Market Updates

Oliver Stone

November delivered a two phase adjustment across equities and bonds. The first half was dominated by valuation compression in AI linked equities and uncertainty created by the U.S. data blackout; the second half saw a measured recovery as disinflation signals and the probability of a December policy cut reasserted.

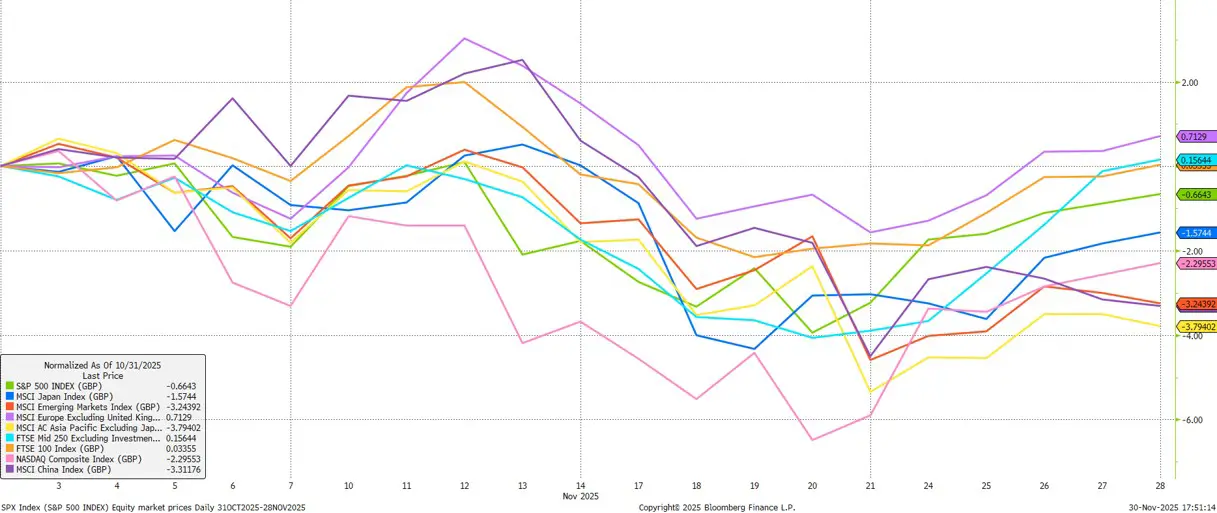

Headline U.S. equities ended the month down around 0.66%, but the composition of returns shifted meaningfully: equal weighted benchmarks and small caps outperformed their market cap weighted peers, value equities exceeded growth counterparts, and sector dispersion widened as leadership narrowed away from the largest technology constituents.

Outside the U.S., developed ex U.S. equities generally provided positive returns, with the exception of Japan, while emerging markets underperformed after a strong year to date run. Asia technology stocks weakened with pressure on high beta names, and China/Taiwan bellwethers reminded investors of the fragility of momentum when positioning is crowded:

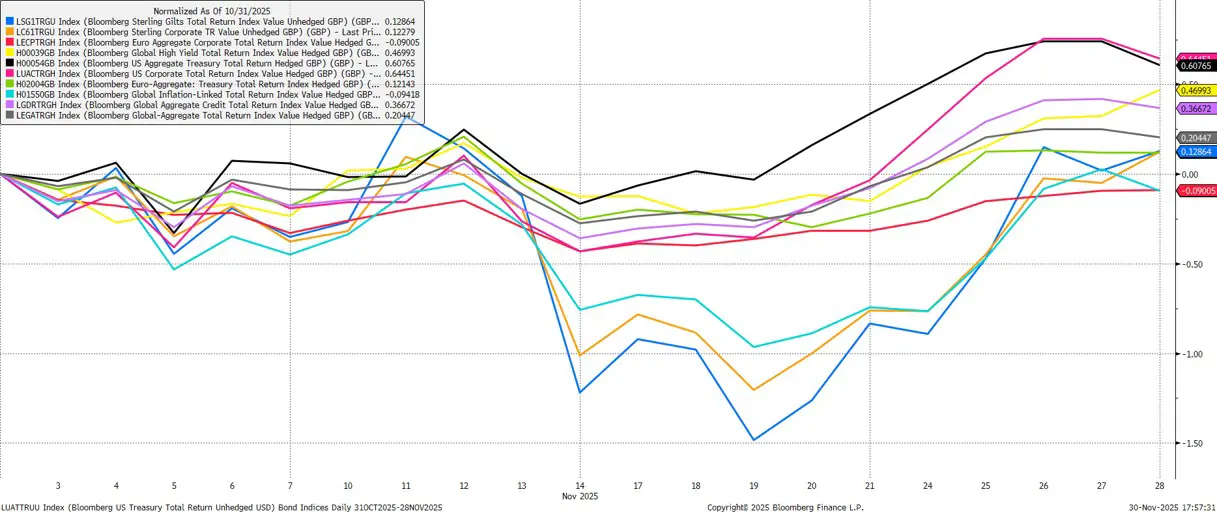

Fixed income offered more clarity than equities in November. With the U.S. government effectively reopening on 12 November and alternative inflation indicators signalling ongoing disinflation, the 10‑year Treasury yield drifted toward the 4.0% area into month‑end before firming slightly in early December. This path supported investment grade and high yield bonds in the US and Europe, and while UK bonds were volatile around the budget and the OBR’s accidental leak, prices recovered as investors focused on fiscal‑rule adherence, issuance trajectories and medium‑term discipline; factors that matter to the marginal buyer more than the political theatrics:

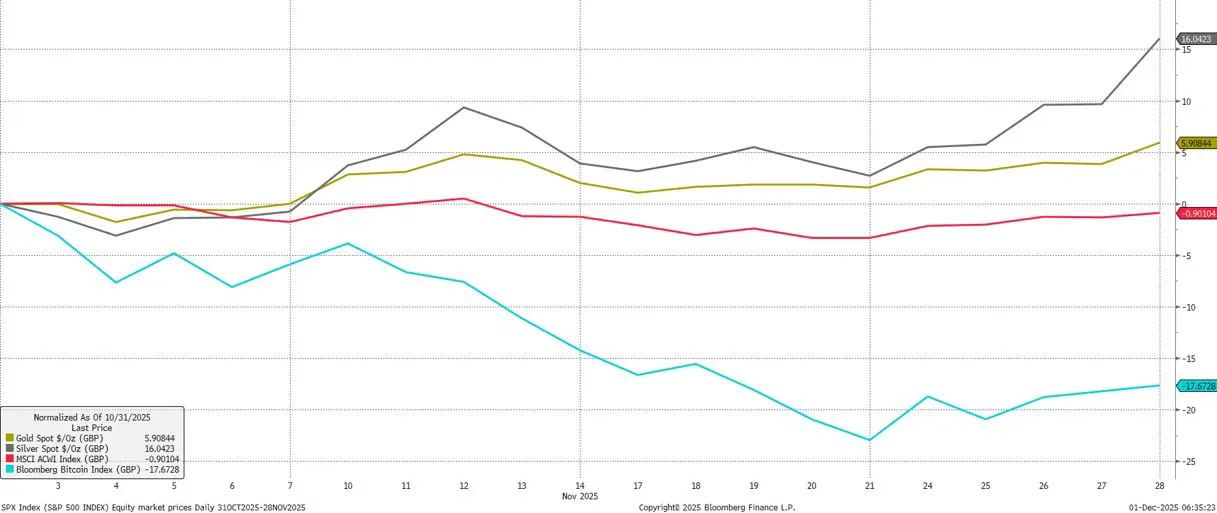

Currencies and commodities reinforced the month’s regime. Sterling firmed modestly on improved policy clarity despite tax‑raising measures; the yen weakened further on looser domestic policy settings and renewed geopolitical friction. Precious metals extended their structural leadership. Gold advanced by nearly 6% to close near $4,220/oz, supported by lower real yields, continued central‑bank demand and persistent macro hedging. Silver rose by over 16% to fresh highs around $56–57/oz, underpinned by tight physical markets and industrial demand. The magnitude of precious‑metal gains contrasted with weakness in crypto and high‑momentum technology, offering practical diversification rather than merely theoretical hedging:

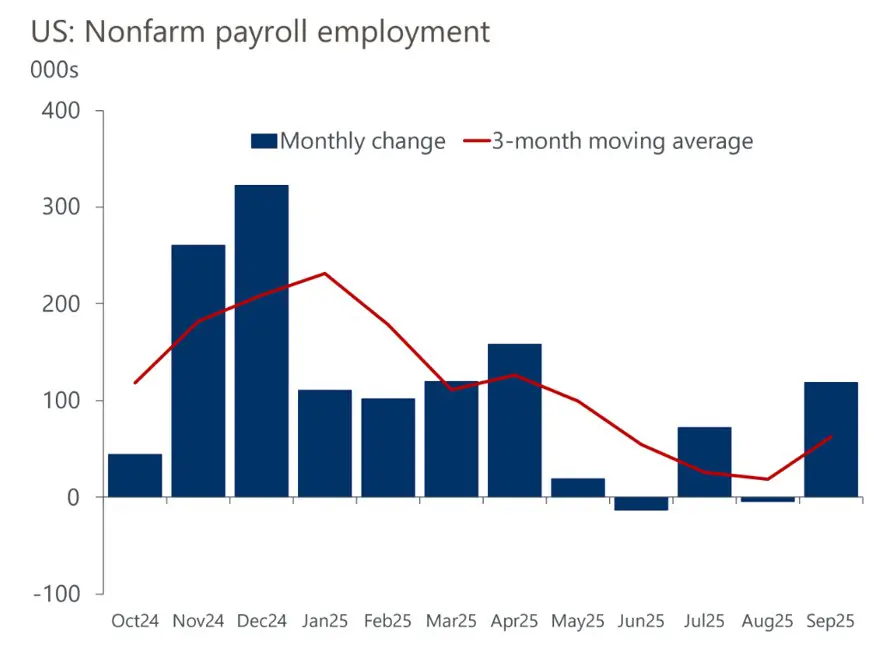

Macro policy developments were relevant through their impact on expectations rather than via surprise. In the United States, the 43‑day government shutdown impaired the publication of key data releases, including the cancellation of October CPI, and forced markets to triangulate from private proxies and high‑frequency series. As agencies resumed operations, rate‑cut odds re‑accelerated into month‑end against a backdrop of moderating inflation and softening labour‑market indicators:

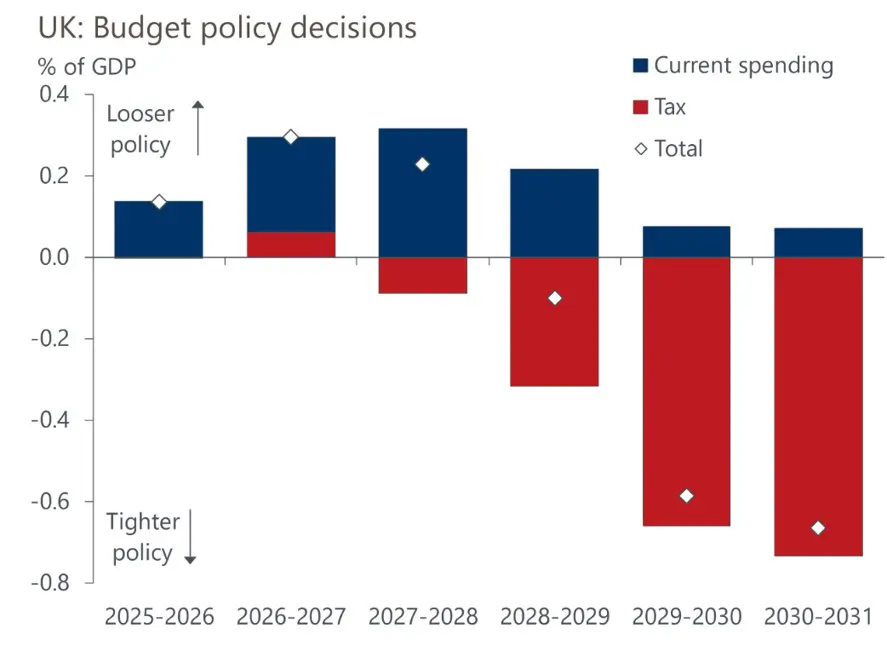

In the United Kingdom, announced budget policies were slated to raise roughly £26bn in new tax measures by 2029/30; lifting fiscal headroom to c.£22bn and preserving adherence to the government’s fiscal rules. While productivity downgrades and the back‑loaded nature of the planned fiscal tightening tempered medium‑term growth expectations, the near‑term market reaction centred on sustainability rather than stimulus:

The Bank of England voted 5–4 on 6 November to hold Bank Rate at 4.0%, judging disinflation to be proceeding, and signalled that further reductions would be contingent on continued progress toward the 2% target. The message was gradualism rather than haste. The ECB maintained its meeting‑by‑meeting stance and characterised policy as “in a good place” with inflation near target, reducing the likelihood of policy‑driven surprises in euro‑area assets. Combined, the major central banks’ posture supports a lower‑volatility backdrop for duration and quality credit, with the locus of uncertainty shifting to growth composition rather than inflation trajectory.

As we head into 2026, there are reasons for continued optimism: inflation is easing, interest rates should drift down gradually, and growth will likely be positive across regions and sectors, if not stellar. That mix favours a well‑diversified portfolio—balancing risk exposures to buffer against any unpleasant surprises that will undoubtedly occur as we move through the year.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: