Market Updates

Imogen Hambly

Discover more insights from our Divisional Director, Peter Donaldson, and Portfolio Manager, Imogen Hambly, as they delve deeper into last month’s market update.

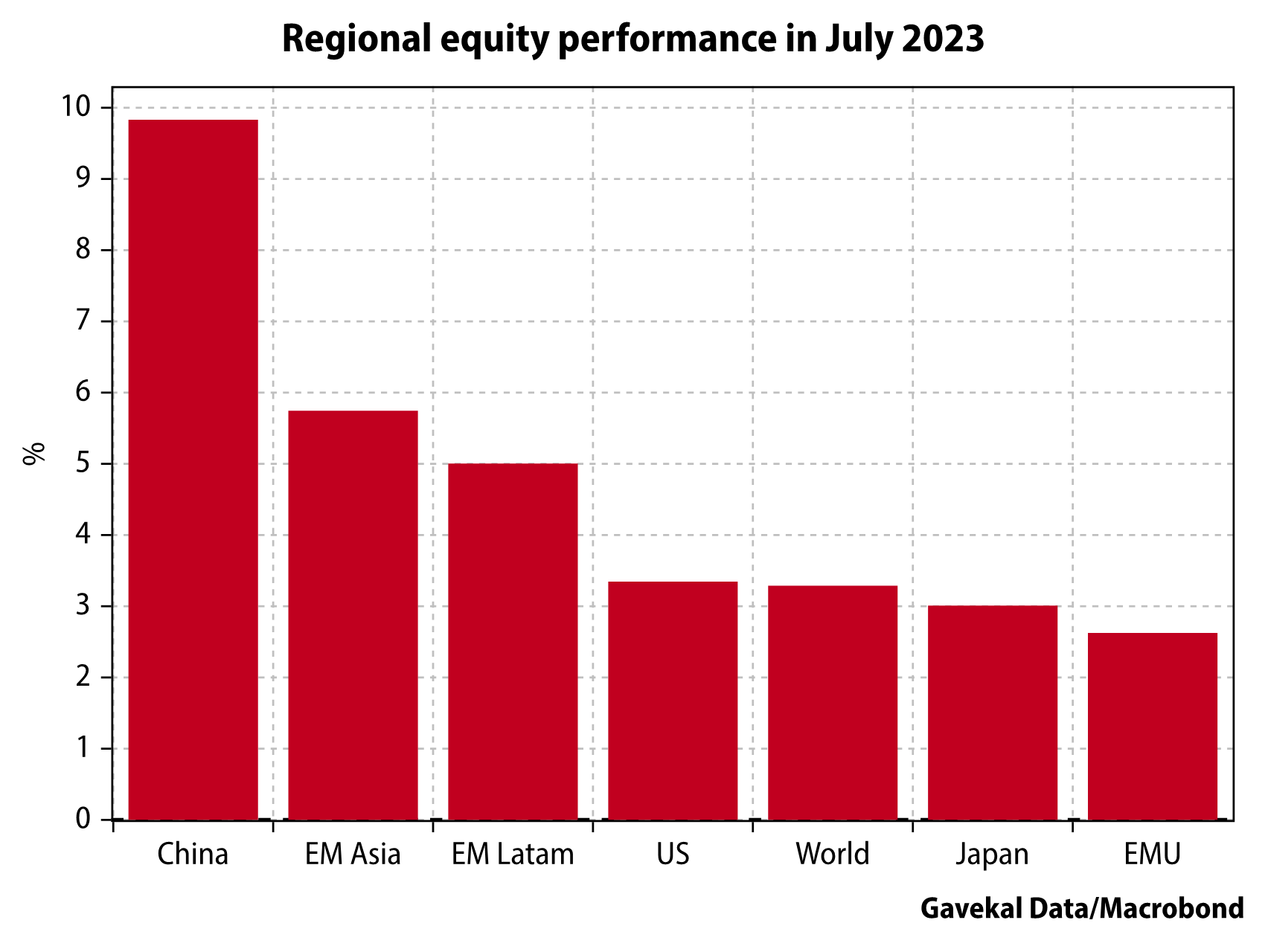

Global equity markets returns were positive through July, with the global equity index gaining 3.2%, in local currency. On a regional basis, Asia and emerging markets outperformed, benefitting from a resurgence in positive sentiment towards Chinese equities. In pound terms, the MSCI Emerging Markets index (shown below in red) and MSCI Asia ex Japan index (below in yellow) had their best months since January, gaining 5.0% and 4.9%, respectively.

Elsewhere, developed market equities also posted gains, with the technology heavy Nasdaq index (the pink line above) continuing to grind upwards, adding a further 2.6%, in pound terms, through the month.

While positive, returns from European equities (shown above in purple) were slightly more lacklustre, with analysts now beginning to pare back their growth expectations, as the Eurozone flirts with a recession. Core inflation levels – that is, inflation less the more volatile food and energy components – across the region remain elevated, while manufacturing output has meaningfully slowed over the past few months and remains on a clear downward trajectory.

However, as sentiment towards Europe has weakened, that towards China has shown signs of strengthening. The past six months have seen equities across the region struggle in the face of slower than expected growth, falling exports and a burgeoning youth unemployment rate. But, despite these ongoing headwinds, July saw a number of encouraging policy developments that offer the potential to boost growth across, among others, the region’s ailing property and technology sectors. Investors welcomed this news, with positive price action seen across Chinese equities, leading to the region’s notable outperformance, per the chart below.

Moving on to the US market, where the mega cap technology stocks and those related to generative artificial intelligence have seen blowout returns over the past few months, what was witnessed through July was a far more broad-based rally in prices. The chart below shows returns of the US based S&P 500 market cap weighted index (the line in black) versus the S&P 500 equally weighted index (in red).

Through early Q2, the market cap weighted index saw a distinct uptick in returns versus the equally weighted index, indicating a concentrated rally in the largest companies. June and July, however, have seen the two indices move in tandem, with the equally weighted index slightly outperforming of late, raising hopes that this will be a more sustainable rally in US equity prices.

As interest rates continue to rise though and the effects of past rate hikes start to be felt, so do downward pressures on growth, corporate earnings, and broad equity markets.

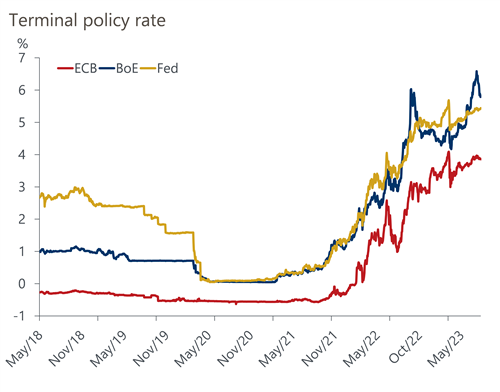

Both the US Federal Reserve and European Central Bank (the ECB) raised their policy rates by a further 25bps during July, a move that takes the ECB’s headline interest rate to its highest level in 22 years. Across Europe, the US, and the UK, Central banks have undertaken one of the fast rate hiking cycles on record as they fight to quell sticky inflation levels. But, with growth weakening and inflation levels moderating, as the chart below indicates, terminal rate expectations are now stabilising and even reversing, as is the case for the Bank of England (the blue line)

The end of the rate hiking cycle is something both equity and bond investors are keeping a keen eye open for.

On the whole, bond investors are looking through the slowdown in growth and are instead taking solace from strong labour market and consumer spending data, as well as the number of healthy corporate earnings reports that came out during the Q2 reporting season. Through July, this meant we once again saw outperformance from the higher risk portion of market, with high yield bonds (shown below in yellow) gaining 2.0%, while global investment grade credit (shown in purple) added 0.9%. Government bonds had another tricky period, with yields edging up – recall that bond yields and prices move in opposite directions – on the back of the aforementioned policy rate moves.

All things considered, we are seeing a lot of mixed signals from macro-economic data and markets at the moment. Across developed markets, growth and manufacturing are slowing, but labour markets are still proving extremely resilient. Corporate earnings are generally holding up, with a number of companies beating expectations recently – however, as the effects of interest rate hikes begin to bite, there are risks to the downside here.

From an investment perspective, plenty of opportunity exists across global markets, but as always, we are led to focus on a number of key factors – good quality companies, attractive valuations and above all else, diversification.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: