Savings & investment

Imogen Hambly

What is the outlook like for investors in the year ahead?

Here we take a look at some of the main themes, key markets and investment drivers for 2026 – and how these could affect your financial plans.

As we look ahead to 2026, several themes remain front of mind for investors including:

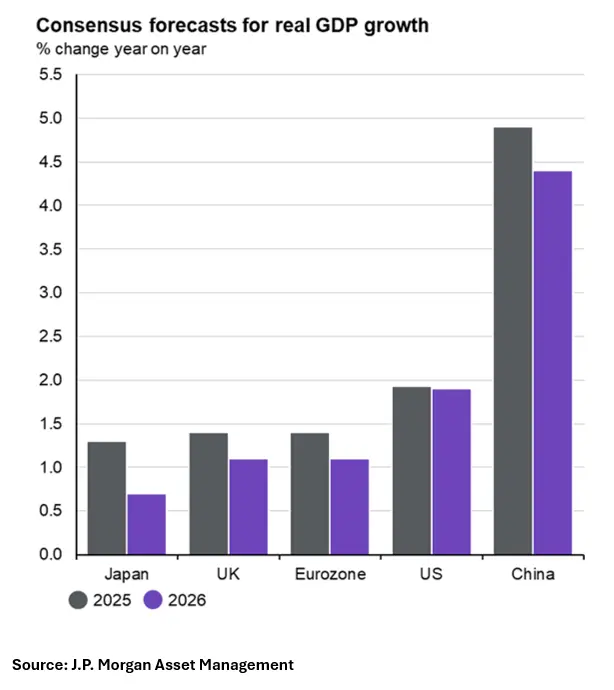

At a regional level, consensus expectations continue to favour the United States, where GDP growth is forecast to remain resilient, while Europe and other developed markets face more subdued prospects.

Emerging markets, meanwhile, are expected to benefit from more supportive duration dynamics, underpinned by a weaker US dollar.

Despite the powerful rally in the “Magnificent Seven” technology stocks that dominated much of 2025, broader US equity market returns were comparatively subdued, lagging several other major regions as investors became increasingly alert to the risks of concentrated market leadership and elevated valuations.

Nevertheless, US GDP (Gross Domestic Product) growth has held up well and remains at the forefront of developed market growth expectations heading into 2026.

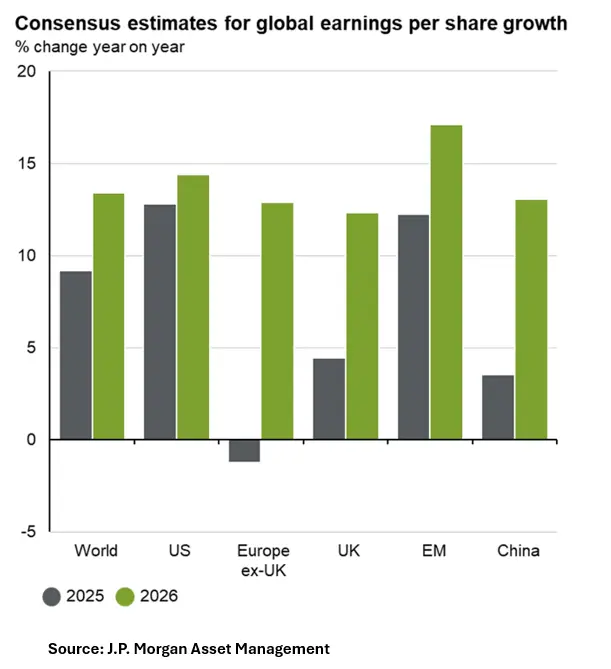

Corporate fundamentals continue to provide solid support, with more than 80% of S&P 500 companies beating earnings expectations in the third quarter, and forward guidance across both the technology sector and the wider market pointing to sustained profit growth.

Furthermore, corporate investment is expected to remain robust, underpinned by tax incentives and a more accommodative regulatory backdrop for the banking sector, which should support lending activity and credit growth.

While labour markets are showing signs of gradual cooling, productivity per worker continues to improve – a trend likely to persist as companies increasingly integrate Artificial Intelligence into business operations.

Against this backdrop, the Federal Reserve is widely expected to continue easing policy, albeit at a measured pace given lingering inflationary pressures. A steeper yield curve is therefore anticipated, creating a constructive environment for risk assets, particularly equities and high-quality corporate bonds.

Across Europe, equities demonstrated notable resilience through 2025, particularly in the latter months, supported by limited exposure to the most highly valued technology stocks and renewed strength across luxury goods, select industrials, and consumer-facing sectors.

While economic activity across the region remains subdued – most notably within Germany’s industrial sector, where output data continues to signal underlying weakness – stabilising energy prices and targeted fiscal stimulus have helped to cushion market returns.

The European Central Bank faces a challenging policy backdrop. Although inflation has continued to moderate, it remains above target, with easing core inflation offset by persistently elevated services inflation.

This dynamic complicates the outlook for monetary policy and suggests that any further easing is likely to be measured.

However, valuation differentials between European and US equities have continued to widen, presenting potential opportunities for selective investors.

Companies with strong balance sheets, durable cash flows, and pricing power may be well positioned to benefit as markets look beyond near-term growth challenges.

UK equities delivered mixed performance through 2025.

Large-cap stocks were relatively resilient, supported by steady global growth and strength across energy and materials, while mid- and small-cap equities lagged as persistent concerns over domestic growth, sticky inflation, and an uncertain fiscal backdrop weighed on sentiment.

The Bank of England has signalled an increasing openness to easing policy, which could help alleviate pressure on more interest-rate-sensitive areas of the market.

That said, the outlook remains finely balanced, with inflation proving stubborn and consumer confidence subdued.

As with our view across continental Europe, we believe a selective investment approach is well suited to the year ahead, focusing on companies with strong balance sheets, robust cash generation, and exposure to global growth drivers rather than relying solely on domestic demand.

Emerging markets face a mixed outlook. Continued US dollar weakness has supported positive earnings surprises, helping to underpin equity market performance through 2025.

However, renewed concerns around the pace of China’s recovery, alongside heightened volatility in technology-exposed markets such as South Korea and Taiwan, remain notable headwinds moving forward.

In China, fiscal stimulus is expected to provide a degree of economic stability, though policymakers appear focused on maintaining balance rather than driving aggressive expansion. This more measured approach may weigh on regional GDP growth expectations as the year progresses.

Overall, continued US dollar weakness should continue creating more favourable duration dynamics and support earnings growth across emerging markets, benefiting both equity and fixed income assets.

While markets with significant exposure to the global technology cycle may remain more volatile, we view the broader emerging market outlook as constructive.

Japanese equities have moderated following several months of strong gains, which were underpinned by ongoing corporate governance reforms and a persistently competitive yen.

Toward the end of 2025, however, rising inflationary pressures and a flare-up in geopolitical tensions between Japan and China contributed to a more cautious, risk-off tone across the market.

Despite this near-term pause, the structural tailwinds supporting Japan remain firmly in place.

Continued improvements in corporate governance and a stronger focus on shareholder returns provide a constructive long-term backdrop, although we remain mindful that both domestic developments and external geopolitical factors may continue to drive bouts of volatility.

Moderating interest rates and resilient corporate fundamentals provided a supportive backdrop for fixed income markets throughout 2025, a theme that we expect to carry into the year ahead.

Bond yields are anticipated to trend lower in 2026, offering an important tailwind for risk assets more broadly.

Softer inflation readings across the US, eurozone, and UK have underpinned rallies in sovereign bonds, as central banks have shifted policy rates lower, with guidance from both the Federal Reserve and the Bank of England signalling further easing ahead.

At a global level, corporate bonds are well positioned to continue outperforming government bonds, supported by strong balance sheets and contained default expectations.

While credit spreads may tighten further, gains are likely to be more incremental, with investors remaining selective amid an uneven and evolving macroeconomic landscape.

Overall, fixed income markets are expected to provide a valuable counterbalance to equity risk, with high-quality bonds retaining a key role as both a source of steady income and a stabilising force within multi-asset portfolios.

While artificial intelligence (AI) stocks have experienced a remarkable rally throughout 2025 – raising concerns of an AI-driven bubble – AI remains a genuine structural growth theme, supporting productivity gains and driving leadership across global markets.

Adoption is set to accelerate further, with substantial investment in technology and infrastructure continuing across both developed and emerging markets, generating ripple effects in labour markets.

Although concentration risk and elevated valuations are considerations, the major AI players continue to deliver strong revenue and margin growth, leaving many investors confident in the potential for continued upside.

However, AI is unlikely to be the sole driver of market returns in 2026.

Quality stocks – those with a history of stable earnings, high profitability, and low leverage – are expected to reassert their role in protecting portfolios during periods of volatility, while sectors such as pharmaceuticals, financials, and industrials appear particularly attractive, offering more modest valuations alongside steady earnings growth.

The global growth narrative for 2026 is evolving in a way that underscores regional divergence.

While the US and China are expected to deliver above-trend growth, Europe and other developed markets remain constrained by structural headwinds, including muted domestic demand and competitive export pressures.

Emerging markets, by contrast, stand to benefit from a combination of policy flexibility, supportive demographics, and a weaker US dollar.

This uneven backdrop creates both opportunities and risks, emphasising the importance of active asset allocation and a focus on both sectoral and regional diversification to capture growth potential while managing volatility.

Although inflation has moderated from its peaks, the path ahead remains complex.

Central banks are expected to maintain a cautious stance, balancing the need to support growth with the imperative to contain residual inflationary pressures.

In the US, the Federal Reserve is likely to continue cutting rates, but not aggressively, as policymakers remain wary of reigniting price pressures.

In the UK, rate cuts may be slower and more conditional, given persistent inflation.

For investors, this environment favours active selection across bond markets, while maintaining hedges against inflation through real assets and commodities.

The interplay between disinflation trends and policy caution will be a defining feature of fixed income markets in 2026.

We think 2026 offers opportunities for investors willing to navigate complexity.

Consensus supports risk assets, but divergences in regional and thematic views underscore the importance of active management and diversification.

Consulting a financial adviser can help you decide what investments could help you towards your financial goals in 2026, whether that’s accumulating funds for retirement or investing for growth.

To start your investment journey – or if you’re thinking of changing course – talk to an adviser today.

| Match me to an adviser | Subscribe to receive updates |

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

For further information, please contact:

For further information, please contact: