Market Updates

Imogen Hambly

Hopes for a so-called ‘soft-landing’ persisted through May, with cooling inflation and signs of improving growth helping to drive gains across all major equity regions, in local currency terms. However, an appreciation of sterling versus most other major currencies weighed on GBP denominated returns.

Once again, performance from commodity markets was strong, driven by rising activity levels and expectations of supply shortages in some key materials – most notably copper, where prices of the metal hit all time high levels, before dropping back as the month came to a close. Elsewhere, ongoing tensions in the Middle East led to a mid-month rally in safe-haven gold.

Across bond markets, the emerging environment of improving growth and falling inflation led to mixed outcomes, as investors struggled to comprehend the trajectory of monetary policy movements. Mid-month reports of moderating US CPI inflation created increased expectations for interest rate cuts, driving down bond yields initially, before strong labour market data pushed yields in the other direction. A month end rally in bond prices was then triggered by a US PCE inflation print that indicated a weakening in consumer spending.

At a global level, correlations between bonds and equities were noticeably high throughout May, indicative of a market that is firmly focused on movements in inflation.

On a regional basis, the US market resumed its positive streak, with the Nasdaq (in pink, above), gaining 5.0% in sterling, benefitting from a set of exceptional results from technology giant, Nvidia. Earnings reports from the chipmaker continue to impress traders, with reported quarter one profits and revenues exceeding analyst predictions. Looking more broadly, ongoing corporate strength, coupled with optimism over monetary policy easing led both the Nasdaq and the S&P 500 (in green, above) to reach record highs through the month.

Elsewhere, the broadening in returns continued, with Chinese equities (above in purple) rallying particularly strongly through the first half of the May, as market participants reacted positively to the latest round of policy driven stimulus and sought to capitalise on the region’s low valuations. Despite exuberance waning towards month end, in GBP terms Chinese equities still managed to eke out a modest 0.3% gain – in local currency terms however, this equates to a more pleasing 2.1%. Wider Asia Pacific (above in yellow) and Emerging Market (in red) equities benefitted from China’s positive performance, albeit sterling denominated returns from both regions were ultimately negative.

Japanese equities (above in dark blue) had a more difficult month as ongoing weakness in the yen weighed on investor sentiment towards the region. In GBP, the Japanese index fell 0.5%.

Closer to home, the UK’s mid cap index, the FTSE 250 (in light blue, above), had a standout month, adding 5.1% and outperforming the large cap FTSE 100 (in orange), which gained a more reserved 1.6%, having posted a new record high earlier in the month. Once again, strong performance from the UK indices is reflective of a broadening market and of investors’ renewed interest in undervalued stocks. As noted last month, this undervaluation of UK Plc. is not going unnoticed, with the pickup in M&A interest in UK companies continuing to create headlines. Through April it was mining giant BHP’s interest in Anglo American that drew the most attention, albeit Anglo have since rejected the offer. More recently, rejected bids for financial services firm Hargreaves Lansdown provided further proof of just how cheap, good quality UK companies are – a factor that bodes well for investment into the region moving forward.

Across fixed income, as noted previously, shifting interest rate expectations drove market movements through May. As the chart above shows, UK gilts (in dark blue) had a volatile month, rising over 2.5% in the early weeks before retreating to close up 0.8%. US government bonds (in black) performed slightly better, with a pullback in yields leading to a reversal of the losses seen during April.

Once again, corporate bond indices outperformed their government bond counterparts, with earnings growth and resiliency across the corporate sector providing credit with an element of protection against swings in interest rate expectations. The global credit index (in purple) added 1.8%.

While the direction of travel that certain central banks are going to take with regard to their key policy rates is becoming increasingly clear – most notably the European Central Bank (ECB) – market movements firmly indicate that for other key policy makers, things remain a lot murkier.

Within the Eurozone, growth data surprised to the upside through the May, while inflation appears to be trending downwards, allowing markets to believe, with an element of confidence, that the ECB will be the first of the major central banks to cut rates, with a cut on June 6th all but locked in by traders.

Looking towards the US and the Federal Reserve (the Fed) though, the picture is significantly less clear.

The release of April’s US CPI print showed a very small cooling in inflation, although the region’s labour market remains tight, leading the Fed to temper its rhetoric around imminent rate cuts. Furthermore, looking at PCE inflation, a broader measure that is known to be the central bank’s preferred metric, there was a slight increase in prices through April, albeit this was coupled with a weakening in consumer spending.

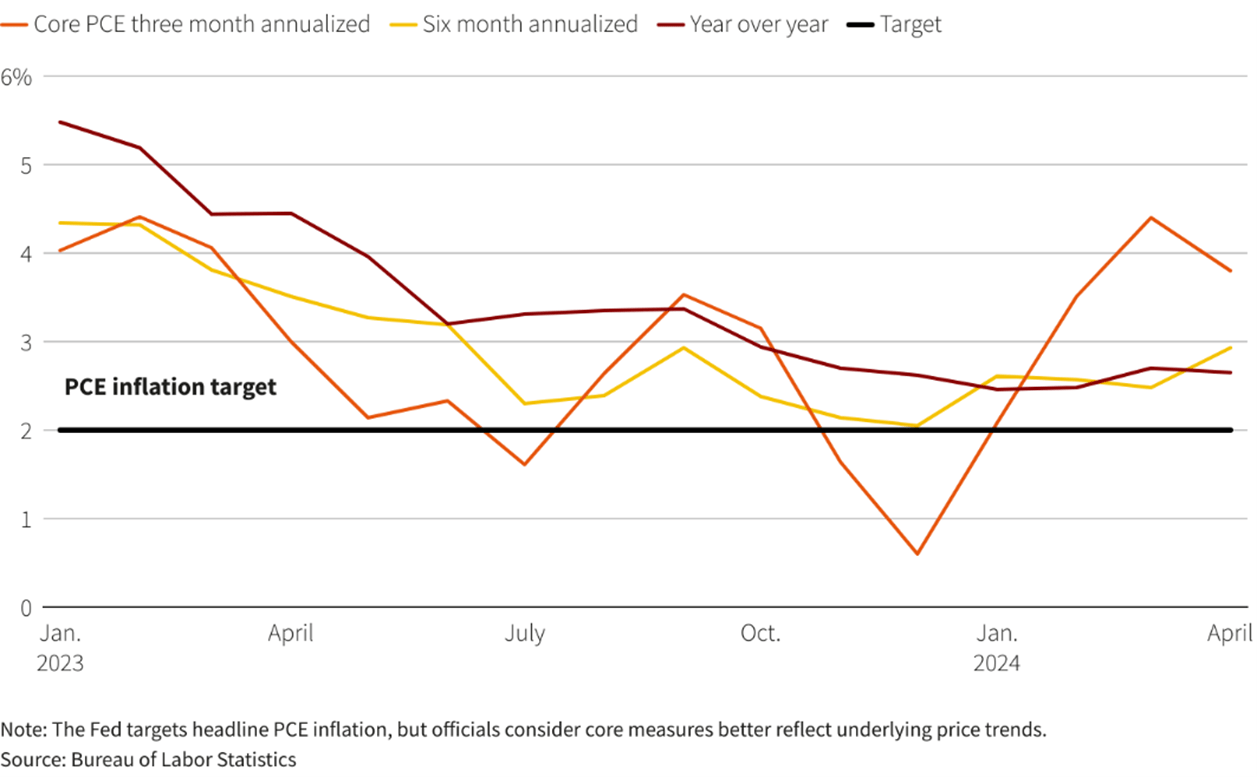

Looked at in combination, recent data releases do point towards a softening in the US inflation picture, however, as the chart below shows, when viewed on a year over year basis, PCE inflation is clearly beginning to stall – and it appears to be doing so at a rate that is somewhat higher than the Fed’s target 2%.

Whether this stagnating inflation picture affects what the Fed does moving forward is yet to be seen, but there is reason to think rates in the US will stay elevated for a little while longer. By way of a reminder, coming into this year, markets were pricing in 1.5% of cuts from the Federal Reserve during 2024. A far cry from the 0.5% that is currently predicted.

Finally, looking at the UK, the picture is different again. Despite falling from 3.2% to 2.3% through April, the region’s most recent inflation print came in above expectations, with the drop driven in its entirely by so called ‘base effects’. As such, with inflationary forces still at play across the UK, the scope for a June interest rate cut from the Bank of England is limited – a point that is particularly important in the context of the general election on July 6th, as the Bank will want to ensure its actions are not viewed as being in any way politically motivated.

Needless to say, as we move into the summer months, we expect volatility across markets to continue, given ongoing uncertainties around interest rates, inflation levels, and the political landscape. However, current data indicates that global growth is beginning to pick up, corporate earnings are improving and valuations in a lot of areas remain very attractive, all which provides us with plenty of room for optimism.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: