Market Updates

Oliver Stone

June saw a broadly positive performance across equity markets, with most global indices rising as risk sentiment improved. This came despite escalating geopolitical tensions in the Middle East. US equities in the form of the tech-heavy NASDAQ index were the top performers, rising by 4.6% in pound terms, while the UK was a notable laggard, with the FTSE 100 posting negative returns of -0.13%, reflecting domestic macroeconomic and political concerns.

Silver prices surged nearly 9.5% during the month, beginning to catch up with gold’s performance which has been setting a series of new all-time highs over the past year. This pattern is typical in the early stages of a precious metals bull market and may continue if the trend persists:

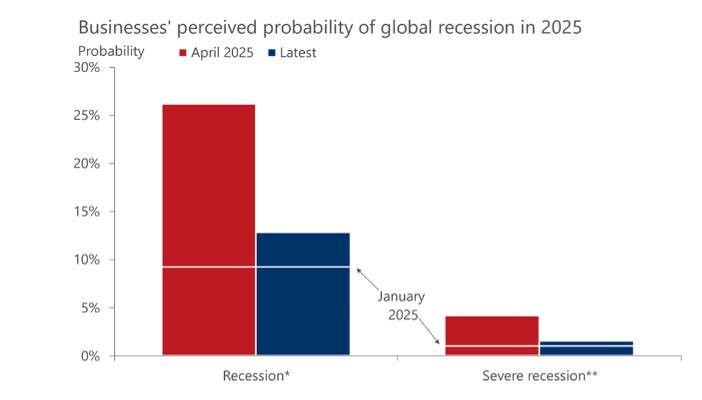

This improved sentiment followed the delay in US tariff implementation, with President Trump signaling a willingness to negotiate. This helped reduce perceived recession risks among global corporates, although growth expectations still remain well below levels seen earlier in the year:

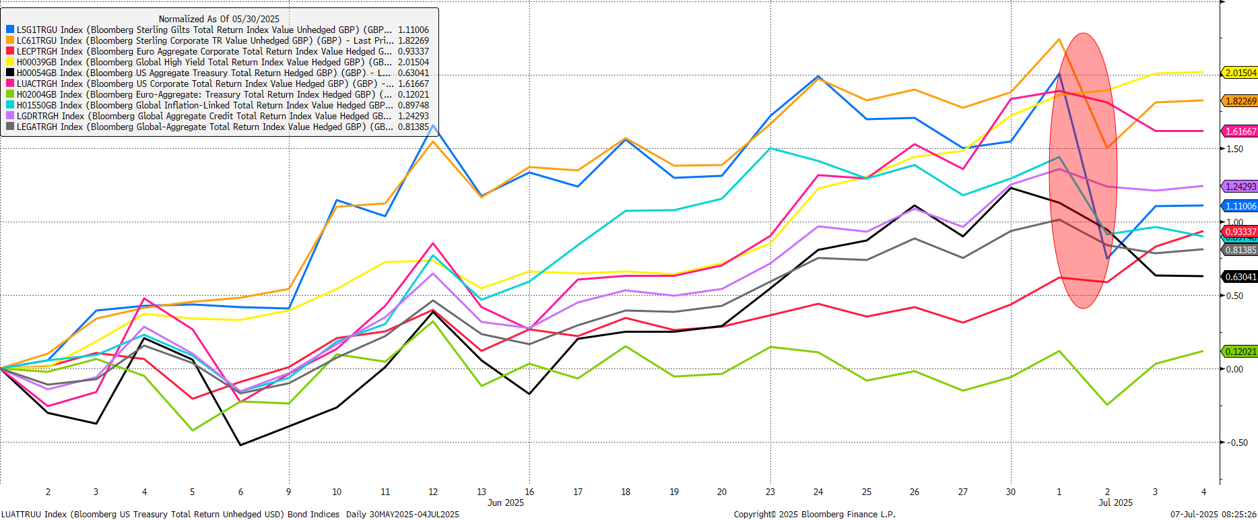

Bond markets were volatile. Sterling assets performed well during June as falling gilt yields (and therefore higher prices) reflected weaker macroeconomic data. However, a sharp drop in gilt prices occurred early in July following a session of Prime Minister’s Questions in which the Chancellor’s job security was questioned, serving to highlight the fragility of UK asset prices to political developments.

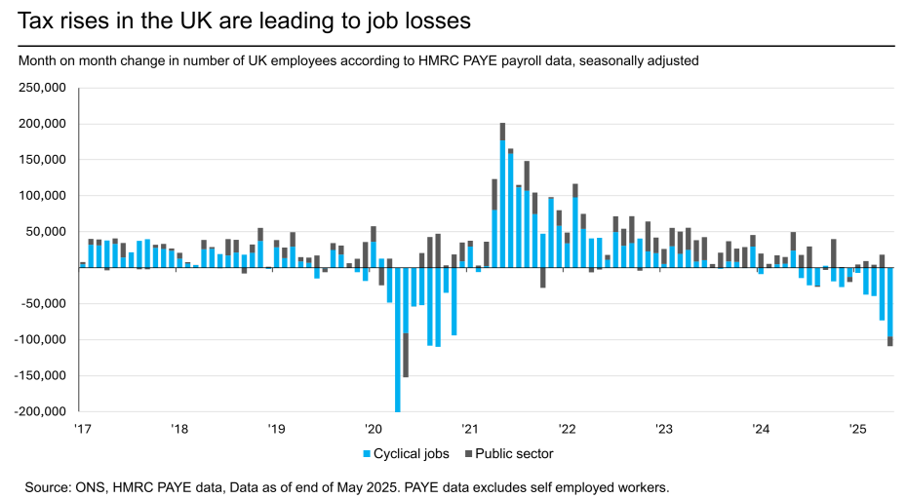

UK jobs data weakened further, with continued losses in cyclical sectors and high candidate availability reported by recruiters. This, combined with fiscal pressures, suggests the UK government may need to tighten policy by £20–30bn in the autumn budget, likely through further tax hikes and threshold freezes.

This places the government in a Catch-22 position; bond markets are expected to react negatively to any perceived fiscal loosening, but equity markets will likely react negatively to further fiscal tightening as animal spirits are crushed:

Geopolitical tensions escalated mid-month with Israel’s Operation Rising Lion and subsequent Iranian retaliation. The US intervened with Operation Midnight Hammer, but a ceasefire was reached within 12 days. Oil and gold prices spiked initially, but markets quickly stabilised, reflecting investor resilience to short-term geopolitical shocks.

Brent crude rose to nearly $80 per barrel during the conflict, driven by fears of supply disruption in the Strait of Hormuz. Although prices eased after the ceasefire, they remain elevated, reflecting a persistent geopolitical risk premium:

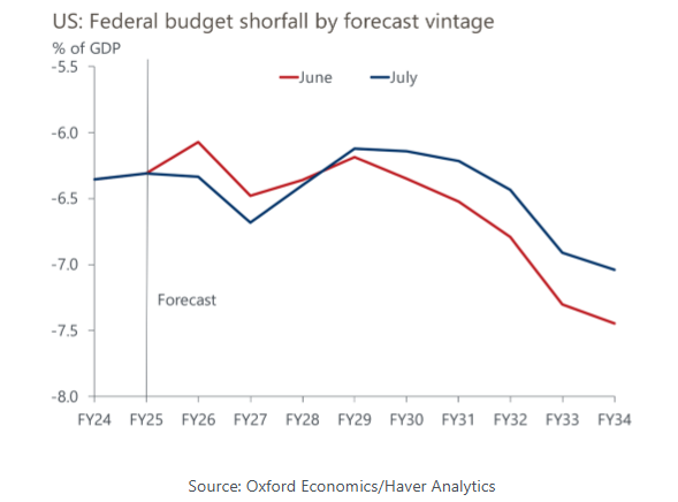

The US passed the One Big Beautiful Bill (OBBB), a major tax-and-spending package that will significantly widen the fiscal deficit. The deficit is expected to reach nearly 7% of GDP over the next few years, raising concerns about long-term fiscal sustainability. This has reinforced our preference for shorter-duration bonds:

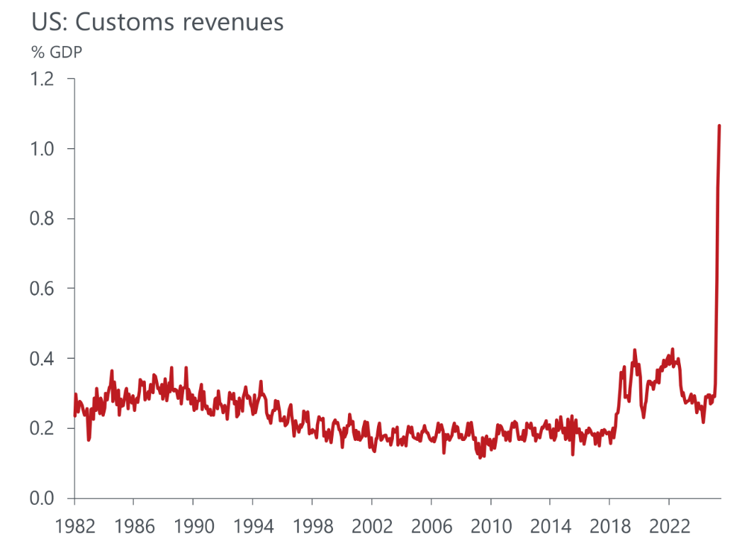

Tariff policy remains a key macroeconomic variable. The 10% universal tariff and other measures are expected to raise $2.5 trillion in revenue over the next decade. Given the president’s broad authority over trade policy, further changes could occur rapidly and without congressional approval. Retaliatory measures from other countries remain a risk, particularly in the form of non-tariff barriers.

In summary, June was marked by strong equity performance, volatile bond markets, and significant geopolitical and fiscal developments. Diversification remains essential in navigating these complex dynamics and mitigating risks associated with market volatility and economic uncertainty.

For a deeper dive in to the June update, listen to our Market Update podcast where Portfolio Manager Imogen Hambly and Investment Director Oliver Stone unpack the key market events and trends.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: