and to give some thought as to whether you wish for them make decisions separately or together.

You can apply and register for an LPA via the www.gov.uk/power-of-attorney/make-lasting-power .

Please note LPA’s are only applicable in England and Wales. You can find out more about making an enduring power of attorney in N.Ireland or power of attorney in Scotland via the following websites:

At Fairstone we have a wide range of advisers across the country who are able to assist you in making or updating a will, setting up a lasting power of attorney agreement or answering any other questions you may have. Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Wills and LPAs are not regulated by the FCA. The details relating to the laws of England & Wales are correct at the time of publication, and legislation may change. Fairstone Group Limited and associated companies are not legal advisers therefore specialist legal advice may be required before establishing wills and LPAs under any jurisdiction applicable to place of residence.

According to recent research carried out by Unbiased.co.uk, over 60% of UK adults don’t have a Will. Out of those 60%, a fifth of people don’t believe that they have enough assets to make it worthwhile.

The number of people without a Will is now at an all-time high and while it is hard to pinpoint an accurate reason for this, there are two common misconceptions.

Firstly, a lot of people think that they don’t have enough assets to make a Will and that family and friends will be able to decide amongst themselves as to who gets what in the event of a person dying. Secondly, people wrongly assume Wills are complicated, time consuming and expensive.

The best way to help ensure your property, possessions and savings go to the people and causes you care about after you die, is to arrange a properly drafted Will, as it will allow you to decide how your assets are distributed upon death. You can leave your entire estate to one or many people, or to a charity.

Making a Will is even more important if you have young children as it allows you the opportunity to make legal arrangements for the care of any children you have under the age of 18.

If you die without a Will in place, you will have no control over who will inherit your estate. Instead the Government will decide who inherits this through the rules of intestacy and this may include people you may not have considered benefiting from your estate.

The intestacy rules are outdated with modern family life. For example, if you live with your partner but are not married or are in a civil partnership, the intestacy rules will not recognise that person and they will not be entitled to benefit from your estate on death.

In addition to setting up a Will, it is also of equal importance to set up a Lasting Power of Attorney (LPA). An LPA is a legal document that grants another person authority to make decisions on your behalf if you are no longer able to make these decisions yourself.

Many people think that if they could no longer look after their own affairs, someone would automatically be able to step in and take control. But this isn’t the case, and sadly too many families don’t realise this until it’s too late.

This would mean that if you were unable to access your bank account, for example to pay utility bills or to purchase food, no one else could access this for you. Also, if you needed medical treatment and a decision had to be made about what treatment to undertake, no one would be able to make an informed decision for you. Your family would therefore need to apply to the court for a Deputyship order which can be expensive and time consuming.

There are two types of LPAs. A Health and Welfare LPA allows you to name people who you would like to make decisions about your health care, medical treatments and living arrangements and a Property and Affairs LPA allows you to name people to deal with money or property that you own within England or Wales. You can state the circumstances in which you would want the LPA to come into effect.

Setting up a Will and LPA are inexpensive in comparison to the consequences of not having them. It is important to use a reputable and qualified practitioner as a badly drafted Will can have unintended consequences that may lead to difficulties for your loved ones after you pass away.

At Fairstone we have a wide range of advisers across the country who are able to assist you in making or updating a Will, setting up a Lasting Power of Attorney agreement or answering any other questions you may have. Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

Wills and LPAs are not regulated by the FCA. The details relating to the laws of England & Wales are correct at the time of publication, and legislation may change. Fairstone Group Limited and associated companies are not legal advisers therefore specialist legal advice may be required before establishing Wills and LPAs under any jurisdiction applicable to place of residence.

Fairstone chartered financial planner Sandra Corkhill discusses the gender pension gap and steps you can take to help reduce it.

Being a volunteer for the PFS, I help to teach financial literacy in colleges and universities. Client case studies are used to teach good financial habits. Astute audience members will often ask, how much could I earn in my lifetime? Or why are we so old when we get a State Pension? At this point all debates get lively but it got me thinking…

We’ve all heard about the gender pay gap, but very few discuss the gender pensions gap, despite the fact so many women experience it. Women’s pensions at retirement are half the size of men’s, regardless of the sector they work in, new research has highlighted [1].

The gender pension gap is the percentage difference in income between men’s and women’s pensions and it begins at the very start of a woman’s career.

The research found that every single industry in the UK has a gender pensions gap, even those dominated by female workers. Considering women are likely to live four years [2] longer than men, this issue deepens as they need to have saved around 5% to 7% more at retirement age.

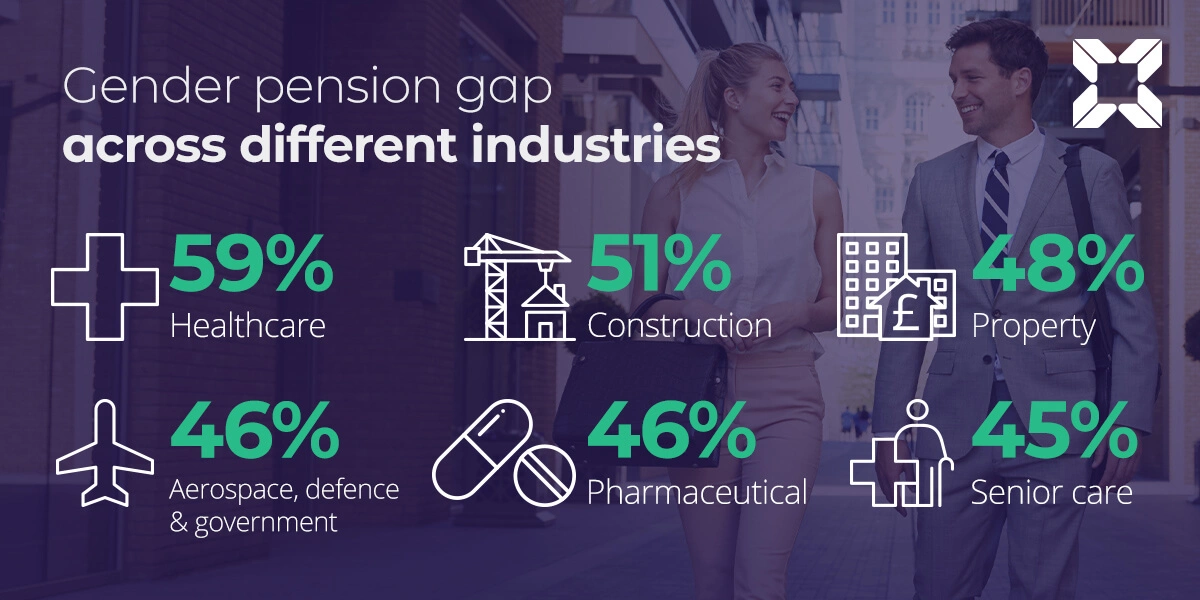

According to the research, the gender pensions gap exists regardless of average pay across different sectors, and ranges from a gap of 59% in the healthcare industry, to 13% in courier services. The healthcare (59%), construction (51%), real estate/property development (48%), pharmaceutical (46%), aerospace, defence and government services (46%), and senior care (45%) sectors were found to have the largest gender pensions gaps. Of these six sectors, three are key industries for female employment – healthcare, pharmaceuticals and senior care [3].

There are many reasons for the gender pensions gap, ranging from women holding fewer senior positions and being paid less, resulting in lower pensions contributions, to the fact they are more likely to take career breaks due to caring responsibilities. Of those that have taken a career break, 38% did not know the financial impact it had on their pension contributions [4].

Another potential driver is a significant gender confidence gap when it comes to managing pension pots. More than a quarter (28%) of women said they had confidence in their ability to make decisions about their pension, compared to almost half (48%) of men [5].

This lack of confidence extends further to other financial decisions, with women less likely than men to feel confident managing their investments (22% of women versus 41% of men), and their savings (56% of women versus 67% of men).

Women often have disrupted work patterns, career gaps and work part-time – this can impact their ability to save consistently for retirement without savings gaps. If you are concerned about your retirement plans and would like to review your pension options, please contact us.

| Match me to an adviser | Subscribe to receive updates |

Source data: [1] The analysis is based on LGIM’s proprietary data on c.4.5 million defined contribution members as at 1 April 2022 but does not take into account any other pension provision the customers may have elsewhere.

[3] According to the ratio of female members across the Legal & General book of business.

[4] Legal & General Insight Lab survey of 2,135 workplace members was conducted between 4–26 July 2022.

[5] Opinium survey of 2,001 UK adults was conducted between 4–8 February 2022.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless plan has a protected pension age).

Your pension income could also be affected by the interest rates at the time you take your benefits.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this article represent those of the author and do not constitute financial advice.

Over time, it is easy to lose touch with pension savings providers as we change jobs, move home and the companies we have worked for change ownership or close down. All these events over time may make it very difficult to find your valuable pension savings. So that means potentially ending up with a number of different pension pots. If you’re one of the millions of people with multiple pension pots, it may be appropriate to consider consolidating your defined contribution pension pots and bring them together.

Even if you have not had many jobs, you could still have a number of different pensions to keep track of. If appropriate, pension consolidation can simplify your finances and make it easier to keep track of your retirement savings.

Having said this, not all pension types can or should be transferred. It’s important to obtain professional advice so you know and can compare the features and benefits of the plan(s) you are thinking of transferring.

Pension consolidation is the process of combining multiple pension pots into one single pot. This can be done with a pension transfer or by opening a new pension and transferring your other pensions into it. You may want to do this to make it easier to keep track of your retirement savings, or to try and get a better rate of return on your investment.

But there are a few things to consider before consolidating your pensions, such as any exit fees that may be charged, and whether or not you will lose any valuable benefits such as guaranteed annuity rates.

If you think you might have lost a pension pot from a previous job, you can use the government’s Pension Tracing Service. This enables people to locate money previously saved for retirement, that is unclaimed. So, it is worth checking if you could have pension funds that have not been claimed.

Finally, you also need to bear in mind that pension savings are big targets for fraudsters. If someone contacts you unexpectedly offering to help you transfer your pot, it’s likely to be a scam. If you’re concerned, contact the Financial Conduct Authority (FCA) to check they’re legitimate.

You only have one retirement so you don’t want to make a costly mistake with your pensions that you could one day regret. Before you look to bring your pensions together, it’s essential to obtain professional advice. For more information about how we can assist you through this complex process, please contact us to discuss your situation.

| Match me to an adviser | Subscribe to receive updates |

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless plan has a protected pension age).

Your pension income could also be affected by the interest rates at the time you take your benefits.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this article represent those of the author and do not constitute financial advice.

The best time to retire will depend on a variety of factors, including your health, your financial situation and your personal preferences. If you’re in good health and you have a solid financial foundation, you may be able to enjoy a long and active retirement. On the other hand, if your health is declining or you’re struggling to make ends meet, retiring sooner may be the best option.

Ultimately, the decision of when to retire is a personal one. It’s important to do some soul searching and research before making a final decision. Once you’ve decided when the right time for you is, be sure to plan carefully to make the most of your retirement years.

You now need to think about the impact that inflation could have on your retirement income, and consider do you have enough to retire? Rising inflation can wipe years of retirement income off pension pots as savers must increase the amount they withdraw to maintain the same spending power each year.

Inflation can have a significant impact on your retirement plans. If inflation is high, the purchasing power of your savings will decrease over time. This means that you will need to save more money in order to maintain your standard of living in retirement.

To offset the impact of inflation, you may need to adjust your retirement plans. For example, you may need to save more money so that you can maintain your standard of living in retirement. Additionally, you may need to invest in assets that are less vulnerable to the effects of inflation. Bonds are one type of investment that can help protect your portfolio from inflation risk. In general, they can offer relative stability, but you need to take your age and risk tolerance into consideration.

While inflation can have a significant impact on your plans to retire, there are steps you can take to offset its effects. By saving more money and investing in assets that are less vulnerable to inflation, you can help ensure that your retirement plans remain on track. Additionally, by being aware of the potential effects of inflation, you can make adjustments to your plans as needed to account for its impact.

As you get closer to retirement, it’s important to start thinking about how inflation could impact your plans. While inflation can be a good thing if it leads to higher wages and increased economic activity, it can also be a problem if prices start rising faster than your income, as we’ve seen this year with inflation reaching a new 40-year high amid a cost-of-living squeeze.

By creating a model of your expected income and expenses, you can better plan for your retirement and make sure that you have enough money to cover your costs. This type of modelling can also help you to identify any potential shortfall in your retirement savings, so that you can make adjustments to your plans accordingly.

If you are nearing retirement or are already retired, cash flow modelling can help you: understand how much income you will need in retirement; work out how long your retirement savings will last; determine the best way to use your retirement savings to generate an income in retirement; and find out how different life events (such as taking a career break or downsizing your home) could impact your retirement cash flow.

Annuities can be a good way to combat rising inflation, as they provide a guaranteed stream of income that is not affected by changes in the cost of living. However, it is important to choose an annuity that has a high enough rate of return to outpace inflation, as otherwise you may end up losing purchasing power over time.

Some annuities offer built-in protection against inflation. For example, some annuities offer cost-of-living adjustments that increase payments to keep pace with inflation. This can help retirees maintain their purchasing power and keep up with the rising costs of living. While annuities are not the only solution for combating rising inflation, they can be a helpful tool for retirees.

Ultimately, whether or not an annuity is a good way to combat inflation depends on your individual circumstances. If you are concerned about preserving your purchasing power in retirement, an annuity can be a helpful tool. However, you should obtain professional financial advice to weigh the costs and risks associated with an annuity before making a decision.

If you’re sitting on too much cash right now, with inflation on the rise, that cash could be losing value, so you may want to rethink your strategy. Inflation is a natural occurrence that happens when the prices of goods and services start to increase. This can erode the purchasing power of your money, which means that you’ll need more money to buy the same items.

There are a few ways to combat inflation and ensure that your money keeps its value. One option is to invest in assets that are known to appreciate in value, such as stocks and shares or property. No matter what strategy you choose, it’s important to be aware of the impact that inflation can have on your finances. By being proactive, you can ensure that your money keeps its value over time.

When pension planning, your attitude to risk will play a big role in how your portfolio is structured. If you’re willing to take on more risk, you may be rewarded with higher returns. But if you’re not comfortable with risk, you may want to focus on preserving your capital.

Once you have a better idea of your risk tolerance, you can start to allocate your assets accordingly. For example, if you’re okay with some volatility, you may want to put some of your money into stocks and shares. But if you’re not comfortable with any volatility, you may want to keep your money in cash and bonds.

No matter how much risk you’re willing to take on, it’s important to remember that all investments come with some risk. There’s no such thing as a completely risk-free investment. But by understanding your risk tolerance, you can make sure that your portfolio is structured in a way that meets your needs.

Retirement is inevitable, but knowing exactly when to do so is often unclear. No matter when you actually begin your retirement, you’ll benefit from planning your post-work life as early as possible. If you would like to review your retirement plans, we’re here to listen. We look forward to hearing from you.

| Match me to an adviser | Subscribe to receive updates |

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless plan has a protected pension age).

Your pension income could also be affected by the interest rates at the time you take your benefits.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this article represent those of the author and do not constitute financial advice.

It is believed that having more female advisers in the sector could help women engage with financial advice and better plan for their future. The findings come in a survey by Fairstone, which incorporates one of the largest chartered planning firms in the UK, revealed that women are also more likely to seek financial advice when prompted by in response to a life event, such as divorce.

The survey results are more pertinent, given recent research by the Centre for Economics and Business Research, which revealed that by 2025, 60% of the UK’s wealth is predicted to be in the hands of women. We can see therefore that empowering women with knowledge and ensuring the engagement of women in the financial decisions and planning process, will be pivotal to their own financial success and that of the wider financial services industry.

Here Fairstone financial adviser Ruth Heath looks at the implications this could have for both financial advisers and their clients.

There are many reasons why women are not taking financial advice – feeling like they don’t have enough money to warrant it, or prioritising their partner’s financial planning above their own, both forming part of the picture.

Our survey revealed that women are often first motivated to seek financial advice when there is a significant life event such as bereavement or divorce, meaning that they could be facing difficult decisions while also dealing with the impact of a major change in circumstances. It highlights how vitally important it is for women to become financially educated and emphasises the value of starting the advice journey as early as possible so that they can feel prepared and supported when life events occur.

Tailored financial advice is critical for both short and long-term goals and for women, this is arguably more crucial, given that they are likely to live longer than men, meaning more retirement years to fund.

We need to look at how we make financial advice more accessible and inclusive, and advisers have a fundamental role to play. By helping to level the playing field, and through encouraging women to make the shift from saving to investing, we can allow them to compound their wealth and improve the long-term outlook for both their own lives and the legacy they leave for loved ones.

Encouragingly, the survey also revealed that almost half of female respondents (49%) felt that financial advice becoming the norm and starting that process at a young age, would be the biggest change within the sector in the future.

In a bid to raise awareness of the importance of tailored advice for women, Ruth will be hosting a webinar on September 22nd entitled ‘Empowering Women with Tailored Financial Advice’. She will look at what women should be considering at each stage of life and some of the decision-making tools available for building a strong financial plan.

| Sign up to webinar | Subscribe to receive updates |

*The Trustpilot figures are correct as of 13/09/2022

With wealth for millennials set to double in the next 20 years, it’s arguably time to get over the awkwardness and have the conversation now. One of the main reasons why people aren’t discussing their inheritance wishes is that they assume estate planning is not for them. That it is only necessary if you are very wealthy.

But nothing could be further from the truth. Most of us would like to leave a legacy and if you want to ensure your wishes are followed, obtaining professional advice and planning is essential, whatever your circumstances.

New research[1] has highlighted 58% of UK adults admit they have never discussed inheritance matters with their loved ones – with the reluctance to do so equally split between men and women. The findings revealed that the main reason people shy away from it is because they don’t believe they have enough assets to consider it worthwhile (18%).

However, for nearly half the population (49%), getting older is the main prompt for thinking about such matters. Other life events that have pushed people to confront it are: the birth of a child or the death of a parent (both 7%), followed by the COVID-19 pandemic or a health scare (both 4%). And there are certain people who hold the key to unlocking these conversations, with 54% saying their partner is the preferred person to talk to, followed by 22% who feel most comfortable chatting things through with their children. Worryingly, only 2% say they have discussed it with a solicitor and only 1% have done so with a professional financial adviser.

Making a Will provides a good reason to have a multi-generational family meeting about your inheritance wishes. Having an up-to-date Will is important for both you and your family. The truth is that having an out-of-date Will is as problematic as having no Will at all.

Once you have an up-to-date Will, talking it through with your professional financial adviser, they can then recommend a plan about how to approach your inheritance goals. Also remember, failing to prepare your children for what they may inherit can hinder their ability to handle money wisely.

You can give away £3,000 each year and this will not be subject to Inheritance Tax (commonly called IHT for short). In addition, parents can gift £5,000 to each child as a wedding gift, while grandparents can give £2,500.

Gifting money regularly throughout the year can be a great way to financially help loved ones and can also reduce your IHT liability. Some people will find it hard asking for money, so try and speak to your children and grandchildren to find out if you can help them with something specific, such as a new car or school fees.

Life events, like a birth, adoption, marriage or a family bereavement can make people evaluate their own plans. Use these opportunities as a way of talking to relatives about how you would like to pass on your wealth.

Many people are worried about how they will pay for social care when they get older. As a result, people may be starting to plan for this earlier than previous generations. It’s important to talk to your family about the care you want so they stay true to your wishes. This could be an ideal time to introduce the subject of inheritance, as estate planning and later life care go hand in hand.

If you find it hard to approach the subject of estate planning with your family then a good place to start could be talking about family heirlooms. People enjoy hearing stories about older relatives, even if they never had the chance to meet them. Talking about items that are important to you or were important to other family members can be a great way to start a conversation about estate planning.

Some people find the idea of discussing inheritance uncomfortable and wrongly assume that planning in advance is complicated, but if you don’t discuss things before it’s too late the situation can become much more thorny in the future, particularly if there is a blended family or if there is anything unexpected in the Will.

For more information about how our expert advisers at Fairstone can help you, please get in touch.

| Match me to an adviser | Subscribe to receive updates |

Source data: [1] The research of 3,000 nationally representative UK adults was commissioned by Find Out Now in November 2021 on behalf of Brewin Dolphin.

Achieving a million-pound ISA pot might sound like a stretch but you might be surprised at how achievable this goal of becoming an ISA millionaire is with some smart saving and consistent investing habits.

ISAs offer one of the most tax efficient ways to save for retirement and build wealth for the future. You can currently put up to £20,000 a year in ISAs, and any income or investment gains are free from income tax or capital gains tax – regardless of how much money you make.

ISAs are available either as cash or stocks and shares and over time you could build up a substantial amount of money while sheltering it from tax.

| You can find out more about ISAs by downloading our guide |

Over 2,000 people have become ISA millionaires since the tax-free wrapper was introduced 23 years ago, a few in their 30s and, astonishingly, even someone in their 20s.

Chartered Financial Planner, Nicola Cornish, shares 5 top tips on building a million pound ISA:

Growing your ISA will depend on two things, the amount you contribute and the rate of growth. While you can’t predict how the market will react, you can control your contributions.

With many demands on our money, particularly in the current climate, it may not be achievable to utilise your full ISA allowance each year, but the more you add and the earlier you get started, the better.

Putting aside a small amount each month can grow into a sizable sum. The important thing is getting started, and the earlier you do the more time your chosen investments have to grow.

As an example, take two investors, both investing for retirement in 40 years’ time. One starts investing £100 per month immediately, the other waits 20 years, but then invests £300 per month. The investments chosen both grow by 5% per year after charges. At retirement, the first investor will have spent £48,000 on their monthly contributions and the second investor £72,000. Yet despite having spent much less, the first investor’s retirement pot would be worth £152,602 compared to the second investor’s £123,310.

By starting early, you give yourself the best chance of harnessing the long-term growth of stock markets.

Good habits can be the key to strong investment returns. While you may have regular ISA contributions in place it can be easy to forget about them. As time goes on our circumstances undoubtedly change. If you have access to more available income via a pay rise or paying off some debt, it is always a good idea to review how you could utilise the money elsewhere.

A good habit is to review your contributions every year as even a small increase over the long-term can make a big difference.

As an example, imagine you start investing £300 a month from age 30, then increase your contribution by 6% each year (as you get older and potentially earn more). You could end up with an investment pot worth over £1 million by age 68.

The cornerstone of any investment portfolio should always be a diverse range of assets.

Whatever your budget, your aim should be to maximise gains and minimise losses. Diversifying your portfolio is a great way to do this. Spreading your investments across different products and areas makes you less dependent on the performance of any one element and helps to smooth out returns over the longer term.

| Read our ten tips for investing |

One way to do this is by utilising managed investment funds, which allow you to spread your money across lots of different shares at the same time, spreading the risk. Some of the fund sectors that have delivered for investors over the past decade include technology, biotech and smaller companies, although it must be remembered that past performance is not a guide to future returns.

Using investment trusts can also help boost returns although they are a riskier option. These often outperform fund equivalents because they can use gearing – or borrowing to invest.

There will always be fluctuations in the stock market as a result of political or economic situations which may cause some investors to feel unnerved and lead them to making short term knee-jerk reactions. The good news is that history shows us that recovery is inevitable and that those who stay invested for the long-term see better results than those who attempt to time the market.

Today’s ISA millionaires have seen many booms and busts and are a great example of how it is usually best to stick out tough times, remaining invested and adding to your investments. As a patient investor with a long-term horizon, time is on your side.

Regularly investing, and letting any increases build upon themselves, can make a huge difference over time thanks to the magic of compounding returns – using the income you earn from your investments to buy more shares in your portfolio and keep your money growing.

Compound investing works by allowing small amounts of money to grow into large amounts over time, like a snowball effect. It works best when you do nothing and just leave your money invested, making it particularly beneficial for those with long-term goals.

The route to becoming an ISA millionaire might not be a quick one but the evidence does show it is possible with commitment and discipline. To find out more about how you can maximise your investments get in touch with a Fairstone adviser today.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.