Market Updates

Oliver Stone

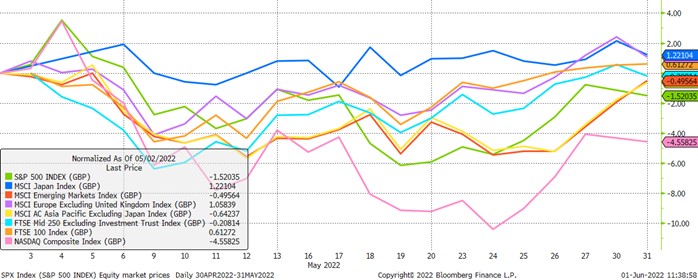

Equity and bond returns were muted again through May as uncertainty around Ukraine and Chinese Covid lockdowns were the predominant narrative drivers. The first chart below shows global equity indices over the month in pound terms, with developed markets generally outperforming emerging markets. This was despite a strong rally into the end of the month for the latter group, driven by a recovery in Chinese stocks as the authorities continued to signal support for an economy battered by extremely harsh and increasingly irrational lockdowns:

Japanese and European equities were strongest with returns of 1.2% and 1.1% respectively, while US equities fared worst as richly valued technology stocks were shunned by investors, exemplified by the Nasdaq’s 4.6% fall. Investors here are still coming to terms with the highly inflationary environment in combination with a much more hawkish Federal Reserve which insists it will seek to aggressively combat inflation and inflation expectations with tighter policy.

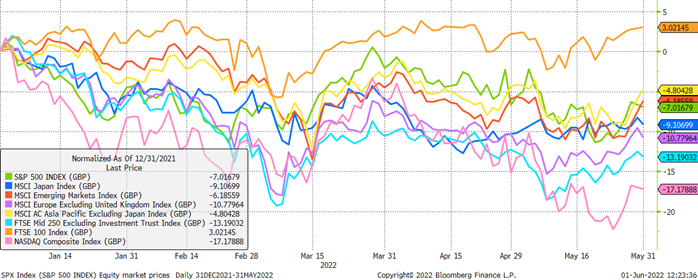

The FTSE 100 posted another positive return of 0.6% to continue a fine run of form in 2022. As the second chart below shows, the UK large-cap index is the standout performer amongst the major global indices, rising by just over 3%, versus -7% for the S&P 500; this in spite of a much weaker pound benefitting the translated returns of overseas equity investments.

The index is heavily tilted towards beneficiaries of the current macroeconomic environment, with more than 40% of its members sitting in the energy (13%), materials (12%) and financial (16.5%) sectors; weightings that are at odds with other developed market indices in particular. In previous years this has hindered relative performance, but in the face of significant commodity supply chain disruption and rising interest rates, it is proving to be an optimal mix:

The strong relative performance for the FTSE 100 has come as the UK economy has begun to struggle under the weight of a dual slowdown in consumer and business activity amidst very high inflation – 9% in April – and geopolitical uncertainty. To illustrate this, the FTSE 250 index of mid-cap, more domestically focused UK companies has struggled this year, falling by 13.2%. The Bank of England’s latest forecasts paint a gloomy picture of the year ahead, with Governor Andrew Bailey’s comments on the Bank’s ‘helplessness’ in combating inflation highlighting the difficulties facing the economy.

In response to the increasing cost of living crisis centred around energy prices, Chancellor Rishi Sunak unveiled a new package of financial support for households worth in the region of £15bn (0.6% of GDP) and weighted towards those households in most need of relief through the colder winter months.

However, alongside the additional spending, the Chancellor introduced a controversial, temporary windfall tax on energy companies’ ‘excess profits’; a measure that he had repeatedly criticised in the months leading up to the plan’s announcement, having previously argued that the obvious impacts of a windfall tax would be to deter investment, undermine competition and kill off jobs.

The levy is expected to raise £5bn in tax revenue this year, offsetting just one third of the Government’s planned outlay, and further, in direct contradiction to its intention, has already resulted in business investment plans being placed on an uncertain footing per comments from BP immediately following the announcement.

The UK is certainly not alone in its cost of living crisis driven by high energy prices, and now joins many European countries in providing fiscal handouts to struggling consumers. But, rather than simultaneously encouraging investors to pour much-needed capital into the oil and gas sector to combat Russia’s systemic importance in global energy and manufacturing supply chains, the Government has succumbed to an optically popular but regressive short-term policy option that will potentially exacerbate the problem rather than help to solve it.

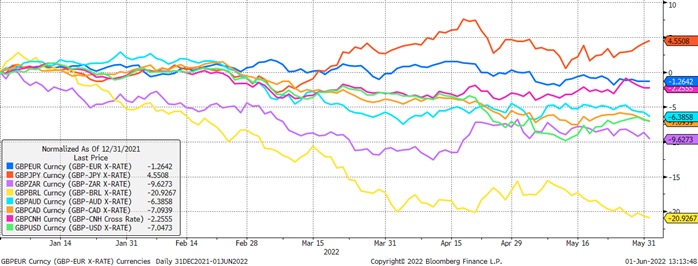

As mentioned in previous notes, investors’ perceptions of the UK economy have played out in the currency and bond markets this year, with the pound notably weaker this year versus almost all major currencies as the third chart below shows. Only the Japanese Yen (in dark orange) has fallen against the pound this year as the Government there persists with an extremely easy monetary policy stance. Elsewhere, weakness is pervasive, with falls of more than 7% against the US dollar (in green), and an extraordinary 21% fall against the Brazilian real (in yellow) which is benefitting from much higher commodities prices:

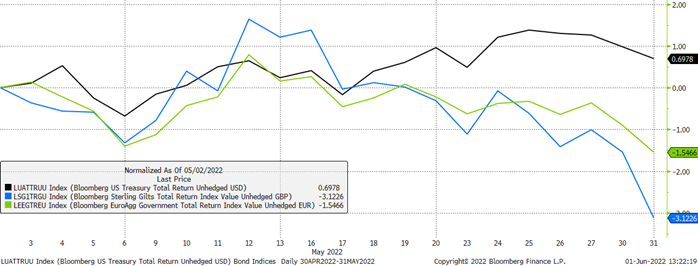

As the final chart below shows, UK government bonds have also begun to underperform global counterparts, with the Gilt index falling by 3.1% in May versus a fall of 1.5% for Eurozone government bonds and a rise of 0.7% for US treasuries. This is despite a hawkish Bank of England keen to carry on with rate hikes and shows weakening confidence in the UK economy:

As per last month, uncertainty will reign until a genuine improvement occurs in Europe. While commodities prices may not rise precipitously from here, they are unlikely to fall back to previous levels until a firm resolution has been agreed: something we sadly see few signs of at the time of writing. As always this speaks to the importance of diversification across portfolios.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

For further information, please contact:

Oliver Stone

For further information, please contact:

Oliver Stone