Market Updates

Harry Scargill

")

Gain a comprehensive overview of the market’s unexpected twists and turns, followed by a look into what to anticipate in the coming year.

Many readers will remember that coming into 2023, it was consensus from economists that we would see some, if not all, of the developed world enter a recession. A poll by the FT showed that in December of 2022, 80% of economists polled thought that we would be in a recession by the end of 2023, while some thought we were already in one at the time. We can now safely say that those predictions were wrong. Instead, throughout 2023, we saw unemployment stay low, consumer spending remain resilient and revisions for full year GDP, particularly in the US, revised consistently upwards.

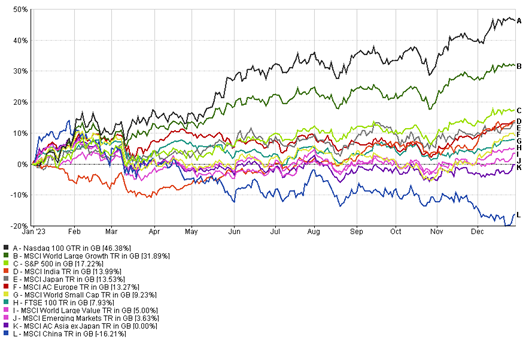

So, the recession never came and economic data across the developed world was better than expected. This therefore sets up for a good backdrop for equities – and it turns out, despite not feeling like it for much of the year, that 2023 was a good year for most risk assets. Below, we are showing returns, in sterling, for some major indexes across the full year. We have the Nasdaq that gained 46%, driven by excitement around Artificial Intelligence (AI) and the hope that we will soon be seeing lower rates in the US as inflation came under control. Followed by the, also tech heavy, World Growth index at 32%, then the broader S&P with a gain of 17%, India, Japan and Europe around 13%, global smaller companies at 9%, the FTSE 100 at a lower, but respectable, 8%, and then emerging markets up 4%. Asia finished flat and then the major outlier of Chinese equities, down 16%.

2023 has just shown how difficult it is to predict markets and economies, particularly as we still unwind issues from the pandemic and the considerable stimulus that came with it. We simply just don’t have precedent for an environment like this and how it may affect asset classes. So, despite many major events happening, accompanied by lots of very negative headlines, equities actually performed pretty well. The key therefore is to remain invested, stick to long-term planning, and allow the power of compounding to work in your favour.

As previously mentioned, a lot of the gains in markets this year have been driven by the rise of Chat-GPT, and what that could mean for wider use of AI advancements and who the winners of that story would be. Thus far, the main winners have been named as the “Magnificent 7”, which as a group consists of Apple, Microsoft, Alphabet (Google), Nvidia, Amazon, Meta (Facebook) and Tesla. These 7 stocks are now the 7 largest in the global equity index, accounting for 30% of the US index, and as a group gained around 106% (in USD) in 2023.

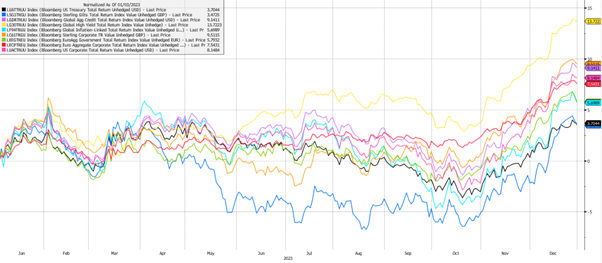

Turning to fixed income, much like equities, bonds battled through a difficult and volatile year, but ended in positive territory across all major indexes that we are showing below. The best performing index here is high yield bonds, gaining 13.7%, which came as a surprise to most investors, as this was an asset class many expected to be weak this year. This is a similar story for the equities, given the poor sentiment in this asset class coming into the year, economic resilience has really boosted returns of those invested. We have seen defaults rising through the year, but remaining low in context of history. However, despite this strong run, investors do remain somewhat cautious of high yield bonds due to spreads being very narrow compared to history and the difficulty it will likely face if the economy does begin to roll over.

We then have sterling credit, gaining 9.5%, global corporates up 9.1%, US corporates up 8.1% and European corporates up 7.5%. Again, benefitting from attractive starting yields and boosts from economic resilience.

The laggards are sterling Gilts, which rallied very strongly from November to end positive, having spent most of the year in negative territory, and up 3.4%. Around the same level of returns from US treasuries and slightly behind the global index-linked market.

As we look out to 2024, we enter with cautious optimism across equity and bond markets. The key question remains whether we have pulled forward a lot of the good news from 2024 into 2023, and whether we may still get the economic impact of the rate rises felt across the economy. Or whether we will truly enter a new growth cycle and the market has every right to be optimistic.

All eyes will continue to be focussed on inflation, unemployment and GDP growth, as a guide as to where central bank interest rates may be headed. Current consensus is that inflation will continue to move lower through this year, in a fairly stable manner, with the US and Europe ending the year close to the 2% target, and the UK still a little higher. Investors therefore hope that this will allow central banks to declare victory on their battle with inflation, and lower rates to a less restrictive level. Markets are currently pricing in around six 0.25% cuts in the US across 2024, which is double the guidelines provided by the Fed. The market is also expecting these cuts to happen in the first half of the year, maybe even in March, whereas the Fed has suggested they would come closer to the end of the year.

However, it remains key to understand what the cause of these cuts could be, as markets will react very differently based on whether the cuts are coming from a strong economic backdrop while inflation remains low, or whether we will need to cut rates to support a weaker economy. Many strategists are also making the point of why we would even want rate cuts if the economic data is still strong with low inflation, and that central banks might leave that option in their back pocket for any future issues that will inevitably crop up.

Entering 2024, we have valuations of equities looking fairly cheap in many regions, particularly the UK and Emerging Markets, which trade at a discount to the rest of the developed world and when compared against their long-term averages. We also have bonds providing very attractive yields, even at the lower risk end of the market, which should provide a good level of support for balanced portfolios. This provides investors with a relatively positive backdrop, alongside tailwinds such as AI, the green transition and potentially lower interest rates. We therefore continue to strongly believe that it is key for investors to remain diversified, and that while there are reasons to be more cheerful, there are still significant risks at play. Particularly given the fact we have both UK and US general elections likely to happen in the final quarter of the year.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: