Market Updates

Oliver Stone

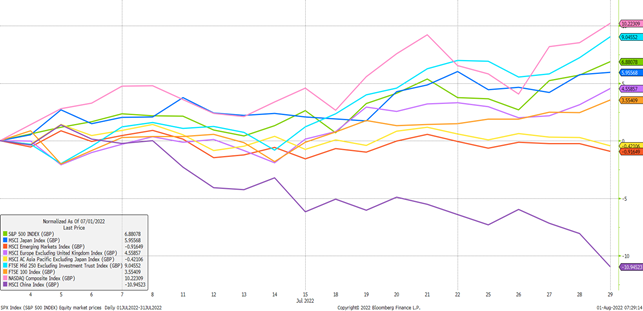

Equity markets furnished investors with some better news through July as we saw a concerted recovery most notably in those developed markets that had previously struggled in 2022. As the first chart below shows, the tech heavy NASDAQ and the midcap biased FTSE 250 were strongest, rising by 10.2% and 9.0% respectively, with other developed markets arranged behind them also generating positive returns:

We don’t yet know how sustainable this recovery in developed market equities is, but for now, it has the feel of a ‘relief bounce’ given the swathe of negativity we’ve seen. Over the past few weeks, markets have begun to react less negatively to poor macroeconomic data and hawkish central bank news; an indication that relatively bearish expectations may already be priced in to a certain extent. This being said, there are still clear reasons to remain cautious.

In contrast to June, Asian and broad Emerging Market indices were relative laggards, falling by 0.4% and 0.9% respectively. This underperformance was driven by Chinese equity losses of 10.9%, erasing last month’s stellar outperformance. Despite some positivity in China around Covid reopenings and the potential for stimulus to be brought forward, volatility is persisting because risks still remain to that more positive view.

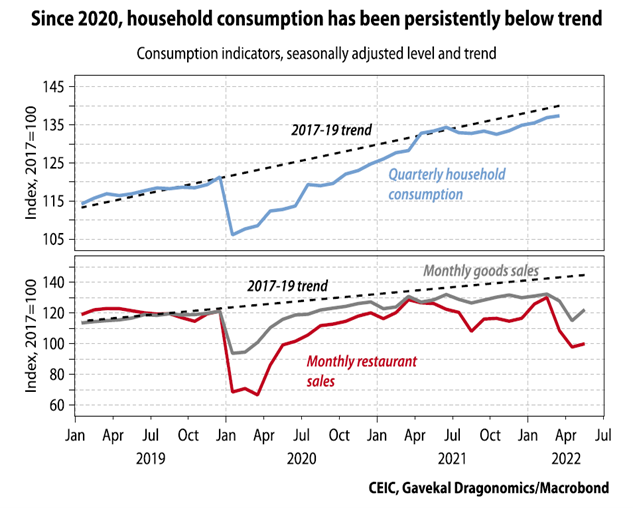

The authorities are still persevering for now with their ‘dynamic zero-Covid’ policy, which is proving a barrier to full recoveries in consumer spending and the labour market.

In the second chart below we can see aggregate household consumption in the top panel still firmly below its trend, whilst the bottom panel highlights more granular weakness in consumption data relating to goods and restaurant sales which have also fallen away again recently:

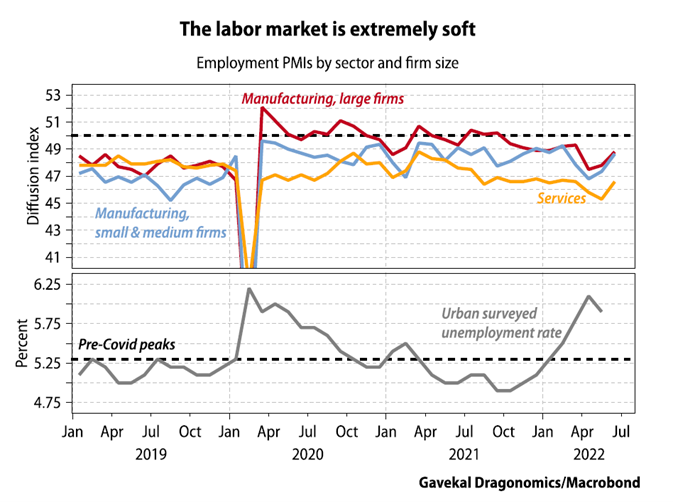

The third chart below shows the state of the Chinese labour market. The top panel shows employment survey data for manufacturing and services companies, with each of the survey components indicating that employment has been in contraction now for several months. Indeed in the case of services and small & medium sized manufacturing businesses, the contraction has been extensive.

As a corollary, the unemployment rate in the bottom panel shows a substantial rise in 2022, the effects of which have included increased consumer uncertainty, dampened confidence and impaired spending plans:

Geopolitical machinations in Taiwan may distract from the domestic picture temporarily, but it is clear that mounting economic uncertainty means investors are now looking for clearer signals on policy, which are yet to emerge after the Politburo’s quarterly economic meeting in July.

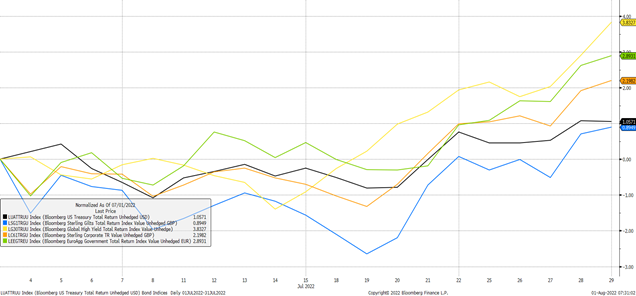

Bond markets also saw a welcome recovery in prices across the board in July, with riskier parts of the credit market outperforming government bonds as the fourth chart below shows. Global high yield bonds and sterling corporate bonds rose by 3.8% and 2.2% respectively, whilst UK Gilts rose by 0.9%:

These positive returns may seem strange given the prevailing central bank narrative is very much geared towards higher interest rates and generally tighter monetary policy to combat inflation, but as indicated above, it has been a change in market expectations that has driven this change in price action.

We do, however, think there are a number of risks to the market’s current viewpoint.

The first and most obvious risk is that inflation can still surprise to the upside, and for now does appear to be doing so. Even though the headline rate will probably moderate by the end of this year, it will still be very high, and many component parts of the inflation basket appear to be rising in a persistent manner. The US Federal Reserve made it very clear at their most recent meeting that they will be data dependent in terms of their rate hiking cycle from now, meaning that if inflation prints are worse than expected in the coming months, markets will need to readjust their expectations.

Second, wages are still rising strongly in nominal terms, if not currently in real terms, and the longer this persists, the greater the risk of sticky or persistent inflation. In the US, employment costs rose more than expected in Q2 by 5.3% y/y, which again implies the possibility of a more hawkish Federal Reserve. Here in the UK, we have the threat of more strike action across multiple sectors unhappy with their pay settlements.

Finally, a more negative scenario centred around Russian energy supply is still on the table. European countries, particularly Germany, are preparing for a full removal of supply which would require huge fiscal support and energy rationing into the winter. While that doesn’t sound immediately bullish for inflation, the rises that would be seen in various prices, combined with massive fiscal support would see a shift in market expectations.

In light of these risks and in spite of the more recent positivity, we would encourage diversification across portfolios, particularly as we look ahead towards the colder months.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

For further information, please contact:

Oliver Stone

For further information, please contact:

Oliver Stone

(1)")