Savings & investment

Harry Scargill

“Sell in May and go away” is one of the oldest sayings in the investment world.

But is it really a good idea?

Here we look at why following this maxim may cost you money instead of making it.

“Sell in May and go away” has been part of market folklore for the best part of three centuries.

The full version – “Sell in May and don’t come back until St Leger’s Day” – dates back to a time when London’s bankers, brokers and aristocrats would shut up shop in May, head to their country estates for the summer, and return to the markets only after the famous horse race at Doncaster in September.

Trading volumes really did thin out, and a seasonal pattern of weaker summer returns became part of investing lore.

This idea then stuck around.

Academic work from Bouman and Jacobsen’s 2002 study in the American Economic Review, examined data from 37 countries and confirmed that in many global markets, returns between November and April have, on average, been higher than those between May and October – a pattern the authors found in UK data going back as far as 1694.

So the seasonal effect is real, but, as we will see, the practical lesson investors draw from it is usually the wrong one – and times have changed.

Today’s markets look nothing like the time that gave us the rhyme.

Trading is global, electronic and continuous; corporate earnings, central bank decisions and major economic news arrive throughout the year; and the average investor is a long-term saver building a pension, not a banker decamping to a country house.

Crucially, even where a small seasonal pattern survives in the average, the gap is far too narrow to overcome the cost of being out of the market when summers turn out to see strong returns.

Research from American Century Investments, published in April 2026, puts this in numbers that make it a little easier to understand.

Looking at 50 years of S&P 500 data from 1976 to the end of 2025, the study shows that a $1,000 investment left alone the whole time would have grown to roughly $294,800.

The same $1,000 switched out of the market each May and back in each November would have grown to just $46,400 – less than a sixth of the total secured by staying invested.

This is quite a staggering difference in returns that really shows the weakness of blindly following this phrase.

If any year was made to test the “Sell in May” theory, it was 2025.

Markets started that year on somewhat shaky ground. The Trump administration’s “reciprocal” tariffs sent the S&P 500 down nearly 19% from its February peak by early April, and headlines were dominated by fears of a global growth shock, sticky inflation and a brewing trade war.

For an investor watching the news on the morning of 1 May, the temptation to follow the adage and step away might have been understandable.

It would also have been very costly.

From the end of April through to the S&P 500’s new all-time high on Christmas Eve, the index, in GBP, returned 24%, and finished the full year up 9.8% – a strong return even after meaningful sterling appreciation against the dollar.

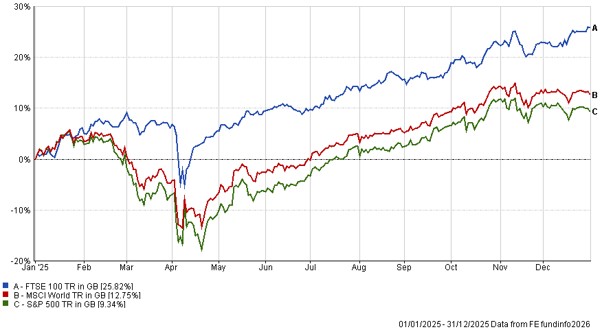

The below chart shows the returns over the full year, along with the volatility we saw in March and April.

In sterling, the MSCI World rose 13.2% and the FTSE 100 25.8%. The summer months – the very period the saying tells investors to avoid – carried a lot of the returns that year.

The table below shows total returns in GBP from 30 April to year-end for the three major indices, across four recent years that all had reasons to be nervous in the spring.

| Year | S&P 500 | FTSE 100 | MSCI World |

| 2020 | +20.4% | +11.8% | +22.5% |

| 2023 | +14.1% | +0.8% | +11.7% |

| 2024 | +17.9% | +2.7% | +13.5% |

| 2025 | +23.1% | +19.4% | +21.7% |

Each of these years had a clear excuse to head for the exit in May: a pandemic in 2020; lingering inflation and recession fears in 2023; election uncertainty and high valuations in 2024; tariff shocks and geopolitics in 2025.

In each case, every one of the three indices delivered a positive return from 30 April to year-end – and in most cases a meaningful one.

An investor who sold in May and waited would have missed real returns in every year shown.

None of this is to suggest that markets only ever go up, or that volatility through the summer should be ignored.

Drawdowns happen, sometimes sharply, and a well-constructed portfolio should already reflect a sensible balance between growth assets and diversifiers.

But the lesson of the last decade, and emphatically of 2025, is that the cost of being wrong on a market-timing call has been far greater than the cost of riding out the noise.

The best days in markets tend to cluster around the worst, and missing only a handful of them has historically taken a heavy toll on long-term returns.

A portfolio spread across regions, sectors and asset classes reduces the temptation, and the need, to react to short-term headlines.

Active rebalancing within a clear strategic framework – not wholesale switches in and out of the market – is what tends to help compound wealth over time.

Catchy as it is, “sell in May and go away” belongs to a different era.

The investors who have done best in recent years have been those who tuned out the seasonal noise, stayed broadly invested in line with their long-term plan, and let their portfolios do the work they were designed to do.

An expert financial adviser can help you to decide on an investment plan, taking into account your circumstances and your approach to investment risk.

They can also help you to stay focused on your financial goals rather than reacting to short-term or seasonal market movements.

Get in touch with one of our advisers today to find out more.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

The phrase refers to an old investment strategy where investors sell shares in May and return to the market later in the year, traditionally around September.

While the seasonal trend has existed historically, modern markets are far more global and continuous. Many investors who followed the strategy in recent years would have missed strong market gains.

Historical data generally shows that long-term investors who stay invested tend to outperform those who frequently move in and out of the market.

Remaining invested allows investors to benefit from compounding growth and avoid missing the market’s strongest recovery periods, which often occur unexpectedly.

Selling during market downturns can lock in losses and increase the risk of missing rebounds that may significantly boost long-term returns.

“Timing the market” involves trying to predict short-term movements, while “time in the market” focuses on long-term participation and compounding growth.

Diversification spreads investments across different regions, sectors and asset classes, helping reduce overall portfolio risk and reliance on any single market event.

Rather than making reactive decisions, investors are often better served by following a long-term investment plan aligned with their goals and risk tolerance.

Yes. A financial adviser can help investors build a suitable portfolio, manage risk and stay focused on long-term objectives during uncertain market periods.

For further information, please contact:

Savings & investment

Savings & investment

Savings & investment

Savings & investment

Savings & investment

Savings & investment

For further information, please contact: