Market Updates

Oliver Stone

The overarching theme for November was one of ‘reversal’. We saw something of a relief month, with big bounces enjoyed by many asset classes unloved or depressed through 2022. Much of the strength was driven by several US macroeconomic data points that were softer than expected, along with some more nuanced language from the Federal Reserve.

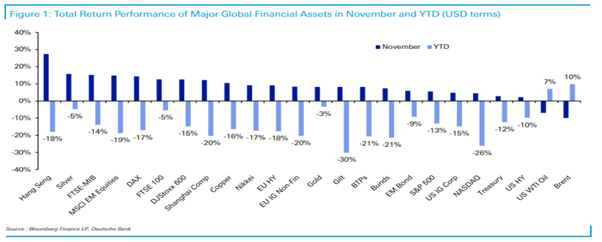

The first chart below summarises the narrative perfectly. It shows a wide range of asset classes listed along the X axis: equities, bonds and commodities, and compares their percentage return in the month of November (dark blue bars) to their year-to-date return (light blue bars).

As can be seen, in November, every asset class listed here moved in the opposite direction to their year-to-date trend, with the likes of Hong Kong equities and Silver performing particularly strongly. On the other side, one of the few asset classes to fall in November was oil (labelled as ‘Brent’ and ‘US WTI Oil on the far left hand side of the chart), having previously enjoyed a stellar 2022:

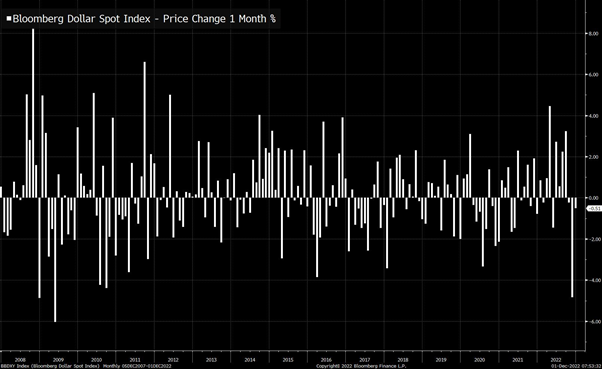

One of the biggest drivers of this turnaround was a much weaker US dollar. We’ve spoken about the dollar many times this year in terms of its strength causing falls across equity, bond and commodity markets, but this month it saw its weakest monthly performance in over a decade, as the second chart below shows. Each bar represents a monthly percentage return of the Bloomberg US Dollar Index – an index which tracks the performance of the US dollar versus a basket of major currencies – with the penultimate bar on the left hand side being November’s return:

The dollar moved lower through the month as we saw some indications of weakness in US labour markets, coupled with a lower than expected inflation print, but the move was turbocharged at the end of the month by Federal Reserve Chair Jerome Powell, who gave a speech that was perceived to be dovish by investors. Previously, Powell has pushed back aggressively against any loosening in financial conditions, deeming it inconsistent with the Fed’s mandate to kill off inflation, but the consensus in this instance was that there was a softening of his tone.

Of course, the million dollar question is: will these easier conditions continue? Well, US jobs data at the start of December was stronger than expected, with more jobs added and wage growth higher, and the Fed is still making it clear that they will react to stronger economic data with a more hawkish view.

Certain asset classes had become very oversold and may have been due a bounce regardless, however, as above, there are signs of some slowing down in the admittedly volatile month-on-month inflation and jobs data.

For now, we see the best course of action as being to look at the data as it comes in and continue to wait for a more established trend. As said throughout the year, we’re in a state of extremely high uncertainty, with now not a time to try and second guess a central bank’s thinking.

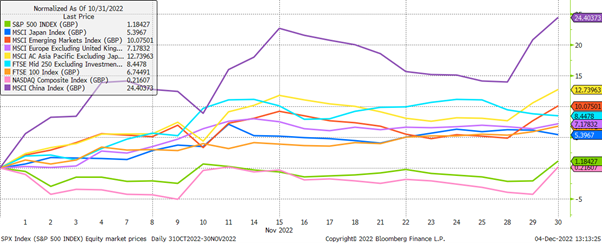

Digging into individual markets in more detail and continuing the theme of reversal, though we saw positive returns for all the major indices in pound terms, we saw an enormous recovery in Chinese equities from last month’s losses, with the MSCI China index rising by more than 24%:

As we discussed last month, we believed that the negative sentiment towards Chinese equities was a shorter-term issue, and with sentiment already very low and valuations very cheap, a rebound was more likely than not. Recent protests around draconian Covid restrictions have made international headlines, with the Chinese authorities now seemingly loosening Covid policy at the margin in recognition of its unviability.

Strength there boosted broader Asian and emerging market equity indices which rose by 12.7% and 10.1% respectively, with the UK Mid 250 index rising by 8.4%; again another index recovering from a very weak 2022.

US indices were noticeably weaker, with the weaker dollar hurting US equity returns when translated back to pounds. Equally though, that same weakening acted as rocket fuel for asset classes previously under pressure, including Chinese equities.

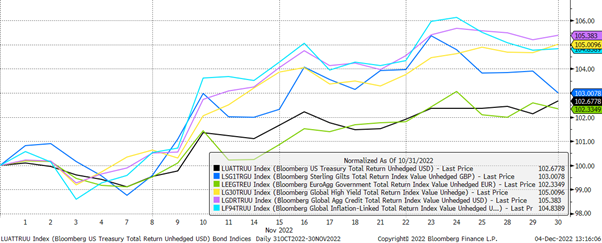

Finally, in bonds, again a recovery was seen as yields moved lower and prices higher. Riskier corporate bonds outperformed government bonds, though all major asset classes saw welcome gains as the chart below shows:

How long these rosier conditions last, we cannot know; indeed at the time of writing it seems that volatility may have returned in the wake of stronger than expected US economic data. We expect the market’s focus to be fully trained on central banks and their monetary tightening plans in the runup to Christmas, with investors looking for any deviation from consensus. As always, this points to the importance of diversification across portfolios.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: