Market Updates

Oliver Stone

Discover more insights from our Divisional Director, Peter Donaldson, and Investment Director, Oliver Stone as they delve deeper into last month’s market update.

We saw a mixed month for equities in the round, with weakness in several regions obscured by a very strong last trading day of September as the first chart below shows; indicative of quarter-end rebalancing. The UK’s FTSE 100 index (orange line) rose most by 2.3%, with performance driven by gains from more cyclical, value stocks, helped along by a weaker pound. Energy stocks performed particularly well, with the oil price having risen by around 30% since its June lows. As a reminder the FTSE 100 is heavily exposed to that sector to the tune of around 15%.

The UK has been receiving a modicum of positive press recently, with the FTSE 100 making headlines in regaining its status as Europe’s largest stock market by market cap, and with some strategists starting to recommend a tilt towards it as the inflation picture here finally starts to look more controlled. Valuations remain highly compelling across a range of metrics, both in the FTSE 100 and even more so in the mid-cap focused FTSE 250 index, which had another poor month (light blue line) despite a last day bounce. With outflows from UK equity funds continuing, and survey data showing global fund managers are very underweight the UK, we feel that there is scope for significant improvement here.

Elsewhere, the US tech-focused Nasdaq index (pink line) struggled this month, falling by 2.3% as US bond yields continued to rise amidst continued hawkish rhetoric from central bankers. The US Federal Reserve kept interest rates on hold at their September meeting but again made it abundantly clear that investors need to get used to the idea of higher rates for longer. US equities in local currency terms had their worst month since September 2022; not helped by worries around another potential US government shutdown, which despite being avoided over the 30th September weekend, has since precipitated the ousting of Kevin McCarthy from his House speaker role, and raised renewed shutdown risks for November:

Fixed income markets had few bright spots to speak of in September, despite central banks beginning to signal that they are coming to the end of their rate hiking cycles. As the second chart below shows, performance was weak across the board, with bonds globally seeing their worst month in 2023, and government bond yields taking out some long standing records during the month.

UK Gilts (blue line) were the best performing developed market government bond index, falling by 1.0% and erasing gains enjoyed earlier in the month from a lower than expected inflation print and a ‘pause’ from the Bank of England. US Treasuries fell by 2.2%, with the yield on a 10 year Treasury at one point in September rising above 4.6%; the highest point since 2007.

Once again, the most significant weakness came from global inflation linked bonds (light blue line), which fell by 4.0%. This part of the market has a particularly high level of sensitivity to interest rate expectations due to its generally long-dated maturity nature, and with yields rising over the month, it was hard hit.

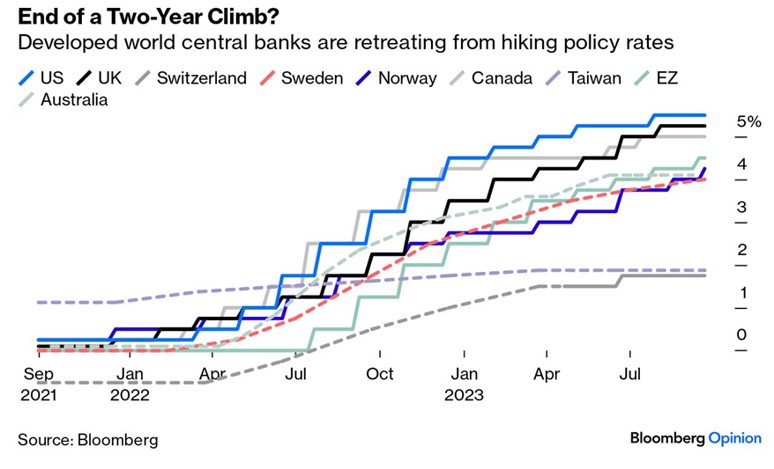

As mentioned above, a hot topic of conversation today is whether we have reached the end of central banks’ rate hiking cycles, and by extension, a peak for interest rates. The third chart below shows headline interest rate levels for a wide range of countries and regions, and after nearly two years of aggressive, rapid rate hikes, it shows what could be interpreted as a set of burgeoning plateaus:

Central banks’ sole focus remains on returning headline inflation back to target. However, given the progress made on rate hikes, and with headline inflation generally now beginning to slow, policy rates in most economies are now more likely than not close to peaking. After the massive overshoot of inflation targets we would expect central banks to tread cautiously in terms of future rate hikes, but to likely err on the side of keeping rates higher for longer.

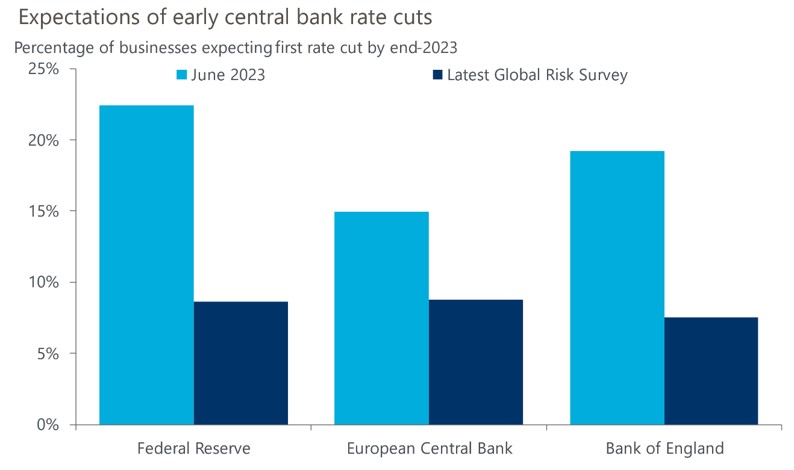

Of key importance is that investors and businesses are beginning to believe this rhetoric, as the fourth chart below shows. This chart illustrates survey data from a wide selection of global businesses, with the bars representing the proportion of respondents that believe each of the three major central banks will start to cut rates by the end of 2023. The light blue bars are the responses from June this year, and the dark blue bars are September’s responses, with a huge shift in beliefs being apparent over this short space of time – surveyed business leaders’ expectations for early rate cuts have collapsed as central bank rhetoric continues to be stoically hawkish.

Of course, we must remember that monetary policy is, as history suggests, about tightening until something breaks. If a financial crisis or a recession breaks out, interest rates will have to come down fast, though if inflation is still above target as and when that happens, central banks will face an interesting dilemma.

Looking ahead to the final quarter of 2023, it remains key to be diversified across asset classes, strategies and geographies as volatility is likely to remain elevated. In the first days of October we have seen large intraday swings in equity, bond and commodities markets, and with the lagged effects of much tighter monetary policy only slowly starting to filter through to the real economy (amongst other factors), market conditions may well continue to be fractious. Despite this uncertainty, we still see many good looking opportunities across the financial landscape, particularly within unloved parts of the equity market which should play out over the medium term and reward patient investors.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: