Financial crime continues to evolve. While many people are familiar with scams such as phishing emails or cold calls, criminals are now using more advanced and convincing methods to exploit trust, technology and human behaviour.

At Fairstone, protecting our clients, their identities and their investments is a priority.

This article explains the most common types of financial scam affecting UK consumers today, how scam tactics are becoming more sophisticated, and what we do to help keep you safe.

We also outline what you should – and shouldn’t – expect from us when it comes to how we work with you.

Financial scams are no longer limited to obvious warning signs like poor spelling or generic messages. Criminals are increasingly combining social engineering with advanced technology to make scams more realistic and harder to detect.

One rapidly growing trend is the use of AI‑generated or “deepfake” voice messages, commonly sent via WhatsApp and other messaging platforms.

In these scams, criminals clone the voice of someone you trust, such as a family member, using short audio clips taken from social media videos, voicemail greetings or other publicly available recordings. These voice messages are then used to create highly believable emergency scenarios requiring urgent financial assistance.

Recent UK cases show families being targeted with WhatsApp messages that include convincing voice notes, often claiming a phone has been lost and money needs to be transferred urgently. These scams have resulted in significant losses and are becoming more common as the technology becomes cheaper and easier to access.

Deepfake audio is not limited to family impersonation. It has also been used to impersonate professionals, senior leaders and trusted contacts, which means relying on a familiar voice alone is no longer a reliable way to verify legitimacy.

As scam methods become more advanced, the importance of taking time, verifying requests independently and contacting a trusted adviser has never been greater.

Fairstone would never rely solely on a voice message, unexpected call or messaging app to request financial action.

We apply verification steps and use confirmed contact details before acting on sensitive instructions.

If you receive an unexpected message, voice note or call about financial issues that causes concern, please pause and contact your adviser straight away before taking any action.

Banking fraud often involves criminals posing as banks or financial institutions.

You may be contacted unexpectedly and told there is an issue with your account that requires urgent action, such as transferring funds or confirming details.

Typical warning signs include pressure to:

Fairstone would not pressure you to move money or act urgently following an unexpected banking‑related request.

Any genuine financial instruction would follow clear verification steps and allow time for consideration.

If in doubt, contact your adviser directly before taking any action.

Card fraud occurs when debit or credit card details are used without your permission.

This may happen following phishing emails, data breaches or insecure online transactions.

Unexpected payments or card declines should always be investigated promptly.

If card fraud may affect your broader financial position, your adviser will take time to understand the situation before any financial decisions are made.

If you are unsure how an incident affects your finances, contact your adviser.

Impersonation scams involve criminals pretending to be trusted organisations or individuals, including banks, advisers, government bodies or professionals. Increasingly, these scams may include:

Fairstone advisers will always clearly identify themselves and follow agreed security procedures. We will not rush you or ask you to bypass verification checks.

If someone claims to represent Fairstone and something does not feel right, pause and contact your adviser using known contact details.

Romance scams develop over time through dating apps or social media. Criminals build emotional trust before requesting money, financial help or investment support.

These scams are particularly effective because they rely on personal connection rather than technical fraud.

If a personal relationship starts to influence financial decisions, your adviser can help you pause and assess the situation objectively.

If in doubt, speak to your adviser before sending money or making commitments.

Online scams include phishing emails, fake websites and fraudulent messages designed to capture login details or personal information.

These messages often appear realistic and may include links or attachments.

Fairstone would never ask you to provide sensitive information or approve financial instructions via unexpected online messages. High‑risk requests are always subject to additional verification.

If you receive an online request that concerns you, contact your adviser before responding.

Investment scams typically promise high or guaranteed returns with little risk and may be presented as limited‑time opportunities.

Pressure and urgency are common tactics.

Fairstone advisers will never recommend investments without appropriate due diligence, suitability checks and time for consideration.

If approached about an investment outside your usual adviser relationship, contact your adviser before proceeding.

Identity theft occurs when personal information is used to open accounts or commit fraud in your name.

This often follows phishing scams or compromised email accounts.

Fairstone always carries out identity checks before acting on instructions. If you believe your identity may have been compromised, your adviser can support you in considering next steps.

If in doubt, contact your adviser promptly.

Protecting your personal and financial information is extremely important to us. We have clear steps in place to make sure we are always speaking to the right person and to reduce the risk of fraud or impersonation.

When we speak to you by phone about personal, financial or investment matters, we will ask you to confirm security information before continuing.

We treat emails requesting withdrawals, investment changes or bank detail updates as high risk.

We will only proceed once identity has been confirmed using verified contact details.

We may sometimes communicate via Microsoft Teams. Where there is any uncertainty about identity, we will pause and reconnect using trusted details.

If you receive a communication claiming to be from Fairstone and are unsure, always contact us directly using the details on our website or official documents.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

Common financial scams include banking fraud, impersonation scams, investment scams, online scams, identity theft and, increasingly, AI‑enabled scams such as deepfake voice messages.

Pause before responding, question unexpected requests, avoid acting under pressure and verify requests using trusted contact details. If in doubt, contact your adviser.

Do not act immediately. Verify the request independently using a known phone number and speak to your adviser before sending money. AI voice scams are becoming increasingly convincing.

No. Fairstone will not rush you or pressure you into moving money without proper checks and confirmation.

If you are ever unsure, your first step should be to contact your Fairstone adviser directly.

We pride ourselves on providing face‑to‑face advice, not call‑centre interactions. With over 50 locations across the UK and more than 400 advisers nationwide, a face‑to‑face meeting is always available should you want to discuss a request in person.

If something does not feel right, pause and speak to your adviser before taking any action.

The last couple of weeks have delivered a steady stream of unsettling headlines from the Middle East.

Oil prices spiked, some equity markets fell, and commentators rushed to predict what happens next.

It’s natural to feel uneasy in moments like this. But for long‑term investors, the best response is usually the most straightforward: keep calm, stay diversified, and stick to the plan you built around your goals.

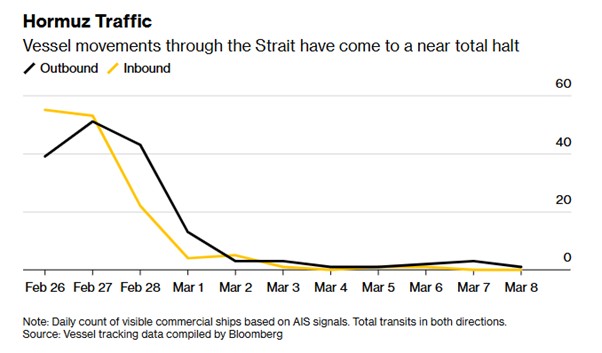

Recent military escalation in and around Iran has disrupted shipping through the Strait of Hormuz, a narrow channel that normally carries a large share of the world’s oil and gas:

When those flows look threatened, energy prices can jump quickly and knock confidence across wider markets.

We’ve seen exactly that pattern: crude oil briefly pushed into triple‑digit territory before easing back as talk of strategic stockpile releases and naval escorts helped steady nerves.

Equity markets sold off at first, then showed signs of resilience as energy prices backed off their highs.

In short, it has been a fast‑moving situation – but not an unfamiliar one for markets.

Diplomacy continues in the background and policy responses are on the table.

Authorities have discussed reserve releases to cushion supply, and any reopening of shipping lanes would help prices normalise.

The timing is uncertain, it remains a fast-moving situation and headlines may stay volatile for a while yet.

That said, markets often adjust faster than the news flow, especially when investors can see a path to stabilisation.

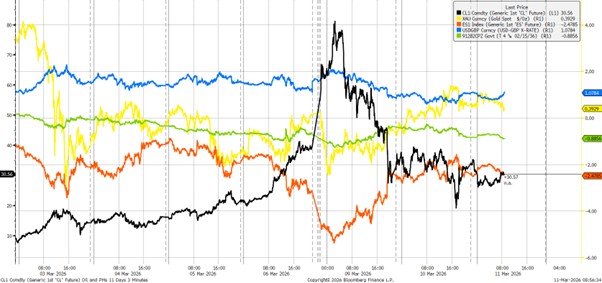

Oil jumped (black line in the chart below) as shipping slowed, before retracing a good portion of the move when signs of policy support and limited tanker escorts emerged. Large daily swings have been common.

The initial “risk‑off” reaction hit most equity regions. Energy companies outperformed on the way up, then gave back some gains as crude eased.

US equities (orange line in the chart below) have been relatively resilient versus other regions as the US is seen as less exposed to the volatility.

Government bonds (10-year US Treasuries in green line), which often rally when shares fall, were tugged in two directions – by safe‑haven demand on the one hand and by renewed inflation concerns on the other (higher oil can keep inflation sticky). That’s one reason returns have varied by market and maturity.

The US dollar firmed as investors sought safety, which matters for UK investors holding overseas assets (USD/GBP in blue line).

Gold was volatile (yellow line)—useful as a diversifier over time, but not a guarantee of gains on every risk‑off day.

As oil pulled back from its peak, market anxiety measures cooled from their initial spike, reminding us that conditions can change very quickly when policy signals improve.

None of this is to minimise events; it’s to put them in context.

Markets have navigated many geopolitical shocks over the decades, and while the path is rarely smooth, the longer‑term pattern has been one of recovery as fundamentals reassert themselves.

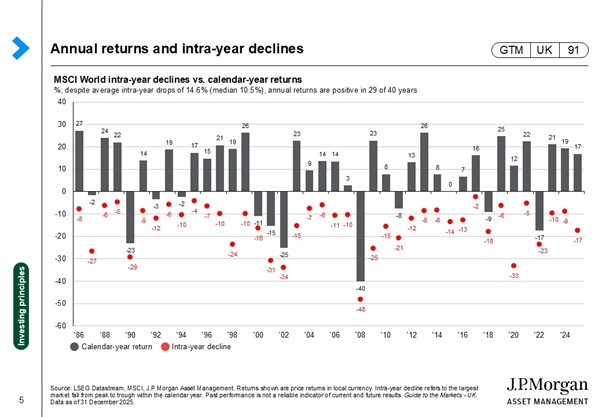

Every year experiences pullbacks. A long-running analysis by J.P. Morgan Asset Management (see chart below) shows that, despite an average intra‑year decline of roughly 15% in global equities (red dots in the chart below), calendar‑year returns (grey bars) have still been positive most of the time.

In other words, setbacks are common, recoveries are too.

Selling after markets fall often locks in losses and risks missing the recovery.

Fund‑flow data show investors tend to withdraw money near market troughs – exactly when patience is most valuable.

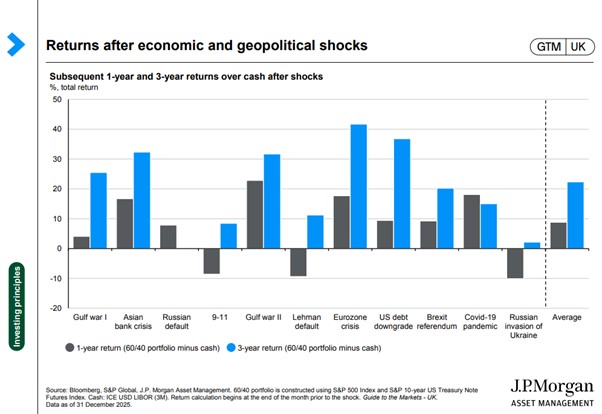

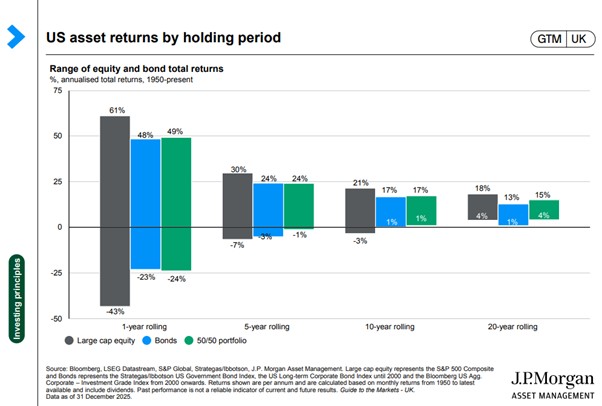

More importantly for today’s environment, the chart below shows that a simple 60/40 mix of shares and bonds has beaten cash after past geopolitical and economic shocks more than 70% of the time over the subsequent year – and every time over the subsequent three years in the sample J.P. Morgan studied:

The longer you stay invested, the lower the historical odds of losing money—particularly in a balanced portfolio.

Combining time, compounding and regular reinvestment has been a powerful driver of long‑term outcomes as the final chart below shows; while over short time periods the range of returns can be wide and sometimes negative, the longer the investment time period the more predictably positive returns become.

Whilst the current time is unsettling for investors, it is important to remember that the fundamental principles of investing remain the same.

Your portfolio was built around your personal objectives and time horizon.

Short‑term market moves – especially those driven by geopolitics – don’t usually warrant wholesale changes to a long‑term plan.

A balanced approach helps cushion the journey and has historically rewarded patient investors, including through past crises.

Cash has a role for near‑term needs and as a stabiliser, but moving large amounts out of markets after shocks typically hurts long‑term results – and inflation quietly chips away at purchasing power.

Rather than making big directional calls, periodic rebalancing back to your agreed mix naturally trims assets that have risen and adds to those that have fallen, keeping risk aligned with your goals.

We are monitoring developments daily – including energy market dynamics and any policy responses – and we’ll adjust where needed within the discipline of your strategy.

If your circumstances change, please let us know so we can reflect that in your plan.

Get in touch with an adviser to discuss your current situation, any concerns you have or adjustments you’re thinking about making.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

At Fairstone, we see International Women’s Day on March 8 as an opportunity to listen, reflect and celebrate.

This year’s theme, “Give to Gain”, is a powerful reminder that when we share our knowledge, uplift one another and create space for different voices, we all grow stronger. Progress happens when we invest in others, and in doing so, move forward together.

We’re proud to share thoughts from women across our organisation, highlighting their experiences, insights and what International Women’s Day means to them.

Their voices reinforce the importance of opportunity, equity and empowerment, in our workplace and beyond.

“I joined Fairstone on 16 May 2012 and I have been here as a Self-Employed Financial Adviser ever since.

My role is to look after and advise clients. I love the problem solving of that and meeting people. Having worked in such a male-dominated career normally being the only female financial adviser, I forgot to see myself as that and thought of myself as just an adviser.

Joining Fairstone, I learned that female clients love to have female financial advisers. It turns out that many get ignored by male advisers in some firms. For me, this seemed to be an untapped market. I have been my most successful at Fairstone and won an award at the annual conference in 2018 for customer service.

For young females wondering whether to pursue a career as an IFA, I would say please do – although there are more of us now, we are still under-represented.

International Women’s Day is interesting for me. If you had asked me what I thought about this 10 years ago I would have said, based on my experience, that I thought things were relatively straightforward for women and I think that was from my determination that made me succeed.

Reflecting on this now, I think it is so important to recognise how different things are for women in the workplace and what others have sacrificed in order for us to have the opportunities that we have today. IWD for me is a time to reflect on all those amazing women.

If I could pay it forward to at least one other woman before I retire, that would be my dream.”

“I’m an Independent Financial Adviser at Fairstone and relatively new to the firm. It was the cultural fit that led me here, and the supportive and encouraging environment that has allowed it to be such an enjoyable and enriching experience so far.

Previously, I was a self-employed adviser within a large network. While that model offered independence, it could also feel quite isolating a lot of the time without the day-to-day collaboration and shared energy of a team environment.

I absolutely feel supported as a woman at Fairstone. The fact that Fairstone is a safe space that encourages growth and development – and provides the utmost support, regardless of who you are, is evident.

As a woman, I still have a voice, and this hasn’t always been the case at other firms in the past.

I think the important thing to highlight is that the support here at Fairstone is universal across the board, regardless of whether you are a man or a woman.”

“What excites me about the future of women in wealth management is that women are not just accepted in the industry anymore, they’re actually needed.

The Great Wealth Transfer is a prime example of this, as is the fact that there are now more women owning and leading businesses than ever before.

I’m not saying that all women only want to work with women, but women being available in client-facing roles is so important and it’s so great that this is being recognised.

The number of advisers who are women is unfortunately still low but it’s clear to see that there are big pushes and attempts to change this.”

“I joined Fairstone two years ago, having started my career as a solicitor advising clients on their wills, powers of attorney, tax and trusts before moving into roles where I managed other advisers and becoming increasingly involved in the leadership of advice businesses.

As one of our three managing directors, I work as part of the senior management team and across the business to make sure we remain one of the leading independent financial advice businesses in the UK where our colleagues across the country can all play their part in making sure our clients are well looked after and have confidence in their financial future.

I’m a working mum who followed a career path through law and into financial services, in full and part-time roles, working with brilliant people throughout, so for me, visibility as a woman in this industry is about being able to encourage others into the sector, supporting them as they develop and giving them a chance to see how rewarding they could find it.

As senior leaders, we need to ensure we are an inclusive organisation that attracts and retains the best talent, that offers flexibility in part-time and full-time roles, that encourages and supports progression and which allows people to excel in their role and be proud of the role they do.

Financial services and financial planning in particular are still often perceived as male-dominated sectors, which may put women off when looking at their career options. Managing finances effectively in today’s complex world is challenging and as more women seek financial advice, we need talent and diversity within financial services that reflects our society.”

“After finishing university and spending a year in the charity sector, I started out as a paraplanner in one of Fairstone’s regional offices. After a year or so, I realised that a financial advisory role wasn’t for me, so when a vacancy came up within Fairstone’s investment management team in 2016, I applied for and got that job and I’ve been here since.

My role has grown as the company has grown – I studied for and achieved various qualifications in investment management and I’m now a CFA Charterholder and a Portfolio Manager within the Fairstone Investment Management team.

I’m the lead manager for our Pure Passive and Responsible model portfolio ranges, as well as our Irish fund range and our UK Fixed Income strategy. My role spans everything from strategy development and research to analysis and asset allocation.

Fairstone Investment Management now oversees more than £4.5bn in client assets, which I think really speaks to the strength of our investment proposition, the trust our clients place in us, and the commitment of our advisers and support teams across the UK and Ireland.

That continued growth is also reflected in the recognition the team has received, with both Fairstone Investment Director Oliver Stone and I being named in Citywire’s Top 100 Fund Selectors last year.

At the start of a career in investment management, one of the biggest challenges – particularly as a young woman – can be getting people to place their trust in you. But I think that’s something young men probably experience too.

You’re being asked to take responsibility for people’s life savings, which is a huge responsibility. That’s why building your knowledge base early is so important, both to earn that trust and to feel confident in your own decisions.

I’ve been supported really well at Fairstone throughout my career in terms of training and qualifications and that’s stood me in good stead. Once you build up that base, you get more confident in what you do and in turn that confidence and that knowledge breeds trust from both clients and colleagues.

Building up that trust is vital in investment management – if you don’t trust the knowledge and capability of the person you’re dealing with then you are not going to trust them with your money.

It’s definitely a career which I would recommend to other women. One of the things I like about my role is that, in many ways, it’s what you make of it. You never stop learning – whether that’s about politics, economics, geography or world history.

There’s always something new that’s relevant, so if you’re curious about the world and how markets interact with real world events, it’s a great career to be in.”

“I am currently the youngest manager at Fairstone in my role as Paraplanning Manager for the central team. Having wanted a role that combined finance with people, I found financial planning to be the perfect fit.

I thrive in environments that value strong interpersonal skills and my work across our national adviser group has strengthened my ability to challenge advice constructively and support new employees and firms through integration into our business model – ensuring they feel heard and supported.

I joined Fairstone straight from university as a graduate trainee paraplanner within a female-led team. Working in a male-dominated industry brings its challenges, and at times it can feel like you start on the back foot. However, as a young female professional, I feel a responsibility to push boundaries, demonstrate what is possible, and be proactive in shaping my contribution across Fairstone.

I am fortunate to have received strong support from both Fairstone and my line management, who have encouraged my professional development through qualifications, constructive challenge, and involvement in strategic working groups.

These opportunities have given me the confidence and platform to share my experience, influence senior leaders, and continue contributing meaningfully to the wider organisation.”

“I am Managing Director of Collaboration and Alignment, having recently transitioned into Fairstone’s M&A team to help support new partner firms as we accelerate our growth strategy throughout 2026. My aim is to ensure every partner firm feels connected to Fairstone’s values from day one as growth should feel connected, not complicated.

Before this, I led the advice process within Financial Planning, and that experience means I bring an in-depth understanding of Fairstone’s process, culture, and our operational heartbeat. All this knowledge feeds directly into supporting this next exciting phase.

I spent 18 years growing alongside Fairstone, joining when we were a start-up and watching us evolve into the large, national independent firm we are today. I feel genuinely honoured to have played a part in that transformation, alongside so many incredible colleagues.

I was Fairstone’s first ever employee to take maternity leave and my daughter is currently completing her work experience with us whilst finishing her Business and Finance Studies. She has quite literally grown up alongside Fairstone and watching her take her first steps in the business I love is a wonderful full-circle moment.

My biggest piece of advice to women considering a career in finance would be to not underestimate the power of being in the room.

Finance is a brilliant career for women more than people often give it credit for. The flexibility that exists today means you genuinely can build a career that works around your life, not against it.

Seek out a seat at the table. The conversations, decisions and relationships that shape your career happen there.

Look around for the senior women already doing it; they exist, and they are cheering for you.

Finally, finance is not just about numbers; it is about relationships, strategy, empathy and leadership. Women bring all that in abundance. There is absolutely space to thrive here, and the industry is stronger because of it.

Progress does not happen by chance, it happens by design. Senior leaders have both the privilege and the responsibility to be intentional about creating the conditions where women can truly thrive.

I believe it looks like this in practice: create visible pathways that make career progression transparent and tangible. Show what great looks like and how to get there because you cannot aspire to what you cannot see. Visibility of opportunity changes everything.

Sponsor, don’t just mentor. Women need leaders who will actively champion them in the rooms they are not yet in and use their influence to open doors that might otherwise stay closed. Sponsors advocate.

Invite women into new opportunities as confidence grows through exposure. Pull women into high-impact projects. Don’t wait until they feel ready as we should create the environment that gets them there.

Build inclusive cultures, not just inclusive policies. Policies matter, but culture is lived in everyday moments, whose voice is heard, who gets credit, who is encouraged to lead. The small things add up to everything.

When senior leaders are truly intentional about inclusion, pathways don’t just open, they widen and that is better for everyone.”

“As Chief People Officer, I oversee the full employee lifecycle — from attracting and recruiting talent through to development, engagement, and supporting people to grow and succeed within the organisation.

I’ve worked in HR for about 25 years, starting in generalist roles that gave me exposure to many areas of people and culture. Over time, I moved into more senior leadership positions where I’ve been able to partner closely with executives on organisational strategy, culture, and transformation.

What’s really driven my career is a passion for creating environments where people can thrive and contribute at their best. In my current role, I focus on aligning our people strategy with the business, building strong leadership, and ensuring we’re creating meaningful opportunities for employees across the organisation.

If you’re considering a career in finance, my biggest advice would be to go for it — even if you don’t feel like you meet every requirement or have everything figured out yet. Finance is a broad field with so many opportunities, and there’s space for different skills and perspectives.

I’d also encourage women to build a strong network early on. Finding mentors, asking questions, and learning from people who’ve been in the industry can really help you grow and navigate your career. Confidence is something that develops over time, so don’t be afraid to speak up, share your ideas, and take on challenges that stretch you.

I think senior leaders have a really important role to play in creating opportunities and removing barriers. One of the biggest things they can do is make sure there’s transparency around career progression — so people clearly understand what it takes to move forward.

It’s also about culture. When leaders promote an inclusive environment where different perspectives are encouraged and work–life balance is respected, it makes it easier for women – and really everyone – to see a long-term future in the organisation.”

“As an M&A Partner, I’m responsible for speaking to businesses which may be interested in our partnership and acquisition model – the DBO. I work alongside the M&A team to structure and complete deals – from the first point of engagement, through discussions, to ultimately agreeing terms.

I joined Fairstone on the Graduate Business Analyst pathway, after completing my Masters, initially joining as a Business Analyst, before being appointed M&A Associate, and now M&A Partner.

There are huge opportunities for women across the finance and wealth sector – it’s a massively personable industry and one which has seen some big shifts over the last few years.

We all know that the industry has historically been more male-dominated, however there’s been a big focus on getting more women into the industry and into senior positions, whether that’s into M&A, investment management or financial planning and wealth management.

There is a shift in more women becoming primary or higher earners, as well as a wealth transfer between generations and other factors resulting in women having an increasing share of the wealth across the country. All of this means more women need financial advice, creating a demand for more female advisers in the sector.

Unfortunately, the majority of people still ‘fall into’ this industry and don’t set out with the intention of creating a career in financial services – the more young women who can see how rewarding and lucrative the sector can be the better.

My experience within the M&A team has been nothing but supportive. I’ve always been afforded every opportunity and never felt any different to my male colleagues.

There are some great female leaders and exceptional female planners across the business to look up to as well. It’s thanks to all of those people I’ve been able to progress in my role as quickly as I have.”

“I wouldn’t say I planned to work in finance and in fact I studied fashion. So, when I applied to work at Fairstone I had no experience in the industry.

I started in case management. I really enjoyed my role and the people I worked with, and I feel like my enthusiasm and ‘can-do’ attitude at work helped me to progress to where I am now.

I am constantly eager to look for ways to progress and in doing so I have now passed mortgage exams and now have the qualifications to be a mortgage adviser.

When I started my exams and was given my first study guide, I initially thought ‘I have no idea what this means’ and thought it was going to be impossible. I think self-belief helped me to get to where I am and when I look back to where I started, I am so proud of how far I have come.

I am fortunate to sit amongst various teams at Fairstone head office and the culture is genuinely and positively diverse. I work with some amazing women and am inspired by lots of women colleagues who I have met here at Fairstone by their talent, unique perspectives and trailblazing qualities.

Not only that, I feel encouraged as a woman at Fairstone. My manager helps me to aim higher, stretch my personal professional development to set goals in areas I want to grow, and I feel 100% supported in that journey to achieving them.

When I started my career, I was invited to an external Women’s Recognition Awards event in London and was absolutely encouraged to attend to represent Fairstone.

It was exciting and empowering to go to the event and see so many accomplished and influential women in one room who were pioneers within the industry.

I met so many confident, motivated and inspiring females that day. It was a breath of fresh air to see that the stereotypical man’s world in finance has changed and is being reshaped by the growing community of women in the industry.”

The Chancellor has delivered her Spring Statement for 2026, setting out updated economic forecasts and outlining the Government’s fiscal position for the years ahead.

Since the Chancellor has chosen to restrict major Government fiscal events to one per year – the Autumn Budget – no new tax or spending changes were announced.

Instead, the Spring Statement focused on growth expectations, borrowing rules and the wider economic outlook.

The key points were:

For more information on the Spring Statement and how it could affect you, please download our comprehensive Spring Statement 2026 guide.

| Match me to an adviser | Subscribe to receive updates |

The start of the year is the best time to make plans.

With that in mind, here are some of the red letter days in the financial calendar for 2026 – and why they’re important.

If you need to file a self-assessment tax return, you have to do so by Saturday 31 January, 2026. It’s also the deadline to pay any tax owed from that return.

If you are self-employed then it is the date by which you have required to make a first payment on account. This is an advance payment towards your next tax bill, based on your previous tax liabilities.

Since payments to HMRC can take a few days, it’s always better to complete your tax return in good time for the 31st.

Will interest rates fall further? All eyes will be on the 12 noon announcement on February 5th.

While the Government has said it will stick to just one major ‘fiscal event’ for the year, the Chancellor will issue a Spring Statement on this date in March.

The Office for Budget Responsibility (OBR) is scheduled to publish its Economic and Fiscal Outlook (EFO) on the same date, although this will be will provide an interim economic update, not a full fiscal assessment.

The energy price cap for the second quarter of the year will come into effect on April 1 Day to cover the period from April 1 to 30 June.

Ofgem, the energy regulator, will announce the level of the price cap around the end of February.

Water bills, Council Tax, car tax and TV licence fees are all expected to rise from April 1 onwards.

The tax on electric vehicles will also come into effect and air passenger duty will also rise.

As announced in the November Budget, the National Living Wage will rise by 4.1% to £12.71 per hour for eligible workers aged 21 and over from April 1.

The National Minimum Wage rate for 18–20-year-olds will also increase on the same date by 8.5% to £10.85 per hour, narrowing the gap with the National Living Wage.

The National Minimum Wage for 16 to 17-year-olds and those on apprenticeships will also increase by 6% to £8 per hour.

Business owners will need to take account of these increases in their financial planning for the year.

If you’re planning to utilise your entire ISA allowance, the full £20,000 will need to have been paid into your accounts by this date.

This includes Junior ISAs, which come with a separate annual allowance of £9,000 per tax year.

It’s important to remember that the annual ISA allowance is “use it or lose it” – you cannot roll it over into the next tax year.

Anyone wanting to pay extra into their pension should also try and do this before 5 April, although you can roll any unused allowance forward into future tax years.

Most people can contribute up to £60,000 to their pension pot each tax year and benefit from tax relief.

However, for those with an annual income of more than £200,000 (including salary and income from savings and investments) it reduces to an amount between £10,000 and £60,000 if you earn over £200,000. This is called the tapered annual allowance.

April 5 is also the deadline for employers to register payroll benefits in kind for the 2026/27 tax year.

As well as the start of the new tax year, April 6 is also the date at which increases to State benefits will begin.

In the case of the ‘new’ State pension, this will rise by 4.8% to £12,547.60 a year.

New rules for Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) begin for those with income over £50,000.

This requires businesses and landlords with qualifying income to maintain digital records and update HMRC each quarter using compatible software.

From this point, when someone dies, after the first £1m of business and agricultural assets, inheritance tax will apply.

There will be 50% relief, at an effective rate of 20%. This will also apply to qualifying AIM shares, which previously fell out of your estate once you had held them for at least two years.

The tax on dividends will rise from 8.75% to 10.75% for basic rate taxpayers and 33.75% to 35.75% for higher rate taxpayers after changes were announced in the Budget.

For the 2025/2026 tax year, employers must submit their final Full Payment Submission (FPS) on or before their employees’ last payday of the tax year, which ends on 5 April 2026.

While the legal requirement is to submit the FPS on or before the payday, HMRC typically accepts the final FPS until 19 April 2026 (as this is the Employer Payment Summary (EPS) filing deadline for the previous tax year).

This is the first day that many employees can easily submit their tax returns for the previous tax year.

If you are self-employed then this is the date by which you are required to make a second payment on account for the 2024/25 tax year.

Maximum annual university tuition fees in England rise in line with inflation from £9,250 per year to £9,535 per year.

This was introduced in 2022 at a time of fast-rising petrol prices. The Budget extended it to the end of August 2026.

From this date onwards, the cut will be gradually unwound, until it disappears altogether by March 2027

These are used as part of the calculation for the Pension Triple Lock for the State Pension level from April 2027.

These are used as part of the calculation for the Pension Triple Lock for the State Pension level from April 2027, and for uprating working age and disability benefits from the same date.

Most people file Self-Assessment tax returns online but those who prefer to do it on paper will need their returns to arrive with HMRC by this date.

If timings follow 2025, November will be the month when the Chancellor outlines her Budget for 2026, although this is not guaranteed.

The final MPC meeting of 2026 to set the interest rate level going in to 2027.

To help plan your finances for the year ahead, get in touch with one of our advisers.

| Match me to an adviser | Subscribe to receive updates |

Welcome to our Budget 2025 round-up.

Here we list the key announcements with analysis from experts within Fairstone and some potential actions for you to consider.

To talk to one of our advisers today, simply call 0800 884 0840 or click here.

| Personal allowance | £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £125,140 | 40% |

| Additional rate | £125,141 and above | 45% |

“While the Government has stuck to its promise not to raise headline rates of income tax, National Insurance and VAT, freezing thresholds for three more years will drag more and more people into higher rates of tax.

“To put it in context, if income tax thresholds had risen in line with inflation from 2021, you would not start paying the higher rate of tax until you earned around £65,000. As it is, you’re going to be paying 40% on £15,000 rather than 20% and clients will feel the impact of this if they’re employed.” – Harry Sims, Chartered Financial Planner

If you are close to one of the current tax thresholds, there is a good chance that pay rises over the next four to five years could take you into a higher rate of tax.

This could affect not just your take-home pay but also access to things such as childcare vouchers, which offer up to 30 hours of free childcare per week.

If you or your partner earns over £100,000 a year, your entitlement to this, and other childcare assistance will be reduced.

Talk to an adviser about how you could divert some of your salary into pension savings, which could avoid this cliff-edge scenario, enable you to reclaim some of this childcare support, and help boost your retirement pot.

“The fact that the tax-free lump sum remained the same despite claims that the Government was looking to cut it is a perfect case in point of waiting to hear what is announced in the Budget rather than acting on rumours.” – Oliver Stone, Investment Director.

“While it won’t affect a lot of individuals by a large amount of money, it will make salary sacrifice pension schemes more expensive to run for employers and the introduction of the £2,000 ceiling could cause a potential administration issue.

“Is this the first death knell for salary sacrifice schemes as a whole?” – Mike Palmer, Corporate Financial Adviser

If you are an employee saving into a workplace pension, you now have up to three years to maximise these contributions.

Talk to an adviser on potentially restructuring how you save for your retirement, particularly taking into account the extension of the freeze on income tax thresholds.

If you are an employer operating a salary sacrifice pension scheme, this is a good opportunity to review the scheme in consultation with an adviser since its continuing operation could have quite an impact on your bottom line.

The fact that the change does not come into force until 2029 gives you breathing space to address the issue, potentially in conjunction with other employee benefits you offer.

“Using the stocks and shares ISA wrapper and tax-free allowances is more important than ever, given the reduction in the cash ISA allowance for under 65s, and the savings and dividend tax rate increases for all, potentially applicable to monies held outside ISAs.” – Andrew McErlean, Chartered Financial Planner

“There were no nasty shocks in the Budget – the market reaction has been better than for last year’s Budget – and the Stamp Duty Reserve Tax change for new IPOs is a tiny bit of positivity.” – Oliver Stone

The change to the ISA regime gives investing in a stocks and shares ISA for under-65s a clear advantage over investing in a cash ISA from a tax efficiency point of view.

While investments can go down as well as up, in her Budget speech the Chancellor said that someone who had invested £1,000 a year in an average stocks and shares ISA every year since 1999 would be £50,000 better off today than if they’d put the same money into a cash ISA.

Talk to an adviser about whether investing in a stocks and shares ISA is right for you and, if so, what level of investment risk you would be comfortable with.

“While the surcharge won’t affect the purchase market too much, valuation will be an issue. Who decides whether a property is worth £2m or more and how often will that be valued?

“The changes to taxation on property income will hit the buy to let market. It has been decreasing for quite a while and this will only make it worse.” – Emily Cadmore, Mortgage Adviser

If you currently rent a home, the increase in tax on property income could see rental levels rise further as landlords look to recoup money lost.

Talking to a financial adviser could help you to find the most competitive mortgage rates and get a good deal.

“For business owners taking dividends rather than salaries, they will be paying a bit more tax, so this is not hugely positive for SMEs on a day to day basis.” – Mike Palmer

“VCTs are often the next place higher earners might consider to maximise tax relief, once they have maximised pension contributions so for the likes of C-suite executives and top paid legal/accountancy professionals, this will impact the VCT’s attractiveness as an investment.” – Andrew McErlean

A combination of shrinking tax-free allowances and rising tax rates means that reviewing where you put your money across property, savings and investments is vital to ensure it is working as hard as possible.

An adviser will help you to look at maximising available allowances and allocating your investments in the most tax-efficient way possible in order to achieve your financial goals.

“The rise in the minimum wage is likely to be of more immediate concern to business owners than changes to the salary sacrifice regime. Even business owners who currently pay more than the minimum wage may have to consider pay rises to maintain wage differentials to their competitors.” – Mike Palmer

If you are a business owner, this is likely to add to your wage costs. Talk to an adviser about other workplace benefits which you could put in place to recruit and retain employees – such as group life assurance and private medical cover – but which will cost your business less than a larger across the board pay rise.

Get in touch today to speak to us about any of the issues raised in this article.

You can also download our comprehensive Budget 2025 guide by clicking here.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. The value of investments can go down as well as up and you may not get back the full amount you invested. Past performance is also not a reliable indicator of future performance. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

The group, which provides financial planning and wealth management to over 125,000 clients, including over 60,000 wealth clients, saw a 21% year-on-year increase in revenue and pro forma fee income to £168m in the year to the end of December 2024.

Fairstone is delivering growth through a clear strategy of organic expansion and targeted acquisitions.

The group has invested in its UK and Ireland network, establishing 12 regional hubs – 10 in the UK and two in Ireland – that are being developed into fully operational centres.

These hubs will reflect the structure of Fairstone’s head office, embedding core functions within local teams to improve delivery and support.

As well as expanding its physical footprint, Fairstone has also been developing its digital-first service, Mineral, which offers expert financial advice via video call.

Mineral is helping to address the advice gap by making professional financial advice more accessible and more affordable.

Fairstone identifies Mineral as its solution to closing the advice gap and is now embedding the service across its national infrastructure. The platform is designed to support individuals who are accumulating wealth and seeking to grow their financial position, offering accessible advice through a digital-first experience.

Fairstone’s Downstream Buy-Out (DBO) acquisition programme continues to stand out in the industry. Recent refinements have made it more appealing to firms seeking investment and operational support.

Earlier this year, the group concluded its 100th DBO partnership deal with Yorkshire-based Richardson Premier Wealth Ltd joining the programme.

In the 13 years since the DBO programme was started, it has been a major factor in Fairstone growing the amount of client assets under management (AUM) to £20bn. Enhancements to the model are expected to drive further acquisitions in the coming years.

Fairstone’s success has been underpinned by strengthening its leadership team. Last month, the group announced that former Aldermore Bank CEO Steven Cooper CBE has been appointed as its new Chief Executive Officer.

Steven, who takes up his post later this autumn, will take over as CEO from Fairstone founder Lee Hartley, who becomes Deputy Chair.

The enhanced leadership team, investment in existing operations and further strategic acquisitions will drive Fairstone’s ambition to double the size of its business to £40bn of client assets under management by the end of 2030.

David Hickey, Independent Chairman at Fairstone, said: “This is another strong set of results for Fairstone and is a tribute to the hard work, dedication and determination of our excellent team.

“With £20bn of client assets under management, our continued growth reflects the ongoing success of our client-focused approach, providing chartered, trusted and independent advice at every life stage.

“The announcement of our new CEO, Steven Cooper CBE, and the signing of our 100th Downstream Buy-Out deal this year, makes us ideally placed to scale further across the UK and Ireland.

“We have our sights firmly set on helping many more people make confident, informed financial decisions about their future as we target £40bn of client assets under management by the end of 2030.

“Fairstone continues to be recognised as a trusted, independent, and chartered financial advice firm, committed to delivering high-quality service across every stage of the client journey.

“With over 14,000 verified reviews on Trustpilot and a satisfaction rating of 98%, our reputation is built on consistent client outcomes and a strong focus on professional standards.”

From missed call scams to tax scams, inheritance scams to HMRC scams, the number and frequency of financial services scams continue to be on the rise.

In this article, we look at some of the most common scams, how to stay safe and what to watch out for.

At its most basic level, a scam is something which appears at first glance to be legitimate but is in fact a way to trick people out of money or personal details which can then be used to steal their money.

With advances in technology, these scams have become increasingly sophisticated, harder to identify and more difficult to avoid.

Scammers use a range of different media from phone calls to messaging apps to target potential victims.

They also employ time pressures such as fake deadlines to encourage people to act before thinking.

Scams can take many forms – here are some of the most common to watch out for:

This is where scammers pose as representatives from legitimate organisations like the Financial Conduct Authority (FCA), banks, or government bodies to gain trust and access sensitive information.

They often send official-looking emails complete with logos and contact details in order to fool the recipient.

FCA scams in particular are becoming more prevalent – the authority received almost 5,000 fake FCA scam reports in the first half of 2025.

One of the most FCA scams to watch out for is fraudsters claiming the FCA has recovered funds from a cryptocurrency wallet opened illegally in the potential victim’s name.

Another FCA scam sees fraudsters claiming a County Court Judgment has been taken out against a potential victim who then needs to pay the FCA the monies owed.

Fraudsters can also pose as representatives of HMRC in an effort to carry out tax scams.

One such common tax scam is an HMRC email offering either a tax refund or requiring the payment of additional tax.

Investment opportunities that seem too good to be true invariably are.

Investment scams commonly offer high returns, guaranteed returns or a combination of the two.

Fraudulent investments often involve overseas territories or property investments with an alluring brochure.

Scam cryptocurrency investments are also on the rise as fraudsters use new technology to convince people to part with their money.

Fraudsters also use fake endorsements from well-known business people or TV personalities as a way of scamming victims. MoneySaving Expert founder Martin Lewis consistently issues scam warnings, most recently highlighting deepfake AI videos promoting fake investment schemes and cryptocurrency. He also calls out fake adverts, cold calling, and imposters claiming to work for him.

This is a common tactic used in financial services scams where people receive emails apparently from a trusted source. This can include from people at your workplace or from people you know.

These phishing emails prompt the victim to click on a link and enter login details or personal information.

Fraudsters also use phishing in apps and social media platforms. Here they ask for login details to access your account to read a story or look at a picture.

This scam is similar to phishing, but this time, fraudsters use phone calls to try to extract personal details or convince you to transfer money.

Common vishing scams include messages claiming the unauthorised use of bank or credit cards for Amazon purchases, voicemail scams and missed call scams.

Other financial services scams which use vishing include fraudsters posing as representatives from financial institutions offering access to new investments or savings accounts. It is also common for fraudsters to alert you to a fake fraud and ask you to move money to a different account “for safety”.

Vishing scammers can also pose as representatives of government bodies and law enforcement agencies.

This is a particularly unpleasant form of scam where fraudsters target a vulnerable person and build trust over time.

A fraudster will not ask for money or personal details straight away but will work to gain the trust of the potential scam victim.

Only when this has happened will the fraudster make their move and carry out their scam.

This is known as ‘pig butchering’ as it likens the process to a pig being fattened up prior to being butchered.

Pig butchering scams rely on a relationship being built up so they often take place in arenas like dating apps or websites.

As well as losing money, victims of these scams often feel they have lost valuable relationships as well.

While fraudsters are becoming more sophisticated in the way they target victims, there are some useful rules you can follow to help combat scams.

Always take a moment to stop, think and challenge any suspicious requests.

Legitimate business representatives will not be offended or put off if you challenge what they ask for. Fraudsters may move on to the next potential victim.

If you’ve been targeted, always contact the relevant authorities so they can trace the fraudster and warn others.

If someone urges you to complete something quickly or tries to introduce other time pressures, that can be a sign of a scam. Ask why there is such a need for speed.

In a similar vein, be sceptical of investment ‘opportunities’ with high returns and a very limited time to ‘take advantage of’.

If you’re contacted unexpectedly by a financial firm, do not use the contact information they provide. Instead, find their official contact details on the FCA website or the Firm Checker and get in touch directly.

It’s also a good idea to carefully check email and website addresses. Fraudsters often use addresses that look convincing but have one letter out of place or an unusual ending such as ‘fcaonline’ or ‘fcagroup’.

It is really important to report any suspected financial scams to Action Fraud (the National Fraud & Cyber Crime Reporting Centre) and the FCA, as this helps them warn others and to monitor fraudulent activity.

Both Action Fraud and the FCA issue regular updates about scams, as well as hosting resources on how to beat the fraudsters.

Check out the FCA’s Fake FCA Communications page and Action Fraud’s Prevention page for more information and tips.

Staying safe from financial services scams is an important part of maintaining your financial health and welfare.

Some of the key things to watch out for to stay safe are:

At Fairstone, we have partnered with the Regional Economic Crime Coordination Centre (RECCC) to help raise scam awareness and safeguard the financial wellbeing of our clients and staff.

For more information on our approach, please click here.

To talk to one of our advisers, please get in touch.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. Always seek professional advice before making financial decisions.

| Match me to an adviser | Subscribe to receive updates |

Steven will take up the position later this autumn, bringing with him more than 30 years of experience in the financial services sector. Most recently, as Group CEO at Aldermore Bank, he led the business through a period of substantial growth, almost doubling its size after joining in May 2021, and helped the organisation earn recognition as one of the Sunday Times Top 10 Places to Work.

He has a long-standing career in financial services, having held a variety of senior positions in banking both in the UK and abroad, including Group CEO at C. Hoare & Co, the UK’s oldest privately-owned bank, and having led a number of Barclays’ businesses including as CEO at Barclaycard Business, Personal Banking for UK & Europe, and Business Banking in the UK.

Steven said: “I am thrilled to be joining Fairstone. As well as being one of the fastest growing wealth advisory firms in the UK and Ireland, it is also one of the most trusted by its clients.

“What drew me here was the clarity of purpose, doing the right thing for clients, building long-term relationships, and supporting people to make confident financial decisions.

“That approach aligns closely with my own values. I’ve always believed that integrity, stewardship, and high professional standards are essential to building trust and delivering strong outcomes.

“I’m looking forward to working with colleagues across the business to support our clients and help shape the next phase of Fairstone’s journey.”

Steven began his career aged 16 as a branch cashier at Barclays and has built a career that reflects his belief in social mobility and values-led leadership.

He served as Joint Chair of the Social Mobility Commission and was awarded a CBE in 2022 for services to banking and social mobility. Steven continues to champion inclusive opportunity across the financial services sector.

He is the current UK Chair of consumer credit reporting agency Experian PLC and has served as a Non-Executive Director on a variety of regulatory and listed boards.

Steven will take over as CEO from Fairstone’s founder Lee Hartley, who becomes Deputy Chair. Lee has led the business for the past 16 years, overseeing its growth into one of the UK’s most trusted chartered financial planning firms.

Earlier this year, Fairstone marked two significant milestones: reaching £20 billion in client assets under management (AUM) and completing its 100th partnership within the wealth management sector through its Downstream Buy-Out (DBO) investment model.

Lee Hartley commented: “Fairstone has reached a significant point in its journey, and I’m pleased to be handing over to Steven as he takes on the next phase of leadership. His experience and values are well aligned with the business as it advances towards its 2030 goals.”

With a client base of over 125,000 and annual revenues exceeding £175 million, Fairstone is now entering the next phase of its journey. Enhancements to the DBO model and a broadened long-term strategy will support the firm’s ambition to reach £40 billion in AUM by the end of 2030.

David Hickey, Independent Chairman at Fairstone, said: “I’m delighted to welcome Steven Cooper to Fairstone. His extensive experience leading major financial institutions and his in-depth understanding of retail financial services will bring invaluable insight to the group.

“I’m also really pleased that our founder, Lee Hartley, is stepping into the role of Deputy Chairman, allowing us to continue to benefit from his deep sector knowledge.

“The UK is entering a period of significant intergenerational wealth transfer, and families will need thoughtful, well-structured advice to pass on investments and protect their assets.

“There’s a real opportunity for advice led firms like Fairstone to support clients and their families through this transition, not just by offering financial expertise, but by helping people make confident, informed decisions about their future.

“With the appointments we have made, we have ensured Fairstone has the right leadership in place to guide clients through this transition and to continue delivering on our long-term goals.”

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

After all the build-up, the resumption of higher US tariffs on imported goods and services on August 1 ended up being something of a damp squib.

Thanks to new trade deals agreed between the US and a host of countries and regions including the UK and the EU, the anticipated major fall-out – and consequential market turmoil – largely failed to happen.

But should all this really be a surprise – and what does it mean for investors?

The one thing which has been predictable since Donald Trump took office at the start of this year has been his unpredictability.

As a result, there are now signs that markets are starting to get used to the somewhat quixotic nature of Trump’s actions and almost pricing in the volatility which they inevitably cause.

Let’s look back to the start of April – ‘Liberation Day’ as Donald Trump called it – when the White House overnight imposed tariffs on goods and services from a vast swathe of countries.

It is fair to say that the decision caused chaos on the markets and leading indices around the world plunged into the red.

At Fairstone Investment Management, we got a lot of calls from advisers whose clients were worried about the value of their investments and how they could be affected by the global market volatility.

In the middle of the storm caused by the initial tariffs – and subsequent days when the US and China embarked on tit for tat tariff rises to three-figure percentages – it was difficult to maintain a steady course.

Yet within a space of a few days, those tariffs were placed on pause for 90 days and the markets calmed considerably.

US equities, which took a battering in the early part of April, recovered fairly swiftly afterwards and were back to all-time highs by the start of July. This suggests that investors see the fundamentals of the US economy as sound and are not anticipating a global slowdown in growth.

Even at the start of the week when the tariff pause was going to be lifted, there was relatively little volatility, suggesting that the markets were pretty sanguine about what was to come on August 1.

While the more punitive Trump tariffs of 50%-plus threatened on some countries have not been carried through, some countries such as Canada (35%), Switzerland (39%) and Brazil (50%) are still threatened with higher rates by the Trump administration for various reasons.

There was a brief surge in the price of copper on world markets after Trump said the US is considering imposing 50% tariffs on the metal. Other than that, reaction on the markets has been relatively subdued. For example, the FTSE 100 ended August 1 close to record highs of 9,100-plus, compared with the 7,544 it sank to in the immediate wake of ‘Liberation Day’ back in April.

The idea that these delays could become a pattern of behaviour from the White House is starting to gain ground. The TACO acronym (Trump Always Chickens Out) is beginning to be quoted by traders in increasing numbers.

However, to quote a more English metaphor, it is by no means certain that the US President will continue to march his men up to the top of the hill only to march them down again.

Markets remain wary of the potential for tariffs to ramp up at short notice and the potential longer term impacts of Trump tariffs on the US economy and global trade. As a result, markets and investors will keep watching the situation closely.

As stated at the start of this article, trying to predict Donald Trump’s next move is almost impossible.

Even though the threat of punitive tariffs has largely disappeared, the effective tariff rate being imposed by the US on the rest of the world is running at around 18%. This compares with levels of between 2% and 4% for the past 40 years.

There are signs that the policy is starting to reshape global trade flows. And while Trump is in the White House, there is always the chance of sudden changes in direction.

This whole episode is almost like an object lesson in the basic rules of investment:

If you had sold investments while the indexes were plummeting at the start of April only to buy them back when markets recovered, you could have lost a lot of capital. Attempting to time the sale and purchase of investments is extremely tricky, even for investment professionals, and unforeseen events can easily upset all your calculations.

Investing is a long-term pursuit and staying invested is more effective than trying to predict market highs and lows. Changing course too often may well mean you miss out on the benefits of recovery and even a few days out of the market can be costly.

Diversifying your investments can help to reduce risk. It also means that no single downturn – even if it’s temporary – can seriously impact the value of your portfolio.

Keeping informed is important, but in the world of instant news alerts and social media froth, you can get caught up in spirals of fear or euphoria. This can lead you to make bad investment decisions. Keep an ear out but don’t let the news cycle dictate what you do.

Investment managers and financial advisers have extensive experience of market swings, unforeseen events and all manner of economic shocks. Lean on that experience by taking professional financial and investment advice to ensure your plans are best placed to withstand the turbulence from Trump tariffs, trade wars or other events which could affect your financial future.

Tariffs are an excellent example of the unpredictable external forces which can impact your investment plan.

Keeping calm, staying the course and sticking to your long-term strategy is a wise way to deal with such events.

| Match me to an adviser | Subscribe to receive updates |

Disclaimer: It is important to note that the value of investments and the income from them can go down as well as up and that you may get back less than the amount you invested. This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax treatment depends on individual circumstances and may change. Always seek professional advice before making financial decisions.