Market Updates

Oliver Stone

July was a month of cautious optimism across global financial markets. Risk assets broadly moved higher, central banks struck a more dovish tone, and geopolitical tensions—while still present—showed signs of de-escalation. Yet beneath the surface, the macroeconomic and policy landscape remains complex, with trade dynamics, inflation trajectories, and fiscal pressures continuing to shape investor sentiment.

Global equities delivered strong returns, building on the momentum from Q2. Chinese equities led the way, gaining over 8% in GBP terms and recovering some of the lost ground seen this year after tariff-related relief. The NASDAQ was also strong, up around 7.5% in GBP terms, fuelled by robust earnings from large-cap tech and AI-focused firms. Encouragingly, market breadth improved, with the equal-weighted S&P 500 rising 3.5%, suggesting the rally extended beyond the usual mega-cap suspects.

UK equities also had a good month in absolute terms, with the large-cap FTSE 100 gaining 4.2%, benefitting from its commodity-heavy composition which saw better earnings and a brighter outlook for energy and materials:

Bond markets were more subdued. Early-month weakness gave way to an anaemic rally in the latter two weeks of July, but government bond yields remain stubbornly high, driven by still-robust economic data and increased government debt issuance. For the most part, this left returns broadly flat to modestly negative across fixed income.

In the UK, the 10-year gilt yield edged up from 4.45% to 4.53%, reflecting persistent inflation and fiscal concerns. The Bank of England’s decision to cut rates by 25bps to 4% was narrowly passed, with a second round of voting required. The MPC’s messaging remains mixed, balancing signs of labour market fragility with lingering inflationary pressures. While another cut in November is still expected, confidence in that call has waned.

Across the Atlantic, the Fed held rates steady at 5.25%, but July’s weaker-than-expected jobs report—alongside downward revisions to May and June—has raised the odds of an earlier rate cut. The unemployment rate ticked up to 4.2%, and the foreign-born labour force shrank significantly, reflecting the impact of Trump’s immigration policies:

Inflation data was a mixed bag. In the US, core CPI surprised to the downside, reinforcing disinflationary trends. However, headline inflation remains sticky, particularly in services and food. The UK saw an unexpected rise in headline inflation to 3.6%, the highest since January 2024. Despite this, markets still anticipate further rate cuts, driven by weakening labour market indicators and sluggish growth.

Europe’s inflation hovered around the 2% target, allowing the ECB to pause its easing cycle after eight consecutive cuts. The central bank’s dovish stance has helped anchor rate expectations, though fiscal challenges and trade uncertainty continue to cloud the outlook.

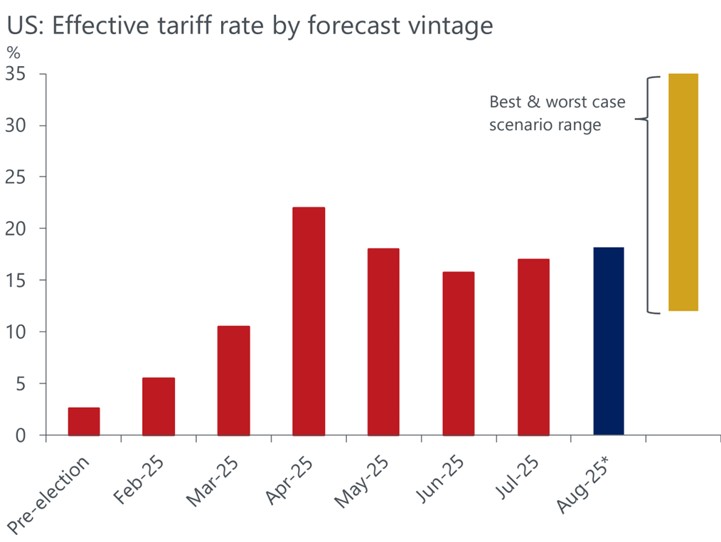

Trade policy remained a dominant theme. The Trump administration’s “One Big Beautiful Bill Act” and a flurry of trade agreements helped calm markets, but effective tariff rates are creeping higher again. As of August 1, the statutory tariff rate stood at 18.2%, up from 17% in July. While headline rates have moderated for many countries, exemptions and preferential deals mean the actual impact varies widely:

For a deeper dive in to the July update, listen to our podcast with Portfolio Manager Harry Scargill and Investment Director Oliver Stone as they break down the key market themes that shaped the month.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: