Market Updates

Harry Scargill

The positive sentiment from November carried on through December, as both equity and bond markets ended the year in in good spirits. The global equity index ended up 4.3%, which combined with the growth in November led to gains of 14% in the final two months of the year.

The significant driver of the returns for both bonds and equities was due to the continued downward trend of inflation seen across key markets. It was a similar story as to last month, with investors cheering the idea of inflation steadily moving back towards central bank target levels of 2%. This month’s numbers showed that in the US, inflation fell again to 3.1% from 3.2% in November, which led to the Federal Reserve (Fed), in their December meeting, outlining that rate hikes in the US are likely to now be behind us, and that we might see rate cuts in 2024.

Closer to home, we saw both the Bank of England (BOE) and European Central Bank (ECB) hold rates steady, following similar positive data relating to their inflation readings. UK CPI fell to 3.9%, from 4.6% in the previous month, whereas in Europe, headline inflation fell to 2.4%, the lowest figure for 2 years.

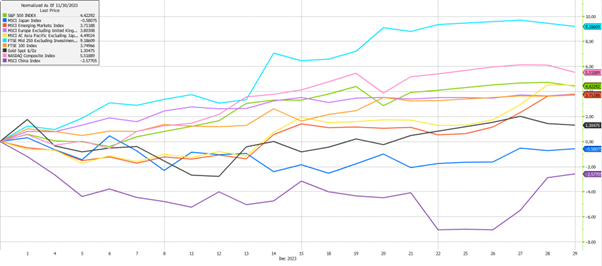

As the chart above shows, the strongest equity market in December was again the FTSE 250, gaining 9.2%, which replaced November as the strongest month of the year for the index. Elsewhere in the UK, the FTSE 100 also performed well, gaining 3.7%, which put it in the middle of the pack.

Continuing the trend of the year, we also saw strong performance from the technology heavy Nasdaq index, gaining 5.5%, with the wider S&P 500 not far behind at 4.4%. The S&P actually finished the year on a streak of 9 positive weeks in a row, the longest since 2004. This meant that as we closed out 2023, we sat with those two indexes trading very close to all-time highs. Asian equities also performed well, gaining 4.5%, following a rally in the last week of the year. The story was the same for Emerging Markets, which finished in line with European equities in gaining just below 4%.

The laggard was China, which despite a late rally lost 2.6% in December. We also saw Japanese equities lagging, with a fall of 0.6%, following a very strong year for that market.

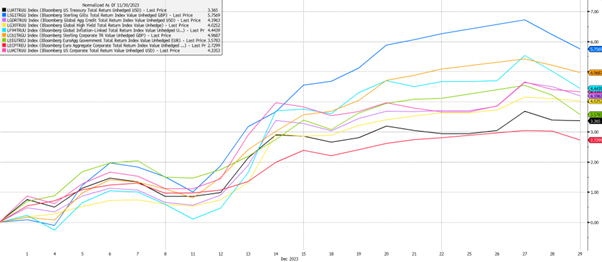

Much like equities, major bond indexes also finished the year very well, as shown in the graph above. It was a very good month for UK based bonds, with Gilts as the best performer, gaining 5.8%, followed by sterling corporate bonds which gained 5%.

We then have a cluster of indexes all increasing in the low-to-mid 4% range, which includes global inflation-linked bonds, global high yield, as well as global and US corporate bonds. Assets that still performed well but lagged were US treasuries at 3.4%, and European Government bonds and Corporate Credit which gained 3.6% and 2.7% respectively.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: