Market Updates

Oliver Stone

")

Russian forces attacked cities across Ukraine overnight (23rd/24th February) after President Vladimir Putin ordered a ‘special military operation’ to support separatists in the Donbas region of Ukraine. Moscow confirmed that it is targeting military facilities in an attempt to demilitarise Ukraine, with reports of conflict in the capital, Kyiv.

The situation is extremely fluid, but President Putin has claimed he does not plan to occupy the country, and that energy supplies to Europe via Ukraine will not be disrupted.

Unsurprisingly the latest moves have been met with widespread condemnation from international leaders, with US President Biden announcing his intent to impose ‘severe sanctions’ on Russia and vowing a united and decisive response from Ukraine’s allies.

At the time of writing, global stock markets and government bond yields have moved lower, the price of Brent crude oil has passed $100 per barrel for the first time since 2014, while gold and silver prices have sharply increased. Outside of Russia itself, European equities have been hardest hit, with indices down up to 5% on the day, with the UK and US outperforming in relative terms thus far, falling by 2.5-3%.

We would expect volatility to persist until the situation becomes clearer. Additional sanctions will undoubtedly be announced by the US, Europe and UK in the coming days, most likely related to the movement of capital and goods. This in turn raises the probability that Russia will seek to respond in kind, with its main weapon being the supply of oil and gas to Europe.

As has been well-reported, Russia has already been restricting the flow of natural gas into Europe, and the aim of any further restrictions here would be to cause enough economic pain that Western leaders are forced to accept that Ukraine becomes a Russian client state within Moscow’s exclusive sphere of influence.

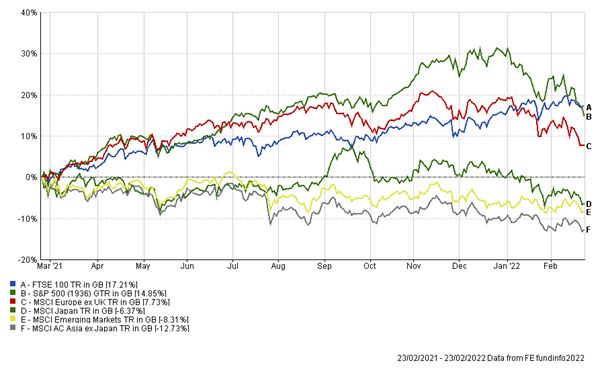

For now, we continue to watch the situation closely and will report on any further developments. Over a rolling 12-month period, developed market equities are still broadly in positive territory per the chart below, with emerging market and Asian equity indices providing strong relative returns in recent months, despite being negative over the past year in aggregate:

Within portfolios we are not planning any immediate changes, and we remain focused on finding long-term valuation opportunities across asset classes. Should a peace deal be struck in the coming weeks, a good buying opportunity will be presented to investors, although downside risks to that view remain. As always, diversification is of paramount importance, with real assets in the energy and commodities space performing particularly well at the moment.

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Match me to an adviserFor further information, please contact:

Oliver Stone

For further information, please contact:

Oliver Stone