Market Updates

Oliver Stone

")

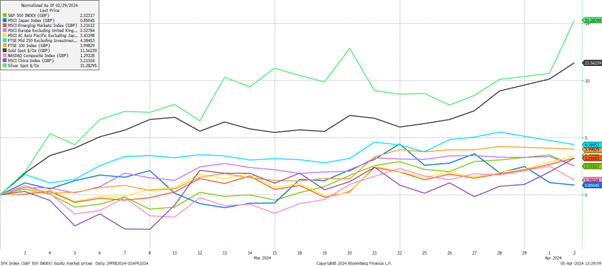

Additionally, we have seen extraordinary strength within the precious metals space in recent weeks, as the prices of gold and silver have rocketed alongside associated mining equity prices, per the first chart below. Silver (light green line) rose by more than 15% during March, with gold (black line) up 11.5% also far outpacing equity markets. As could be expected, precious metals mining companies’ returns – which are a higher beta play on the precious metals space – were even stronger; over the month silver miners rose by 31.5% and gold miners by 25.0%.

Intriguingly, precious metals have been rising despite ‘normal’ conditions for a run up not being in place; the US dollar has been strengthening, while inflation adjusted government bond yields have also been rising, neither of which should be good for gold nor silver prices.

Indiscriminate global central bank purchases are the most likely cause of the recent strength, with notably China and India steadily and in large size adding to their gold reserves over the past 18 months. Many reasons have been offered as to why – perhaps central banks are worried about the US dollar’s role as an economic weapon vis a vis the treatment of Russian assets as a result of their invasion of Ukraine, or perhaps they are worried about the re-emergence of inflation.

Regardless, should the prices of the metals continue to increase, we can reasonably expect mining equities’ prices to also increase, and given this part of the market is extremely cheap with outstanding operational leverage, we see the space as a good diversifier looking ahead.

Excluding precious metals, the best performing equity region this month was the UK. The mid cap, domestically focused FTSE 250 (light blue line) and the FTSE 100 indices (orange line) both performed very strongly, rising by 4.4% and 4.0% respectively, and were driven by some of the positive macroeconomic factors we wrote about in detail last month; PMI surveys continue to show signs of strength in both the services and manufacturing sectors, GDP has returned to positive territory, the labour market remains strong, and inflation continues to surprise to the downside. Notwithstanding the political volatility we might see later this year, we still think the UK is in a good spot, and equities remain cheap.

Elsewhere, at the bottom of the performance rankings this month were Japanese equities, only rising by 0.9% over the month after taking a break from a powerful run up, and the US tech-focused Nasdaq index which rose by 1.3% during the month.

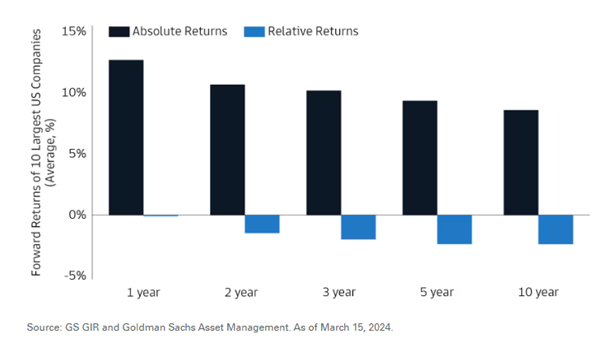

Of course this is only a 1 month time period, but as mentioned above, what we have begun to see is a wider participation in risk asset positivity, which is beneficial for those invested in other asset classes that perhaps haven’t performed as strongly over the last year, and perhaps an early warning for investors heavily concentrated in previous winners.

To illustrate this, the second chart below quite simply illustrates the notion that momentum simply cannot last indefinitely. It shows the subsequent forward returns for the 10 largest US companies over various time frames in absolute terms (black bars) and relative terms versus the S&P 500 index (blue bars), going back to 1980.

The obvious takeaway message is that while these companies do usually continue to generate positive absolute returns on a forward looking basis, their returns relative to the wider index deteriorate to a greater or lesser extent as time moves on; today’s top firms may continue to lead the market in the near term, but we think investors seeking diversification and alternative sources of alpha may find opportunities elsewhere.

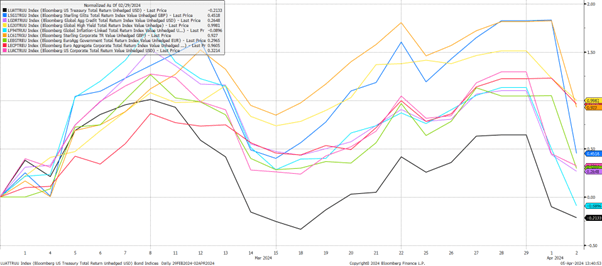

Turning to fixed income, the third chart below shows bond index performance over March, where we can see what was looking like a fairly positive month sharply reversed as investors adjusted their expectations for interest rate cuts:

Best performing again were corporate bond indices which were swung around less by these changing expectations, with government bond indices drawing down much more sharply into the end of the month. The cause of this was various indicators relating to labour markets coming in hotter than expected, and some central bank economists intimating for the first time that if economic data remained hot, that perhaps interest rate cuts might not be needed at all in 2024.

For now, in the US which remains home to the world’s most important central bank, official forecasts as of March were for growth to remain strong, for inflation to fall though remain above target, but crucially for interest rates to still be cut 3 times this year. It seems that the Federal Reserve and other central banks believe policy is restrictive and rate cuts will reduce the amount of downside risk to the economy in the future. They may well be right, but it is still an open debate as to whether policy is as restrictive as they think. Financial conditions have eased significantly since the end of October, with for example the housing market, a key interest rate sensitive sector, rebounding strongly over the last couple of months.

Needless to say, markets like hearing this pro-growth bias from central banks, however, as you can see from the chart above, these same markets still have a reaction function and do not like seeing macroeconomic data surprises that imply an invalidation of their thesis.

As we look ahead into the second quarter of 2024, market conditions have become more fractious, with geopolitical tensions bubbling to the surface again in the Middle East (if indeed they had ever gone away) as Iran attacked Israel. Volatility is elevated across asset classes, which is something we expect to persist, though close attention will still need to be paid to macroeconomic data releases in the coming months given investors’ focus on them, and their importance to the continuation of the current market narrative drivers.

As we have written many times before, there remain plenty of opportunities across different asset class, but as always, diversification will remain key as we try to navigate this highly changeable market environment.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: