Market Updates

Oliver Stone

")

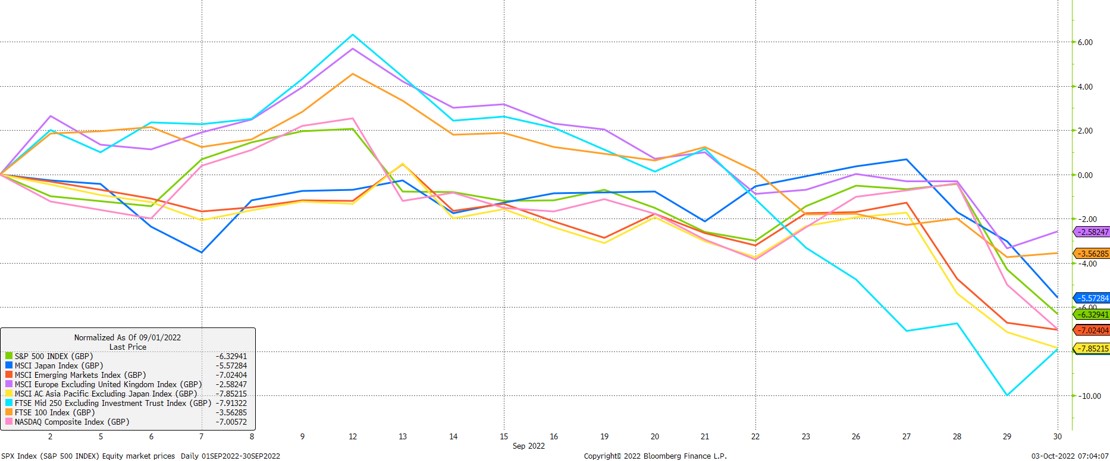

As the first chart below shows, all major equity regions were negative in pound terms, with European and UK large-cap stocks faring best, while emerging market, Asian and UK mid-caps were worst:

Over the year-to-date, UK large-cap equities in the form of the FTSE 100 index remain standout performers in relative terms. The second chart below shows that despite their making a loss of 6.6%, this is far in advance of most other major indices, with European equities for example falling by more than 19% over the same time period. As we have commented before, this phenomenon has occurred due to a combination of the FTSE 100’s international focus, and its composition leaning more towards cyclical sectors, particularly energy:

The outperformance of UK equities is even more stark when viewed in local currency terms – i.e. unadjusted for the pound’s weakness. Again, this is something we have commented on several times through 2022, but it bears repeating how significant the pound’s weakness has been. The third chart below shows the scale of international equities’ underperformance when viewed in this way; UK investors have been well shielded from this due to the pound:

UK equities’ outperformance is all the more impressive given the domestic machinations that have occurred during September and October. Following the now ex-Chancellor, Kwasi Kwarteng’s, ‘mini-budget’ on 23rd September, we saw astonishing levels of volatility in UK government bond and currency markets, which has almost immediately started to impact the wider economy.

The Government’s announcements did not entirely come out of the blue. Measures to cap energy prices for consumers and businesses had long been expected, as had some notions of fiscal easing elsewhere, but on the day and subsequently, two aspects caught investors by surprise: the scale of the intended action, and the lack of balancing measures to fund it.

The energy package alone was expected to cost up to £150bn over its two-year duration, though given the volatility of natural gas prices, this figure is, in reality, open ended. Additionally, Kwarteng presented a reversal of the previous increase in national insurance contributions, the removal of the top rate of tax, a cut to the basic rate of income tax and a cut to stamp duty, amongst various other measures. On top of that, over the subsequent weekend, he explicitly stated that he expected to deliver further tax cuts in the near future.

Crucially, this was all to be met by massive, increased borrowing, at a time where interest rates are rising, and global central banks, including the Bank of England are turning increasingly hawkish to combat high and sticky inflation.

The Government chose not to involve the Office for Budget Responsibility (OBR) in this first instance, apparently keen to front-load its policy agenda. This meant that no independent analysis was provided as to the impact of these measures on the outlook for government debt sustainability. Perhaps not surprisingly then, these factors combined to produce the moves seen in the last week of September and into October, with the Bank of England (BoE) forced to rapidly intervene in size to stop the Gilt market from seizing up.

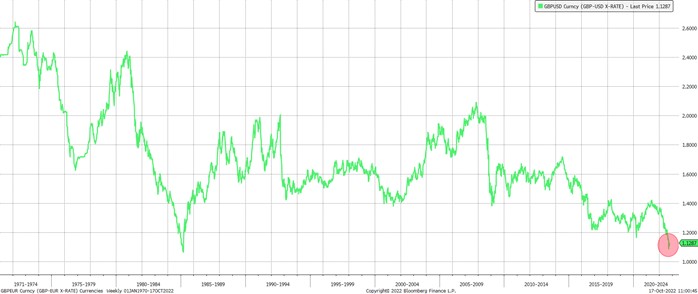

Starting with the pound, the chart below shows its performance versus the US dollar in 2022, with the red oval highlighting the period following the mini-budget. The pound has been on a downwards trajectory versus the dollar this year, along with many other currencies, but this most recent move has been out of kilter with other competitors, reaching a new all-time intra-day low on 26th September:

This is better viewed in a long-term context, whereas can be seen, the pound now trades versus the dollar at a level not seen since the mid-1980s:

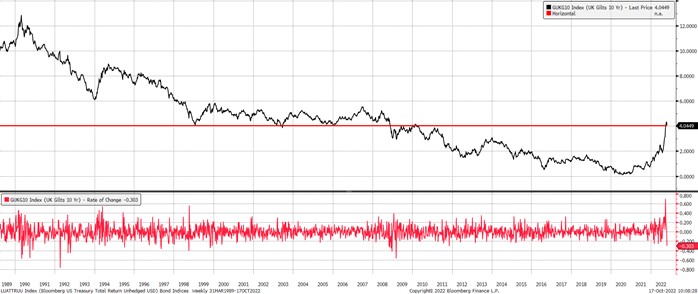

In fixed income markets, Gilts have seen truly extraordinary moves. The top panel of the chart below plots the yield of the 10-year Gilt from 1989 onwards, with the red horizontal line showing that today’s yield is now back to levels not seen since 2008. The bottom panel of the chart shows the rate of change of the 10-year Gilt yield, where it can clearly be seen that at no point in this data series’ history have larger short-term shifts been seen:

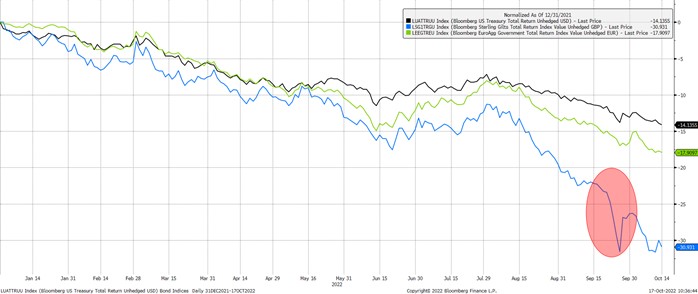

That on its own is dramatic enough but given the very low starting point of this recent upwards move in yields, and therefore with a very high level of duration, or interest rate risk, baked in, when translating the change in yields to price movements, we can see that substantial losses have occurred, per the next chart.

This shows the broad Gilt index in blue through 2022, with equivalent government bond indices for the US (black) and Europe (green) also plotted for context. Despite the recovery since seen due to the Bank of England’s intervention, Gilts have fallen by nearly 31%, with much of that loss suffered in a very short space of time:

As mentioned above, the BoE were forced to step back into the Gilt market to ensure its stability, committing to buying up to £10bn of Gilts and index-linked Gilts every day until 14th October, in a return to emergency quantitative easing in all but name.

This action was required as parts of the UK defined benefit pension market saw highly stressed conditions relating to their holdings of long-dated Gilts; without this intervention they faced a potentially acute funding crisis related to the very sharp price falls illustrated above.

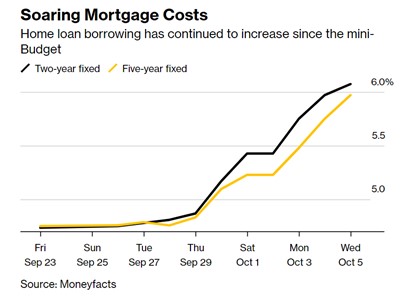

In terms of further real-world impacts, we have already observed that mortgage rates are very sharply rising due to the rise in government bond yields, with a 2-year fixed rate mortgage now costing more than 6% for the first time since November 2008, and a 5-year fixed rate mortgage nearing the 6% mark.

Similar moves have been seen in the corporate lending space, with companies looking to issue new debt facing much higher rates of repayment than just a month ago. While the BoE’s intervention has calmed the worst of the market’s nerves, these higher rates will have a negative impact on future demand:

Events have been especially fluid over the past few weeks. The extent of the market moves above and the pressure this placed on the new government led first to a U-turn on the elimination of the top rate of income tax, followed closely by the sacking of Chancellor Kwasi Kwarteng on 14th October, and the appointment of Jeremy Hunt in his place.

Then, on 17th October, an astonishing emergency statement was made by the new Chancellor (the fourth in 2022), which essentially reversed all of the planned measures introduced by the Prime Minister in September, bar two: the abolition of the health & social care levy (cut to National Insurance) and the cuts to stamp duty.

Hunt announced that corporation tax would now be rising in April 2023, the basic rate of income tax would not be falling to 19%, and would stay at 20% ‘indefinitely’, and, most significantly for consumers, that the energy price guarantee would now only run in its current, open-ended form until April 2023. After this point, a new scheme would be put in place to better target those who need the support.

Financial markets’ reaction to this series of U-turns, culminating in the near-complete reversal of the mini-budget, has been positive, with Gilt yields moving down from their peaks, and the pound making something of a recovery against other major currencies.

The road ahead remains uncertain however, with plans still needing to be announced on identifying deliverable spending cuts, and with consumers and businesses now potentially exposed again to extremely high energy prices next year assuming no change in circumstances in energy markets or a resolution in eastern Europe.

Politically the UK’s future is more uncertain, with the credibility hit to the UK and its assets undeniably large. Shockwaves from the internal fallout will spread far from here and may raise questions about the long-term viability of the government.

It has already been suggested that Prime Minister Liz Truss is now a lame duck after just 40 days in power, with others waiting in the wings to take control. Should this happen, we suspect it may just raise more questions – can the UK be led by another unelected leader, or should there be a general election?

We expect there will be more twists and turns in the weeks to come, but for now we certainly welcome the hint of stability in the pound and Gilt yields that we currently see on our screens. As always, though, the need for portfolios to be well diversified is absolutely critical to avoid any over-exposure to one particular market.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: