Market Updates

Imogen Hambly

Discover more insights from our Divisional Director, Peter Donaldson, and Investment Manager, Imogen Hambly as they delve deeper into last month’s market update.

In contrast to the broad-based rally that we saw in markets through Q4 2023, asset class returns were far more mixed during January, as investors sought to reassess their interest rate assumptions, pushing back the expected date of that all-important first rate cut.

Across developed markets, data releases continued to show economic resilience, with consumers still spending, housing markets still active, and government stimulus packages providing ongoing support to the corporate sector. Strong activity levels led inflation to surprise to the upside in December, although it remained on its downward trend. This offered sufficient evidence to support interest rate cuts through 2024, but forced traders to rethink when those cuts will begin, with central bankers eager to ensure they do not cut rates too early and reignite the fire of high inflation.

Against this relatively positive macroeconomic backdrop, equity markets returned a varied set of results, with the global equity index gaining 0.7% in sterling terms.

While developed markets were generally buoyed by the encouraging growth data, issues within the Chinese market led to losses across broad emerging market and Asian equities, despite announcements by the Chinese Communist Party (CCP) and the People’s Bank of China (PBOC) of a range of new stimulus measures.

Within fixed income, the re-adjustment in interest rate expectations weighed on returns from government and corporate bonds, with the global aggregate bond index falling 1.3%, in GBP, through the month. Other rate sensitive areas also struggled as short-term bond yields moved up. Most notably, real estate and small-cap equities both posted losses.

As tensions escalated across the Middle East, commodity markets performed well, with the Bloomberg Commodity index gaining 0.5%, in pound terms, and global oil prices rallying. Despite ongoing disruption through the Suez Canal and the consequent impact to global shipping, for now, aggregate commodity prices remain below levels seen at the start of the Israel – Gaza conflict.

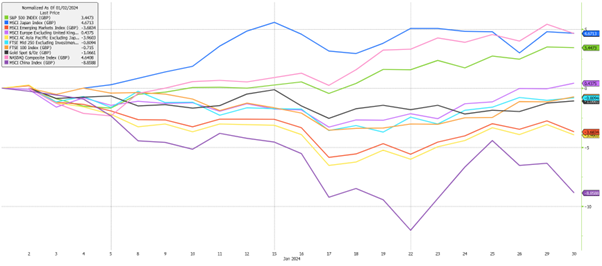

As the chart above shows, at a regional level, Japanese equities (in dark blue) retained their upward momentum from 2023, outperforming other regions and gaining 7.0% in local currency terms, or 4.7% in sterling, with the strength of the pound weighing on translated returns. Across Japan, stocks are continuing to benefit from positive investor sentiment, driven by a number of factors, including low inflation, a positive growth outlook, and policy driven corporate reform.

Elsewhere, the US technology index, the Nasdaq (in pink), had another strong month, gaining 4.6% in GBP and driving the broad US S&P 500 index (in green) higher. From an earnings perspective, recent results indicate a general decline in US profit margins through Q4, however from a macroeconomic standpoint, data continues to hold up well across the region, with employment and wage growth figures pointing towards a robust labour market, while December’s GDP print came in above consensus expectations. In combination, although downside pressures are beginning to filter through, optimism around a ‘soft-landing’ scenario still appears to be supporting the region’s stock market.

Across Europe and the UK, the prospect of higher-for-longer interest rates weighed on returns. European equities (in light purple) were positive in local currency terms, but flat in pound terms, while UK equities gave back a portion of the gains we saw through the latter months of last year.

As noted previously, it was another difficult month for the Chinese market (in dark purple), with equities failing to show any kind of positive price action. The aforementioned policy announcements made by the government and the PBOC through January were designed to provide support to the economy, the real estate sector, and the stock market. However, despite their best intentions, the short-term effect of the policies was to underscore concerns about an economic recovery that is being hampered by an ongoing property crisis, deflation, and weak consumer confidence. Poor performance from China filtered through to the broad Asia ex Japan (in yellow) and Emerging Market (in red) indices, where GBP returns through the month were -4.0% and -3.7%, respectively.

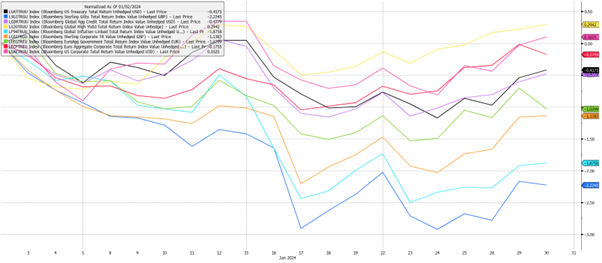

In bond markets, it was a return to the trend we saw through 2023 with high yield and global credit outperforming government bonds, as traders sought to balance the ongoing strength of economies with falling inflation data, ultimately parring back their bets on Q1 interest rate cuts and leading government bond yields to rise.

As the chart above indicates, the move upwards in government bond yields hurt much of the fixed income space, notably US Treasuries (in black) and UK gilts (in dark blue), which fell -0.4% and -2.2%, respectively. The Global High Yield index (in yellow), however, rose 0.3% through the month, benefitting from the more positive macro picture, and the resulting reduction in spreads. US Credit (in pink) also outperformed, eking out a positive return of 0.1%. Again, this comes as a result of reported economic resilience across the US.

Ultimately, the month saw market participants interpret the strength of the economic data as a clear indication that rate cuts are not yet required. Consequently, it was no surprise that central banks across the US, UK and Europe held interest rates steady, with, US Federal Reserve Chair, Jay Powell, turning uncharacteristically specific in his January press conference, stating that a rate cut as early as March is unlikely.

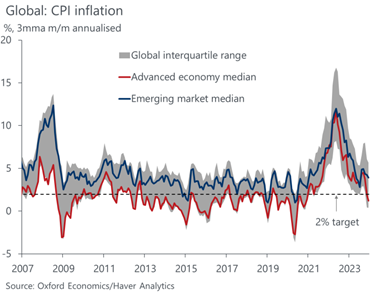

In spite of the more hawkish tone adopted by central banks through the month, it is still generally accepted that inflation levels are falling back to target, as shown below, and while aggregate GDP growth levels are slowing, economies are not likely to enter into deep recessions – meaning rate cuts can come during 2024, and they can do so at a considered pace.

Per the above, there is little denying that the inflation picture is beginning to look relatively healthy, with both core and headline figures moving in the right direction across emerging and developed markets. January has however drawn a spotlight towards the inflationary risks that are present in within the global economy right now.

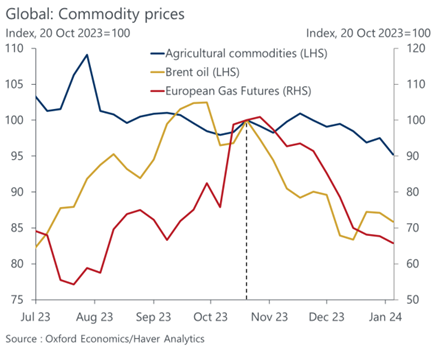

Commodity prices provided a strong disinflationary force through the latter months of 2023, with falling energy prices benefitting corporates and individuals alike.

Year to date though, escalating tensions across the Middle East and Red Sea have not only pushed up oil prices, but have added to shipping disruptions, with delays and rising costs beginning to intensify.

Encouragingly, corporates are so far managing to absorb these inflationary impulses through healthy inventory levels and well diversified energy systems. What’s more, Western economies are now benefitting from imported Chinese disinflation. As such, while activity levels in China remain depressed, it is likely that goods and commodity prices in the region are going to continue to fall and China will remain a disinflationary force, able to counteract the more inflationary geopolitical factors.

After what was an exciting end to 2023, the new year has started with a little less enthusiasm as investors have sought to digest the implications of December’s strong activity data, against a backdrop of falling inflation and mounting geopolitical risks. Despite this pick up in volatility, there remain plenty of opportunities across different asset class, but as always, diversification will remain key as we try to navigate this highly changeable market environment.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: