Savings & investment

Harry Sims

At first glance, cashflow modelling doesn’t sound like the most exciting thing in the world.

But what if I told you that I’ve seen clients so shocked and pleasantly surprised when I’ve taken them through a cashflow modelling exercise that they’ve taken the print-out straight to the pub to show their friends?

Used correctly, cash flow modelling can provide you with the roadmap to get to your desired financial destination – or maybe even somewhere you never thought you could get to.

It can, literally, change your life.

How? Let me explain.

Put very simply, cash flow modelling is a form of software which allows you to map out how much money you could have over time.

You input figures such as your salary, the current value of any assets you have, what investments you have, the value of your house, etc.

You can then use that information to model what will happen to your money under a wide variety of different scenarios.

With each scenario, the software will show you in number and graph form how much (or how little) money you will have every year for however many years you specify.

Because the software is so adaptable and allows for so many variables, cash flow modelling can be used for almost any kind of personal financial forecast.

For example, you can see what effect a rise or a fall in inflation will have, what difference a 3% increase in annual investment returns will have on your assets and how much your pension could increase if you invest another £100 a month.

Cashflow modelling is particularly good at demonstrating the difference between potential returns at different investment risk levels because the software has market data dating back to 1990.

This means that it can account for and illustrate the effects of market volatility and market shocks such as the dotcom boom and bust of the early 2000s and the financial crisis of 2008.

It’s also useful at every stage of your financial journey, from first starting a pension to accumulating wealth, through drawdown of your pension pot and even into planning for potential care costs later in life.

The best way to show what cash-flow modelling can do? A real example.

Imagine turning £18,000 into £60,000 overnight.

Meet my client. She earns £160,000. Her partner earns £42,000.

Their question: Are we being tax-efficient – and how do we afford nursery fees without wrecking cash flow (their child is about to go nursery)?

They’ve got £50,000 in the bank and £250,000 in pensions. The pensions are invested cautiously (risk level 4/10) and modelled back to 1990.

We tested two changes:

Sacrificing £60,000 of salary drops her taxable income to £100,000 – the threshold where free childcare vouchers kicks back in.

Before: £160,000 salary → £95,786 net

Partner: £42,000 → £33,759 net

Joint: £130,346 net

Less £93,000 annual spend (including £10,000 nursery) → £37,346 left

After the change: joint net income falls to £102,317 – a drop of £28,029.

But £60,000 lands in her pension overnight.

And childcare costs of £10,000 disappear, cutting annual spending to £83,000 from £93,000.

Net drop in net income – £18,000.

Effectively, they’ve swapped £18,000 of lost disposable income for £60,000 of long-term wealth.

They’ll repeat it for three years – £180,000 total into pensions for a net cost today of around £54,000.

There are plenty of moving parts, but we assume any surplus income (above spending and pension contribution) sits in cash which, to be clear, wouldn’t be our recommendation.

Then we ran two forecasts:

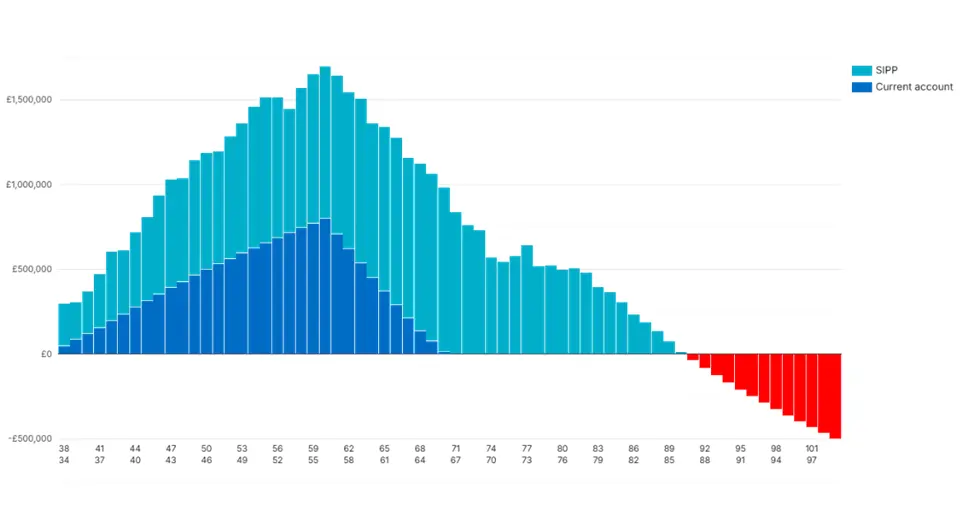

Baseline: No pension contributions, cautious portfolio (risk 4/10), nursery fees paid from post-tax income. We also assume they will need to withdrawal £6,000 a month from their portfolio from age 60 to fund their lifestyle in retirement.

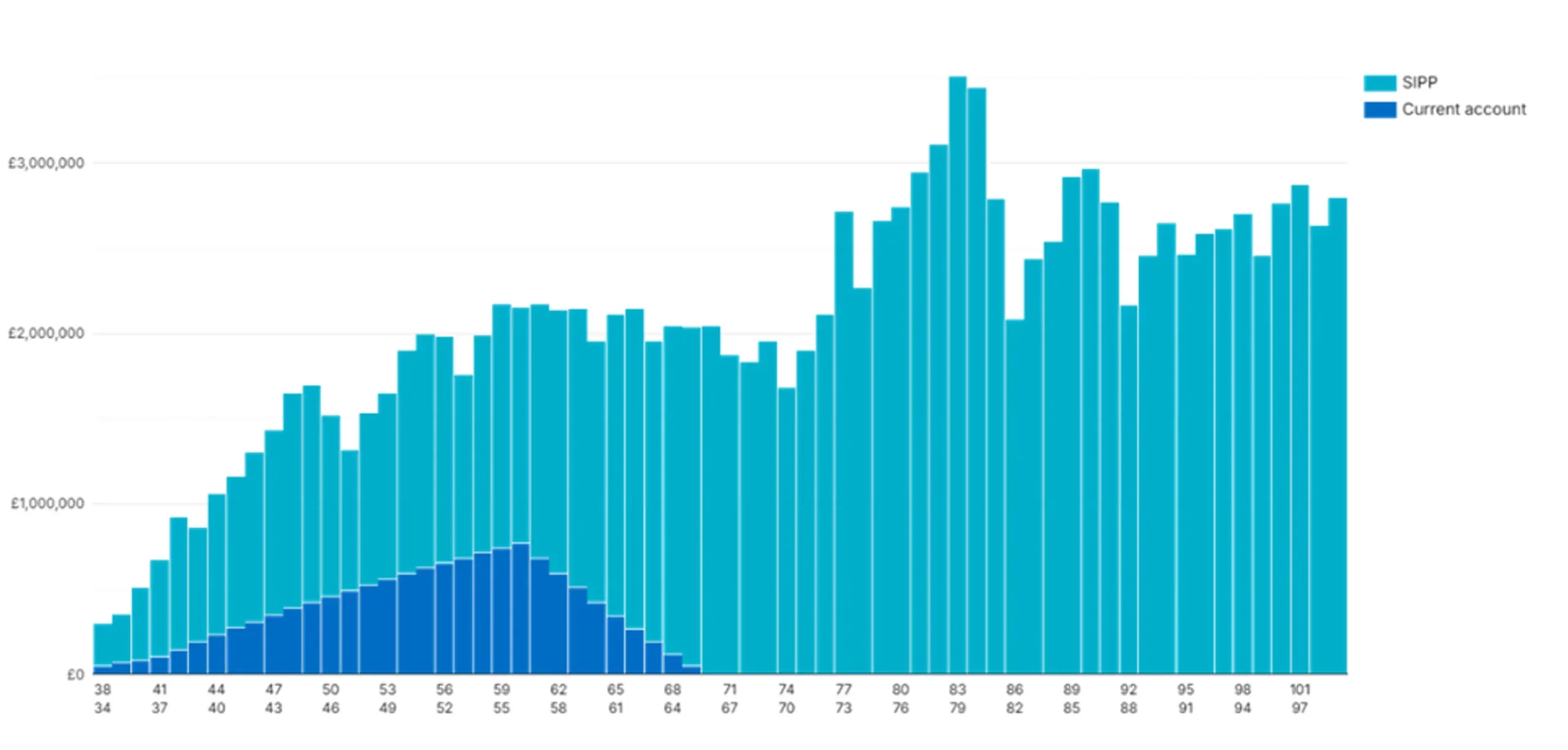

Revised: £60,000 p.a. pension contributions, higher-growth portfolio (risk 8/10), claiming childcare vouchers and allowances. We also assume they will need to withdrawal £6,000 a month from their portfolio from age 60 to fund their lifestyle in retirement.

The cashflow modelling graphs tell the story (amounts in red indicate a shortfall in funds):

Baseline scenario:

Revised scenario:

Two key decisions – sacrificing an amount of income into your pension over the next three years while it remains the most tax-efficient time to do so and increasing your risk profile – can have a powerful impact.

While it is important to stress that investments can go down in value as well as increase and that cashflow modelling produces forecasts rather than definite outcomes, the potential scenarios from those different decisions are very clear to see.

Talking about money in theory is never as impactful as talking about money in practice.

Not only does cash flow modelling look at your potential future real-life money situation, it gives you the facts and figures in black and white.

It is often said that seeing is believing and in that respect, cashflow modelling is the best way in which you can see your future money situation.

When you can visualise your life on a screen, it feels tangible and, in many cases, it feels achievable.

Clients come away after a cashflow modelling exercise with a real sense of security, of knowing that they’re doing the right thing to achieve their financial goals.

Sometimes it can unlock some really life-changing decisions and give people the confidence and peace of mind to put those decisions into action.

It’s also important to point out that cash flow modelling isn’t just for the future: it can help people today as well as tomorrow.

For example, after going through a cashflow modelling exercise with one client, I was able to say to them “actually, you’re saving too much money at the moment. You can afford to go on that exotic holiday this year that you’ve always thought you couldn’t”.

Cashflow modelling can help people in the here and now, let them enjoy their lives more and not put things off.

It would be a mistake to think cashflow modelling is only useful if you’re near retirement and want to see how long your pension pot will last.

For example, it can be tremendously helpful for people in their 20s or 30s who are wondering whether they can afford to start a family and, if so, how large a family that could be.

Equally, if you have retired but want to know how to make your money go further, cashflow modelling will be able to show you the likely outcomes of different scenarios.

Far from being a dry technical tool, cashflow modelling is one of the most powerful and insightful weapons in the financial adviser’s armoury.

While it’s not a crystal ball, it’s definitely a roadmap – and one which you would do well to consult.

To find out how cashflow modelling can help map out your future, get in touch today.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

For further information, please contact:

Savings & investment

Pension & retirement

Savings & investment

")

Savings & investment

Savings & investment

Savings & investment

For further information, please contact: