Market Updates

Oliver Stone

")

After a frantic weekend of classic British political machinations – including the real possibility of a comeback for previous incumbent Boris Johnson – Rishi Sunak was duly anointed by MPs as the new Prime Minister on 24th October. He secured the public backing of over 200 of his fellow MPs while his nearest rival, Penny Mordaunt, secured only 30, hopefully implying that the risk of future short-term political turbulence is now much lower.

The new Prime Minister has since provided investors with a calming tonic of (planned) fiscal sustainability and spending cuts, though the full detail of his and the Chancellor’s plans won’t now be revealed until 17th November.

The delay in this announcement has come in part because of the sharp fall in government bond yields seen since Liz Truss’s resignation – lower bond yields mean the Office for Budget Responsibility’s (OBR) forecast for debt interest costs will be substantially lower than just two weeks prior, giving Sunak and Hunt much greater flexibility around policy choices.

That said, difficult choices still need to be made on tax and spending, and with forward looking economic indicators deteriorating, it seems like life for our new leader will not be getting easier any time soon.

As implied above, market conditions for UK assets did improve substantially in October, though from a very low base.

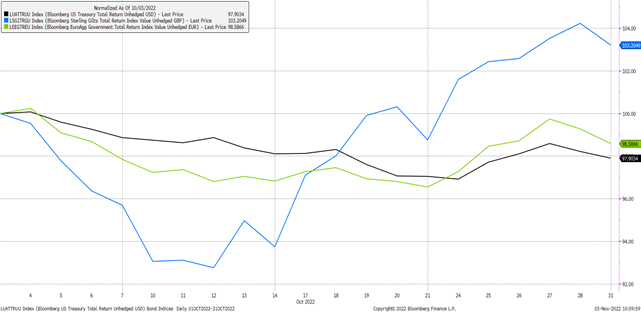

The first chart below shows government bond indices over the month, with Gilts in blue rising by 3.2% in aggregate; ahead of European and US counterparts:

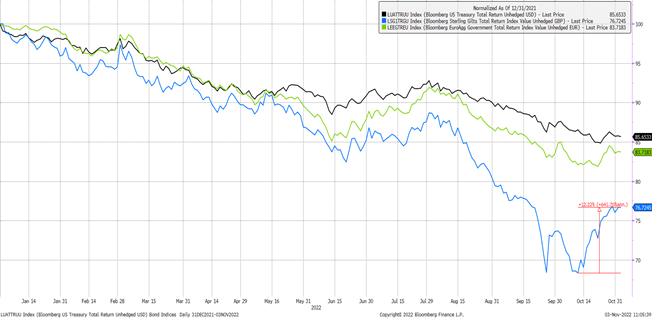

The second chart places October’s performance in a wider context, showing that despite a sharp rise of more than 12% from its low point, the Gilt index is still down more than 25% in the year-to-date, and still looks out of place versus its peers:

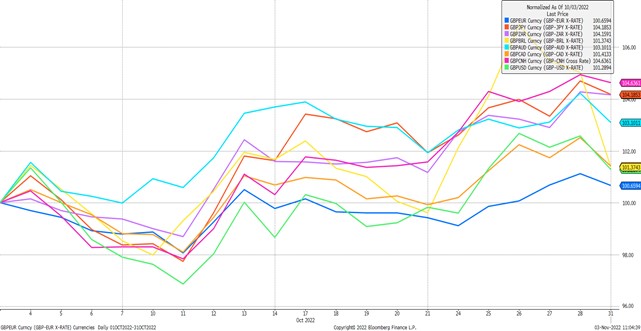

The pound also rallied against all major currencies from an initial low at the beginning of the month as the third chart shows, though anaemically against developed market peers including the euro and the US dollar.

Generally, we are cautiously optimistic that the increased level of political stability should keep feeding through to bond and currency markets:

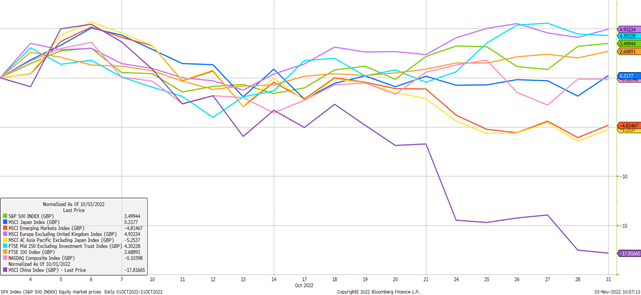

Equity markets were split decisively along developed and emerging lines, with the latter strongly outperforming the former in pound terms. Here again we can see an improvement in domestic UK fortunes, with the mid-cap FTSE 250 index rising strongly by 4.3%; near the top of the pack, while the large-cap FTSE 100 index rose by a still-impressive 2.7%.

European equities were also strong, rising by 4.9% in apparent discord with the current market narrative. While the outlook for the region remains bleak, there has been some short-term relief in the form of much lower near-term gas and electricity prices as storage levels have been high, and the weather unseasonably warm:

At the other end of the spectrum, Asian and emerging market equities were particularly weak, led lower by a very poor month for Chinese equities which fell by 17.8%. During the month the Chinese Communist Party Congress took place which resulted in an unambiguous outcome: Xi Jinping now has complete control of the leadership structure and will most likely remain in power for years to come.

Xi was able to pack the Politburo Standing Committee – the top leadership body – with allies, and publicly humiliated dissenters, with the pointed removal of previous leader Hu Jintao from the Congress hall on the final day of proceedings leaving onlookers with no doubt as to where power lay.

Despite much talk of growth during the Congress, market participants reacted unfavourably to the political outcomes, with concerns raised around a lack of diversity in interests and ideas leading to further a further politicisation of economic policymaking, with negative outcomes. Growth has already slowed markedly in China, in no small part due to continued, aggressive zero-Covid measures, with geopolitical issues around the threat of technological decoupling and souring US-China trade relations also lurking.

This being said, our conversations with investors intimately involved in the region bring more reasons for optimism. The Chinese equity market is now extremely cheap, and with the Party Congress now out of the way, focus can turn more towards concrete steps to help solidify a growth recovery. Geopolitical risk remains, and while nothing can ever be truly ruled out as 2022 has taught us, we do not see the region as having become uninvestable – quite the opposite.

We expect further volatility across all asset classes in the run-in to the year-end, with focus still on central banks and their monetary tightening plans, along with the continued fallout in eastern Europe, all of which as always points to the importance of diversification across portfolios.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: