Market Updates

Oliver Stone

October was a month that kept investors on their toes, with plenty of moving parts across asset classes and regions.

Equities had another strong run, especially in Emerging Markets and Asia ex-Japan which rose by over 6% in both cases. Domestic demand, AI-driven tech momentum, and supportive monetary policy were the main drivers. The US market was led by the “Magnificent Seven” mega-cap tech stocks – illustrated by the strong performance of the NASDAQ index – whose Q3 earnings were robust, particularly in cloud and AI segments. Their performance lifted the S&P 500, even as some of the broader index constituents lagged. The ongoing US government shutdown was a headline risk, but so far hasn’t overly dented market performance.

Chinese equities were notable laggards in October, falling by around 1.5% and taking a bit of a breather from the very strong performance seen in August and September. Still, as mentioned above, broader EM and Asian markets were very strong, with India, Taiwan, and South Korea all posting impressive gains. Japanese equities also posted handsome gains, helped by a weaker yen and a surprise pro-stimulus election result.

UK equities also underperformed, and particularly domestically focused stocks as represented by the FTSE 250 index which rose by just 0.3%. UK macroeconomic data were soft, with GDP and PMI readings disappointing, and inflation remained stubbornly above target. More attention will turn to UK assets next month as the upcoming budget on 26th November is eagerly anticipated.

Bond markets were generally positive as well. Here, UK assets were the standout performers, with UK Gilts rising 2.9% – their best month in nearly two years thanks to softer than expected (though still high) inflation data and expectations for Bank of England rate cuts, and investment grade corporate bonds rising by 2.2%.

At the other end of the spectrum, while still positive, US assets were relatively weak as they gave up some of the previous months’ outperformance. While the Federal Reserve cut interest rates as expected, and announced an end to ‘Quantitative Tightening’, the rhetoric from Jerome Powell was more hawkish than expected on forward looking policy, which disappointed markets somewhat:

On the macroeconomic front, the global backdrop remains supportive for risk assets. US economic data pointed to moderation, with GDP growth slowing but still resilient. Headline inflation ticked up slightly, while core inflation eased marginally, reinforcing expectations for further monetary support. As mentioned, above the Fed’s rate cut was widely anticipated, but Chair Powell’s cautious tone on future policy disappointed some market participants.

In the UK, GDP grew just 0.1% in August after a similar decline in July, while unemployment edged higher and inflation held steady at 3.8%, marginally below forecasts. Subdued growth expectations and positioning ahead of November’s Budget pushed Gilt yields to three-month lows. In Europe, inflation moderated further to 2.1% in October, moving close to the ECB’s target and reinforcing expectations that policymakers will maintain their patient stance.

US fiscal and tariff policies remained central to the macro narrative. While major, market-moving tariff headlines are less frequent than earlier in the year, protracted negotiations most notably with China still have the potential to surprise positively or negatively, and must be closely watched.

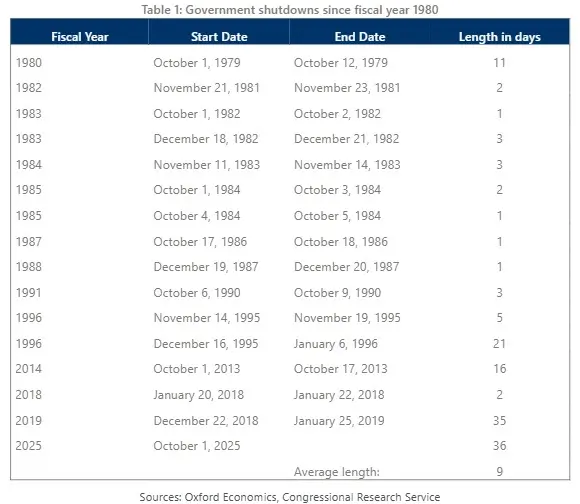

The US federal government shutdown began on 1st October, with major services shuttered and workers furloughed. The primary dispute is ostensibly centred around healthcare spending, and while shutdowns aren’t uncommon, at the time of writing this one is notable for now being the longest in history, currently spanning 38 days:

Each week of shutdown is estimated to reduce annualized GDP growth by 0.1–0.2 percentage points, or up to $15bn per week, and the longer the shutdown persists, the greater the risk to government-funded programs and investor sentiment. Markets have largely looked through the headline risk so far as most of the damage caused by the shutdown will be reversed as federal employees receive back pay, delayed federal contracts are finally approved, and social benefits like SNAP resume in full.

However, the lack of government data makes it difficult to determine whether there have been significant spillover effects from the shutdown into the private sector. For example, jobless claims data point to some private-sector layoffs in States most exposed to the shutdown, but the full impact will only be known once the government reopens for business.

Overall, October reinforced the importance of agility and vigilance in portfolio management. While markets have shown resilience, the interplay of monetary policy, fiscal dynamics, and geopolitical risk continues to drive volatility and opportunity. We remain constructive but cautious, favouring quality, diversification, and active risk management as the global landscape evolves.

For a more detailed look at this month’s update, listen to our Market Update podcast. Join Investment Director Oliver Stone and Portfolio Manager Harry Scargill as they break down the key market developments shaping October. From equities and fixed income to macroeconomic trends and the evolving policy landscape, our experts share timely insights to help you navigate the months ahead.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: